Most predictions for stock performance in 2023 did not include large gains. The consensus predicted that we would see some form of a recession during 2023, and that a period of massive inflation would slow down the consumer, and the stock market along with it.

Well, the consensus was wrong.

- Economic activity actually picked up.

- The consumer continued to spend.

- Both happened with core inflation numbers coming down closer to the 2% target from the Federal Reserve.

Source: Bloomberg Financial

VOLATILITY IN THE MARKETS

The year 2023 ended up being a year made up of three strong rallies and two periods of rather large declines.

First Rally: The first six weeks of 2023 had the S&P 500 up almost 9%.

First Decline: The collapse of Silicon Valley Bank and Signature Bank led to the fear of more banking problems, and by mid-March the S&P 500 was all the way back to flat for the year. Second Rally: From that mid- March low until the end of July, stock prices moved up again. Stronger than- expected (or feared) earnings and continuously falling inflation numbers allowed the S&P 500 to approach a 20% gain. The fear of a recession began to disappear, and hope of an economic soft landing became more believable. Falling inflation numbers gave markets belief that the Fed was at the conclusion of their interest rate hiking cycle.

Second Decline: September and October are traditionally difficult months for stocks; 2023 was no different. As the calendar flipped from July to August, the mood of the equity markets started to change. The culprit? The bond market. The yield on the 10-year Treasury moved from 3.85% on July 26 all the way to a peak of 5% on October 18. During that time, the near 20% return for the S&P 500 had eroded to a 7% gain.

Final Rally: That rising yield on the 10-year Treasury turned dramatically in November and December. The yield on the 10-year Treasury fell all the way back to 3.86% by the end of the year. We also received some lower-than-expected inflation numbers and dovish comments from the Fed that gave equity markets hope – not only that we have seen the last rate hike of this difficult cycle, but also that a rate cut may finally be coming. The last two months of 2023 gave us our most powerful rally of the year, with the return for the S&P 500 climbing all the way up to a 24% gain for the year. The S&P 500 ended 2023 on a nine-week winning streak.

IN RETROSPECT

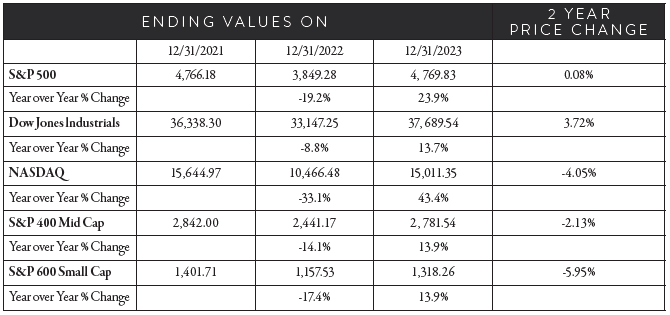

For even more perspective, let’s look back a bit further. As the Waterford Crystal ball dropped in Times Square on December 31, 2021, the stock market was just weeks away from the start of what would become the most aggressive tightening cycle from the Federal Reserve in decades. That last trading day of 2021, the S&P 500 closed at 4,766.18. As that same ball dropped this New Year’s Eve, the S&P 500 closed 2023 at 4,769.83. So, over the course of two years, the S&P 500 provided a price change of a whopping 3.65 points, or 0.076%.

Source: Bloomberg Financial

That price move for the S&P 500 would normally be associated with one very slow trading day, not two extremely volatile years. As a matter of fact, in only a few of those 504 trading days comprising the past two years of trading would the S&P 500 show a price change of less than 3.65 points.

Not only have we traveled through the rising interest rate cycle from the Fed these past two years, we have seen wars break out in both Eastern Europe and the Middle East and countless stories of political disfunction out of Washington. We are officially right back where we started.

The S&P 500 was not the only index that showed this type of performance. It’s important not to confuse the lack of price change over the past two years with a lack of volatility. The years 2022 and 2023 were mirror images of each other, with the first year showing large losses, and 2023 providing significant gains.

Equity index prices are not the only thing that has not changed dramatically over the past two years, as corporate earnings also seem to be stuck in neutral.

- S&P 500 earnings moved from roughly $215 in 2021 to $220 in 2022.

- With only the 4th quarter earnings season left, it does not appear that earnings for 2023 will be much above the $220 earned in 2022. Companies found it much more difficult to pass along all of their increased costs to their customers.

- As sales increased almost 3% in 2023, earnings were flat.

