As we get ready to start the final 3 months of 2023, the equity markets have been able to digest some pretty good news this year. The feared economic recession that seemed almost inevitable just 9 months ago has not reared its ugly head.

- Inflation numbers have fallen from the extreme readings in 2022 to much more reasonable levels.

- The Federal Reserve has seen enough data to seemingly be very close to ending their push of higher interest rates.

- Finally, the job market has remained extremely strong, and has produced consumer spending levels that have kept the economy rolling.

We may have avoided the feared economic recession up to this point, but we are suffering through a different kind of recession: an earnings recession. While the second quarter earnings season slightly topped analysts’ expectations, they came in 5.4% below earnings for 2Q 2022. That was the third quarter in a row to show lower earnings than the year prior. A strong labor market, with strong wage growth, has lowered corporate profit margin. In other words, all of that record consumer spending did not equal record earnings.

While we still have some solid returns year-to-date for 2023, the 3rd quarter did not help the cause. It started off pretty strong, with more solid returns in July. August and September, however, provided losses across equity markets, as the markets began to price in “higher for longer” rates.

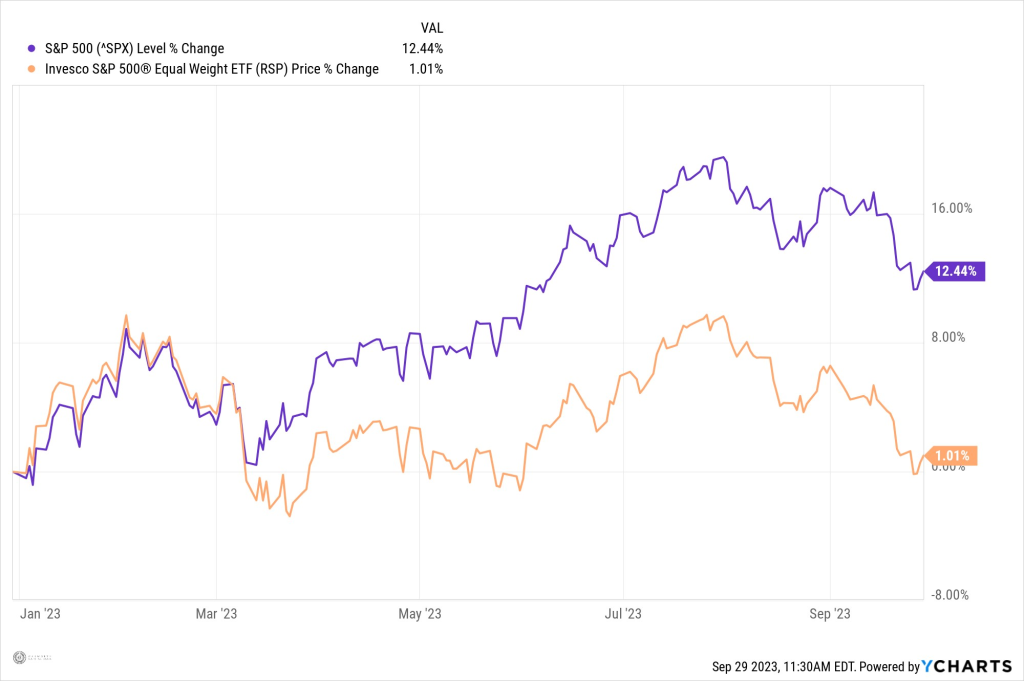

The narrow leadership of the “magnificent seven” stocks that propelled the vast majority of returns for the first seven months of 2023, struggled the last couple of months. This chart shows the impact those handful of stocks had on the return of the S&P 500 this year. The index is still up over 12%, while the average stock in the S&P 500 has returned a measly 1%.

Sectors

Two of the three economic sectors that have pushed returns for the S&P 500 (so far this year) fell in the third quarter.

- Technology (-5.84%) and consumer discretion (-5.0%) struggled in the quarter.

- Declines in Apple (-11.62%), Microsoft (-7.08%), Amazon (-2.48%) and Tesla (-4.41%) led these two sectors down.

- Communication Services (+2.84%) was led by Google parent company Alphabet (+9.32%) and Meta (+4.61%) continued its torrid pace, and is now up a whopping 166% so far in 2023.

