At the start of 2023, the threat of recession loomed over the markets, and investors hoped the Fed would start cutting the overnight rate. Fortunately, despite all of the worry, the economy continued to expand, almost in spite of itself. Perhaps as a result, not only did the Fed not cut rates, it continued to increase them through the middle of the year.

Interestingly, the markets didn’t seem to mind these hikes in 2023 as much as they did in 2022. The fact that we were closer to the end of the tightening cycle than the beginning was apparently some type of solace. By the start of the 3rd quarter, investors finally felt comfortable that the Fed’s next move would be a cut.

Even still, at the start of the year, it appeared as though the Fed might have gone too far and too fast with its rate hikes than in the previous years. While it almost seems like ancient history, everyone held their collective breath when Silicon Valley Bank, and others, essentially failed at the start of the year.

Would this be the start of another financial crisis like the one in 2008-2009?

Fortunately, the answer was no, and the markets and economy were able to put the biggest wobble in the banking system in over a decade behind them surprisingly quickly. By the end of the year, it was almost as though it had never happened, at least as far as the markets were concerned.

Then, we had the various debt ceiling imbroglios, and let’s not forget the removal of the Speaker of the House of Representatives, a first. The never-ending war in Ukraine was never far from the headlines. The Chinese continued to cause trouble in the South China Sea, and Hamas started yet another conflict in the Middle East.

There seemed to be no end to the bricks in our wall of worry.

In a lot of ways, the world stumbled and fumbled its way through 2023. Still, thanks to a strong labor market, the U.S. economy continued to thrive, much more so than virtually anyone had predicted at the start of the year. As a result, investors were finally able to put away the worst of their worries by the start of November, and the stock markets soared.

It was a fitting end to what had been a confounding year.

In the end, while 2023 provided a lot of angst, it also produced a lot of economic activity and positive market returns. As we enter 2024, one can only hope we get a repeat of last year, at least in their stock portfolios.

Thank you for your continued support,

John Norris

Chief Economist

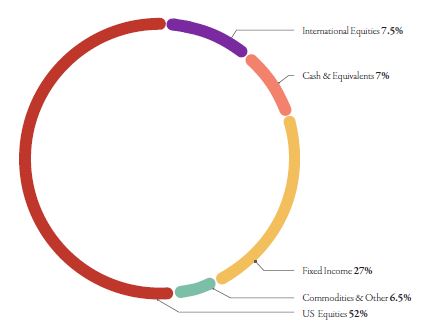

Our Investment Committee distributes information on a regular basis to better inform our clients about pending investment decisions, the current state of the economy and our forecasts for the economy and financial markets. Oakworth Capital currently advises on approximately $1.9 billion in client assets. The allocation breakdown is in the chart below.

The opinions expressed within this report are those of the Investment Committee as of the date published. They are subject to change without notice, and do not necessarily reflect the views of Oakworth Capital Bank, its directors, shareholders or employees.

This content is part of our quarterly outlook and overview. For more of our view on this quarter’s economic overview, inflation, bonds, equities and allocation read our entire Annual 2023 Macro & Market Perspectives.