SECTOR SPECIFICS

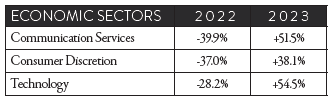

The worst performing indexes in 2022 were the best performing in 2023. The same pattern held for sector performance. Technology, Consumer Discretion and Communication Service sectors recovered from miserable 2022 performances to show the best returns in 2023.

The strength of the largest stocks in the S&P 500, dubbed the “Magnificent Seven,” led the strong market performance all year.

These stocks (Apple +49%, Microsoft +56%, NVDIA +349%, Alphabet +67%, Meta +68%, Amazon +194% and Tesla +59%) accounted for 63% of the entire return of the S&P 500 this year.

It is not surprising that all seven of these companies are members of the three best performing sectors.

By the end of 2023, those seven stocks now provide just over 30% of the weight of the S&P 500, and even a larger weight of the NASDAQ composite index. It was only the equity rally in November and December that saw a broad advancement of stocks, and not one led by the Magnificent Seven. The average stock from the S&P 500 was not nearly as strong as the index returns. These few eye-popping individual stock returns turned a good year of equity performance into a great one.

With recession fears front and center as we entered 2023, the three defensive sectors ended up being a surprisingly bad place to try to get through 2023. Healthcare (0% return in 2023), Consumer Staples (-4%) and Utilities (-11%) all significantly underperformed the broad market. The only other sector that provided a loss last year was the Energy sector (-3.5%). In 2022, Energy was the only sector that provided a positive return (+65%).

LOOKING AHEAD

So how did most experts get their 2023 economic and market predictions so wrong?

We ended up with strong economic activity instead of the feared recession. The labor market did not weaken, it somehow got even stronger. This, in spite of the fact that the Fed raised interest rates even more than most market experts predicted.

In more normal times, rising interest rates and ever-increasing prices (inflation) would be met with a consumer who would limit their spending. This was likely factor contributing to concerns about a recession at the beginning of 2023.

However, the unexpected resilience and strength of the consumer was driven from two main components.

- Labor Markets

First, the labor market remained red hot, and with low unemployment rates and increasing wages, the consumer felt compelled to keep on spending. And indeed, they did. Will the labor market finally cool off some in 2024 and see the unemployment rate move back up to more typical levels? Will corporate leadership try to stop the decline in profit margins and trim down their number of employees? Many companies have maintained higher staffing levels due to concerns about their ability to rehire in the future. If that fear of not being able to rehire subsides in 2024, we may finally observe the anticipated weakening in the labor markets. - Excess Cash

The other component that may have changed the normal reaction to a period of extreme inflation was the amount of excess cash, around $4 trillion, the consumer had saved from the COVID economy of 2020 and 2021. Higher interest rates did not matter to a consumer spending saved cash. Why? They weren’t borrowing money they were then spending.

A RETURN TO NORMAL?

At the end of 2023, we started to see some signs that the consumer was starting to return to more normal patterns. Airlines and hotels that have been slammed since the lifting of COVID travel restrictions in 2021 are starting to see future booking return to a more normal level. The vast majority of that excess “COVID cash” has finally been spent.

How all of these changes play out will have a direct impact on corporate earnings. Will we finally break out and see growth in corporate earnings? Current estimates for S&P 500 earnings for 2024 are $245, or an 11% increase from 2023. These earnings predictions usually end up being a bit optimistic, so something around $235 may be more realistic. Based on the current S&P 500 level of 4,769, we are trading just over 20x earnings.

Currently, the futures market expects the Fed to cut the Fed Funds rate from its current level of 5.5% down to 4% by the end of the year. If that were to happen, we could see slight multiple expansion over the next 12 months for another positive year of equity returns.

As a reminder, 2024 also gives us a presidential election. This one should be interesting! Typically, the stock market likes certainty. By the first week in November, we should know what political party controls the White House and both chambers of Congress.

Do not be surprised if the incredible performance of the Magnificent Seven can’t continue into the new year. Smaller stocks and more value names may finally have their day in the sun. In this scenario, the average stock may outperform the overall index. Another mirror image.

The year 2024 looks to be a decent-but-not-great year for equity performance. The second half of the year may be where we see better performance. That gives us some time to see inflation numbers continue to get closer to the Fed target of 2%, and (hopefully) the November elections will give us some

political certainty.

The opinions expressed within this report are those of the Investment Committee as of the date published. They are subject to change without notice, and do not necessarily reflect the views of Oakworth Capital Bank, its directors, shareholders or employees.

This content is part of our quarterly outlook and overview. For more of our view on this quarter’s economic overview, inflation, bonds, equities and allocation read our entire Annual 2023 Macro & Market Perspectives.