Surging oil prices also helped energy stocks in the third quarter, with the price for a barrel of oil increasing from $70 to over $90. That kind of price change in the commodities usually translates to solid returns for energy stocks. This past quarter was no different, with a 30% increase in oil prices leading to a 15.7% increase in overall energy stock prices over the past three months. Individual energy stock standouts included ConocoPhillips (+15.63%) and Exxon Mobil (+9.63%).

- With the markets giving up ground in the quarter, it was somewhat surprising that the more defensive sectors of the markets showed such poor performance.

- Healthcare was a mixed bag with some large winners (Eli Lilly up 14.53% and AbbVie up 10.64%) and losers (Merck down 10.78% and Johnson & Johnson down 5.9%).

- The consumer staple sector lost 6.20% over the past three months, led by declines in both Coke (-7.04%) and Pepsi (-8.52%).

The real struggle from the three defensive sectors were found in the utilities stocks, which showed a decline of 10.10% for the quarter. Most investors have been buying utility stocks for their generous yield, trying to gain some income production while interest rates on bonds have been pretty skimpy for the past 20 years or so. Put another way, utility stocks have historically been used as a substitute for bonds.

Now that investors have the option to buy a 1-year U.S. Treasury with a yield north of 5%, the 4% dividend yield on a utility stock doesn’t seem as compelling. In 2020 and 2021 we would hear the acronym TINA, or There Is No Alternative to stocks. That is no longer the case, and the migration away from utilities the past few months highlights that shift.

Looking Ahead

The coming earnings season (3Q 2023) is expected to provide earnings that match the third quarter of 2022. Could we have a fourth quarter in a row of lower year-over-year earnings for the S&P 500, or will this “earnings recession” mercifully come to an end? As of today, analysts are expecting 3Q 2023 earnings to match those of 3Q 2022. The real excitement may be waiting for 4th quarter earnings season. Fourth quarter 2023 earnings are currently expected to be 9.5% higher than 4Q 2022.

Corporations hate to disappoint in earnings season, so if that 9.5% earnings growth for the fourth quarter is not realistic, we will see management bring down earnings expectations when they release earnings this quarter.

They would rather beat the current quarter by a penny, and lower guidance for next quarter by a dime. That will be the most interesting part of this coming earnings season… Get your popcorn ready!

Current market expectations are that the Fed could raise rates just one more time before they stop the hikes, and then wait for the effect of those higher rates to have an impact on the economy. The desired effect on the economy will almost certainly involve weakness in the labor market.

Inflation

We get fresh inflation data every two weeks, and we hope to continue to see those pesky inflation numbers continue to come down. The next “inflation hurdle” that the markets will be watching for is core inflation and how far it can drop.

- Currently the two core inflation measures (CPI and PCE) are down to 4.4% and 3.9%; from highs of 6.6% and 5.4%, respectfully.

During the last several weeks of the third quarter, movement in stock prices seemed to be driven by longer term interest rates moving higher, as equity markets started to price in a “higher for longer” interest rate picture. The Fed target for inflation remains 2%.

We have a long way to go to get there.

What will the Fed do if core inflation gets “sticky” north of 3%? Can the Federal Reserve help bring core inflation down close to their 2% target without causing significant slowdown to the labor market, and thus economic activity? That is the “soft landing” we are all hoping for. With unemployment still at a historically low 3.8%, and consumer balance sheets still pretty healthy, we can see some weakness in the labor market and still have a strong U.S. consumer.

Will the Fed be able to keep interest rates at their current elevated levels for an extended period of time, or do we need interest rates to go even higher? That will be the million trillion-dollar question. While that question remains to be answered, companies will (mostly) continue to do what they should do, and that is return capital to shareholders.

The optimism remains that if and when there is a slowdown in the economy, it will more than likely be the most talked about slowdown in quite some time. Companies are resilient, and the preparations and defensive posture that most companies have taken should help to prevent the pain in equities from becoming too unbearable, and in fact it may have already occurred. While an economic slowdown will eventually happen because that’s the life cycle of an economy, it does not mean economic ruin.

People will adapt, and companies will adapt, and the economy will again grow and expand like it always does.

The opinions expressed within this report are those of the Investment Committee as of the date published. They are subject to change without notice, and do not necessarily reflect the views of Oakworth Capital Bank, its directors, shareholders or employees.

This content is part of our quarterly outlook and overview. For more of our view on this quarter’s economic overview, inflation, bonds, equities and allocation read our entire 3rd Quarter 2023 Macro & Market Perspectives.