It is not a stretch to say that corporate earnings are the single most important factor in determining a value for that company, or its stock price. Each quarter, every publicly traded company announces their financial results of the previous quarter and give updates (or guidance) on current conditions and any changes in expectations for future quarters.

To better understand the earnings season, and how to interpret the data we receive, we must first understand the goals of both the analysts and

corporate management.

- The analyst receives much of their information from the companies they cover, and they want to keep a good working relationship with the

management of those companies. - Management, on the other hand, wants the analyst to portray their leadership of the company in a positive light. Job security for both parties.

With that in mind, let’s look at some of the most common trends of earnings season

- Preliminary projections: Analysts typically start to provide earnings estimates 12 months before the start of that year (in January of 2024 we start to see earnings estimates for full year 2025).

- Guidance adjustments: Analysts start earnings estimates with VERY optimistic glasses on. Those first earnings estimates are almost always lowered over the next 24 months.

- Earnings management: Corporate management never wants to have their actual quarterly earnings come in lower that the analysts’ consensus estimates. Over the past 10 years (i.e., 40 earnings seasons) 74% of companies have had their earnings results beat the analyst’s final consensus estimates. The average 10-year earnings “beat” is 6.7%.

S&P 500 EARNINGS

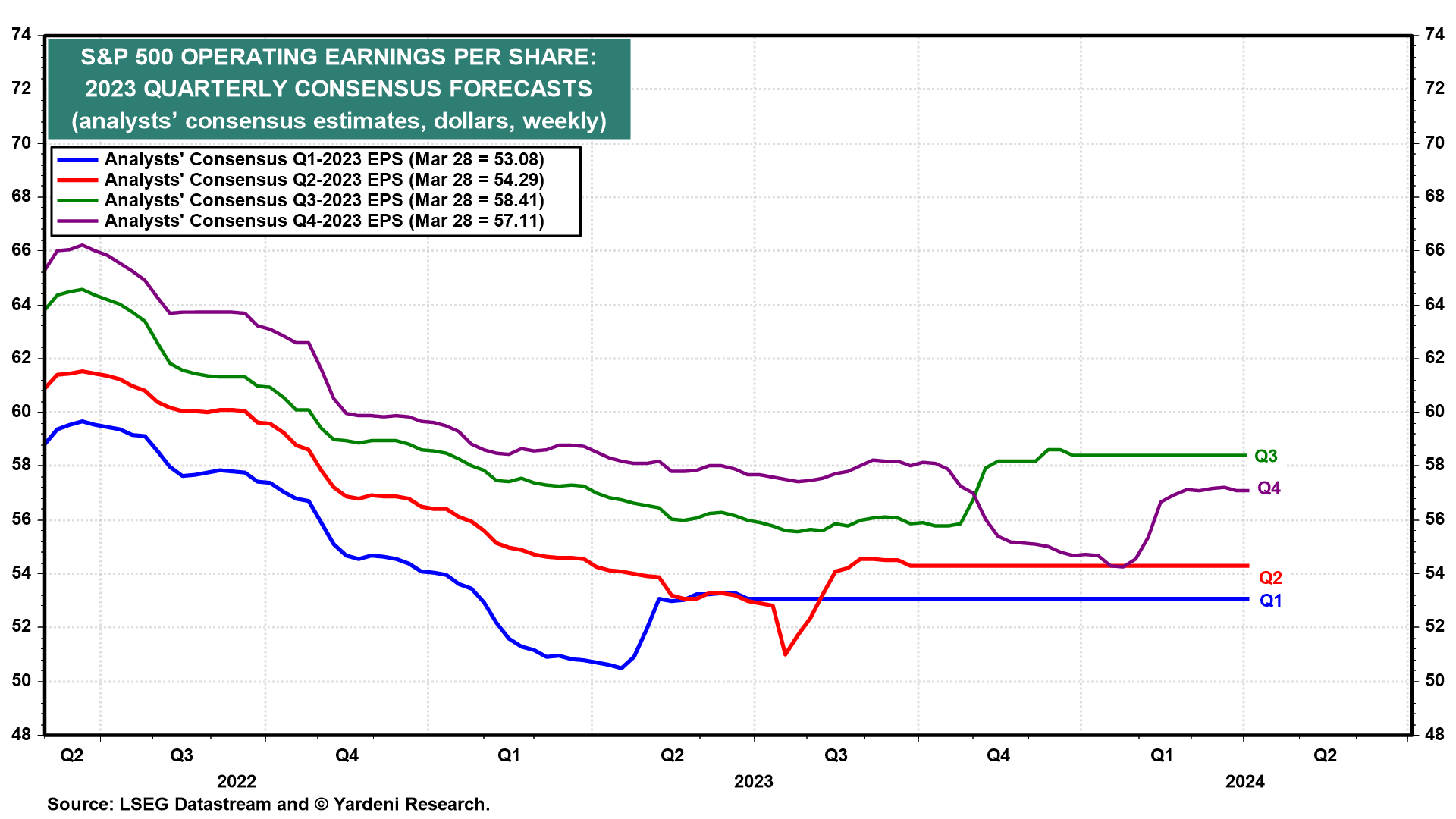

