After an extremely strong start to the year in the stock markets, a pullback during the 3rd quarter was to be expected. While red ink is never fun, the sell-off during the quarter wasn’t anyone’s worst-case scenario. In fact, it sort of made sense.

- Interest rates continued to climb higher.

- The economic data remained enigmatic.

- Analysts still wondered how many more rate hikes the Fed had up its sleeve.

- The money supply was basically stagnant, thanks to sluggish bank lending activity and energy prices accelerated.

The 3rd quarter is historically the worst for stock prices. While the financial industry refers to this market seasonality, you could also call it the summertime blues.

Despite the headwinds facing the U.S. economy, the labor markets have remained strong and given consumer spending a tailwind. Further, despite the slowdown in traditional banking, the mountain of cash sloshing about insurance company and private equity firms’ balance sheets has provided enough liquidity to keep activity going.

In so many ways, we ended the quarter in about the same place we started it, albeit a little lighter in equities. Clearly, that is no one’s definition of a worst-case scenario.

However, the question remains: How much longer until higher interest rates start to impact consumption patterns?

To date, the Federal Reserve has significantly increased the price of money over the past 18 months, and the economy has continued to grow. Is this monetary policy magic a delayed reaction, dumb luck or are things just different this time around?

The truth is this: 3rd quarter Gross Domestic Product (GDP) will likely be surprisingly high thanks to strong consumer spending. After that, however, we expect the official growth rate to start to slow for the next couple of quarters. As for the monetary policy magic? Perhaps the answer to that question is a little bit of all of it.

In the end, this past quarter was to be expected. It wasn’t a lot of fun, but the summertime blues rarely are. Do you want to know what is fun? The fall. It is my, and the markets’, favorite time of the year, and I am really looking forward to it.

Thank you for your continued support,

John Norris Chief Economist

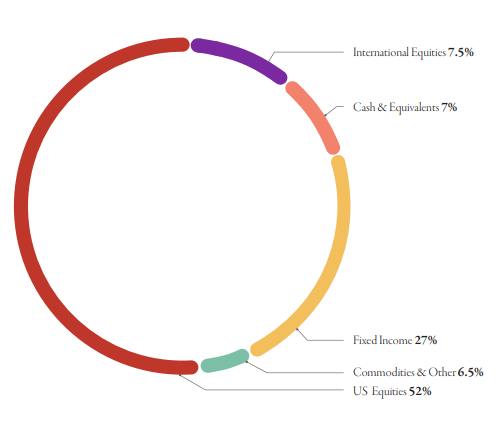

Our Investment Committee distributes information on a regular basis to better inform our clients about pending investment decisions, the current state of the economy and our forecasts for the economy and financial markets. Oakworth Capital currently advises on approximately $1.9 billion in client assets. The allocation breakdown is in the chart below.

The opinions expressed within this report are those of the Investment Committee as of the date published. They are subject to change without notice, and do not necessarily reflect the views of Oakworth Capital Bank, its directors, shareholders or employees.

This content is part of our quarterly outlook and overview. For more of our view on this quarter’s economic overview, inflation, bonds, equities and allocation read our entire 3rd Quarter 2023 Macro & Market Perspectives.