Twenty-twenty three ended up a very typical year for earnings. As indicated in the chart above, the past four quarters for the S&P 500 earnings estimates moved consistently lower until just before earnings were announced, and like magic, actual earnings ended up higher than the last estimate. Each quarter finished significantly lower than where the estimate started, but each quarter still ended up beating the final estimate.

This is why it’s important to take forward earnings estimates with caution when determining how expensive the stock market is currently trading. An optimistic earnings estimate will produce an artificially low price-to-earnings (P/E) ratio.

Earnings season can also give us information on how the eleven economic sectors of the S&P 500 are performing. Different sectors that show unusually strong or weak performance may give us some clues on the health of the economy. Additionally, we look for individual stocks with earnings performance that is significantly different from other companies in the same sector.

Moving forward, our Investment Committee will review each earnings season, providing our takeaways from the previous season and a perspective preview on the next. With only about four to five weeks separating the end of one earnings season from the beginning of another, there is scarcely any downtime in between.

4TH QUARTER RECAP & 1ST QUARTER PREVIEW

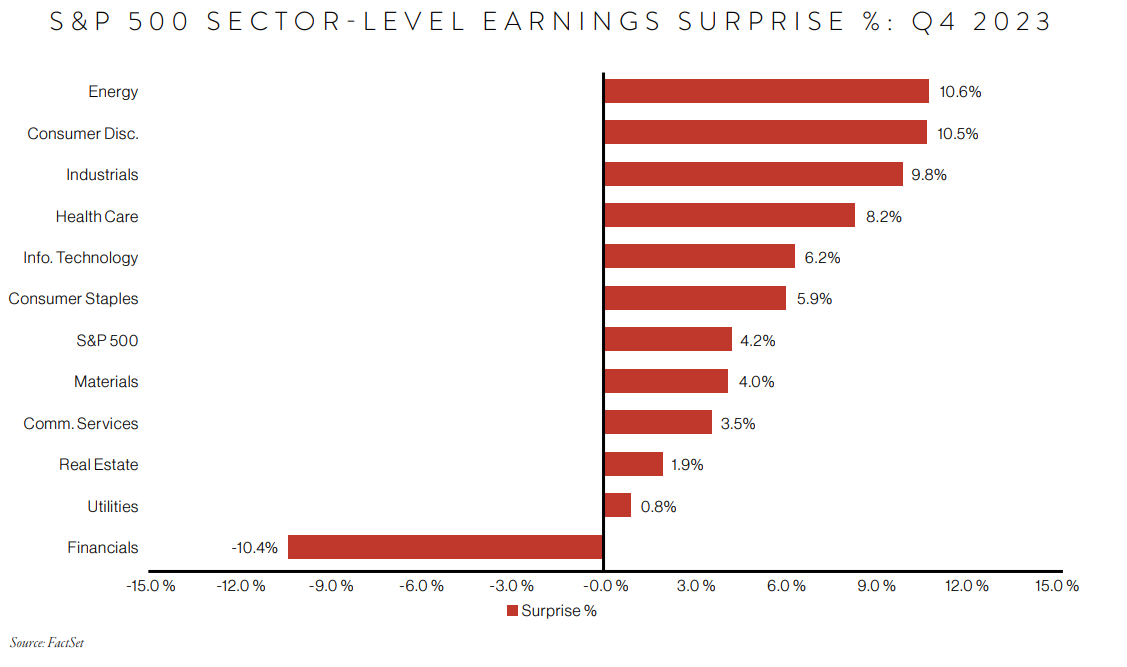

The largest financial stocks typically lead off the earnings report, and the 4th quarter earnings season started off with a whimper. Many of the largest financial companies showed large one-time charge-off’s that significantly lowered their earnings. The “leader” in the one-time charge-off category was Citigroup, recording $4.66 billion, which reduced earnings to a loss of $1.16 for the quarter and expected earnings of $0.81. After the dust settled on earnings from the financial sector, total earnings came in 10.4% below expected earnings..

Charge-off: When a debt is deemed unlikely to be collected after a borrower fails to make payments for a prolonged period of time.

Source: FactSet

Thankfully, things improved from there, as the remaining 10 economic sectors all reported earnings above analysts’ expectations. This outperformance was led by the energy (+10.6% above expectations), consumer discretion (+10.5%) and industrial stocks (+9.8%). The S&P 500 ended the quarter 4.2% above the analysts’ expectations, while actual revenue was 1.2% above expectations. Charge-off: When a debt is deemed unlikely to be collected after a borrower fails to make payments for a prolonged period of time.

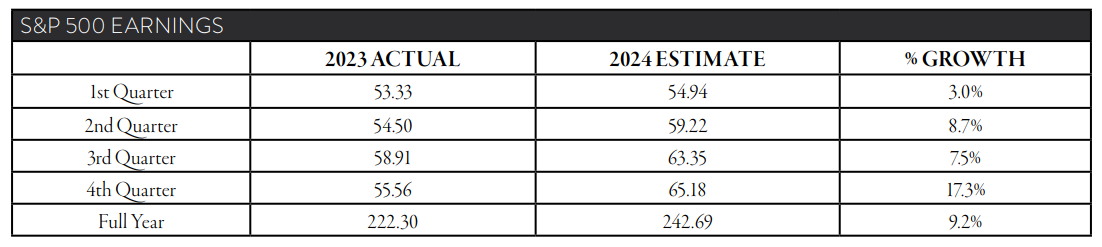

- For the full year of 2023, S&P 500 earnings are expected to close around $222.30 in earnings per share.

- This is only 1.4% higher that the earnings for full year 2022, which closed at $219.19.

- As we head into the first earnings season of 2024, analysts are expecting S&P 500 earnings growth of 10.6%, up to $243.60.

- The bulk of that earnings growth is expected to come in the 4th quarter, with a 17.3% increase year over year.

Not as much earnings growth is anticipated in the coming quarter, with expectations set at just a 3% increase compared to the first quarter of 2023. As we move through the first earnings season, we would not be surprised to see earnings slightly exceed expectations, followed by lowered guidance for the rest of the year.

THE FINANCIAL SECTOR

After such dismal earnings last quarter, the spotlight will remain on the financial sector this earnings season. With continued concerns over the valuation of commercial real estate in major cities, the banks that have a larger percentage of their loan portfolio committed to commercial real estate (including Wells Fargo, Citizens, M&T and Zions) will be carefully monitored. Other interesting points to consider from bank earnings will be net interest income (NII) and loan loss reserves. This will give us some insight on how the banks feel about the health of the economy. Higher loan loss reserves could indicate growing financial strain on consumers. However, with an unemployment rate still below 4% and wages growing at just above 4%, the consumer still appears to be in good shape.

TECHNOLOGY AND COMMUNICATION SERVICES

Some of the technology and communication services stocks that have shown very strong earnings growth the past few quarters, led by NVIDIA, Amazon and Meta, will try and keep up that impressive growth trend. Any hint of slowing growth could lead to trouble for a stock with a higher valuation.

CONSUMER DISCRETIONARY

Finally, earnings season is usually completed with some of the best-known retail companies. It is always interesting to get a gauge on the strength of the consumer and what are they spending their hard-earned cash on.

The chart below shows the great start to the year for equity prices (dotted blue line), but we have not seen a corresponding move-up with earnings expectations (solid line). We did see a decline in 2024 earnings expectations while the financial stocks were struggling through fourth quarter 2023 earnings season, but the successful remainder of earnings season allowed for this year’s earnings expectations to regain most of that lost ground.

IN SUMMARY

The move-up in stock prices over the first three months of 2024 can be supported with good 2024 corporate earnings. As I write this piece next year, the final 2024 earnings growth needs to be closer to the 9.2% growth that the analysts currently expect, and not a repeat of the 1.4% growth that we realized in 2023.

This content is part of our quarterly outlook and overview. For more of our view on this quarter’s economic overview, inflation, bonds, equities and allocation read our most recent issue of Macro & Market Perspectives.

The opinions expressed within this report are those of the Investment Committee as of the date published. They are subject to change without notice, and do not necessarily reflect the views of Oakworth Capital Bank, its directors, shareholders or employees.