Well…maybe sometimes fight the Fed.

2023 will always be looked at as a year that puts a little asterisk next to the adage that famed investor, Marty Zweig, coined in 1970. The saying makes sense. All too often, the Fed seems to follow the famous saying in the tech space of “move fast and break things,” as their policies both under-and overshoot frequently. Be it their inability to hit 2% inflation for most of the last (pre-COVID) decade, or the continued loose post-covid policy that at least didn’t help tame the rampant inflation to come.

Basically, when the Fed shows up to cool things off, don’t stand in their way.

THE STOCK MARKET

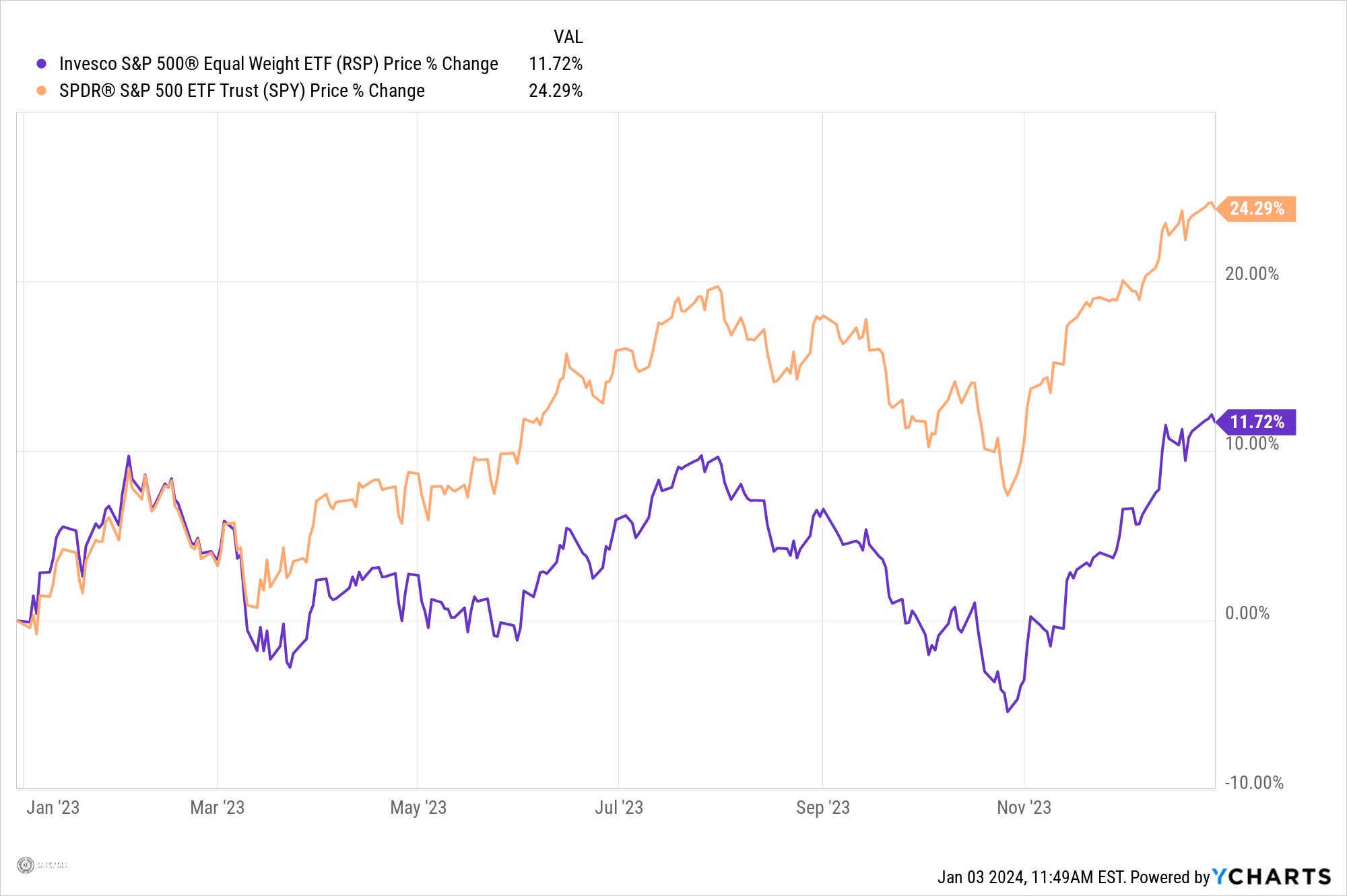

Not only was 2023 a tough year for the “Don’t fight the Fed” crowd, but it was also a tough year for the stock-picking crowd. Never in this century has there been more names within the S&P 500 underperforming the index. Shockingly, the equal-weighted version of the S&P 500 underperformed the standard S&P 500 by over 12%!

In fact, that same equal-weighted index was down for the year, as recently as November 10th. That is, if your portfolio didn’t have at least a market weighting to what is now being called the Magnificent Seven (Apple, Amazon, Microsoft, Alphabet, Tesla, Nvidia, Meta) then you likely underperformed ‘the market’.

EQUAL-WEIGHTED S&P 500 VS STANDARD S&P 500

As good of a year as this was on the surface, things were not, and continue to be, far less smooth underneath.

That begs the question, what does this mean for our Investment Committee’s thoughts, and subsequently our allocation?

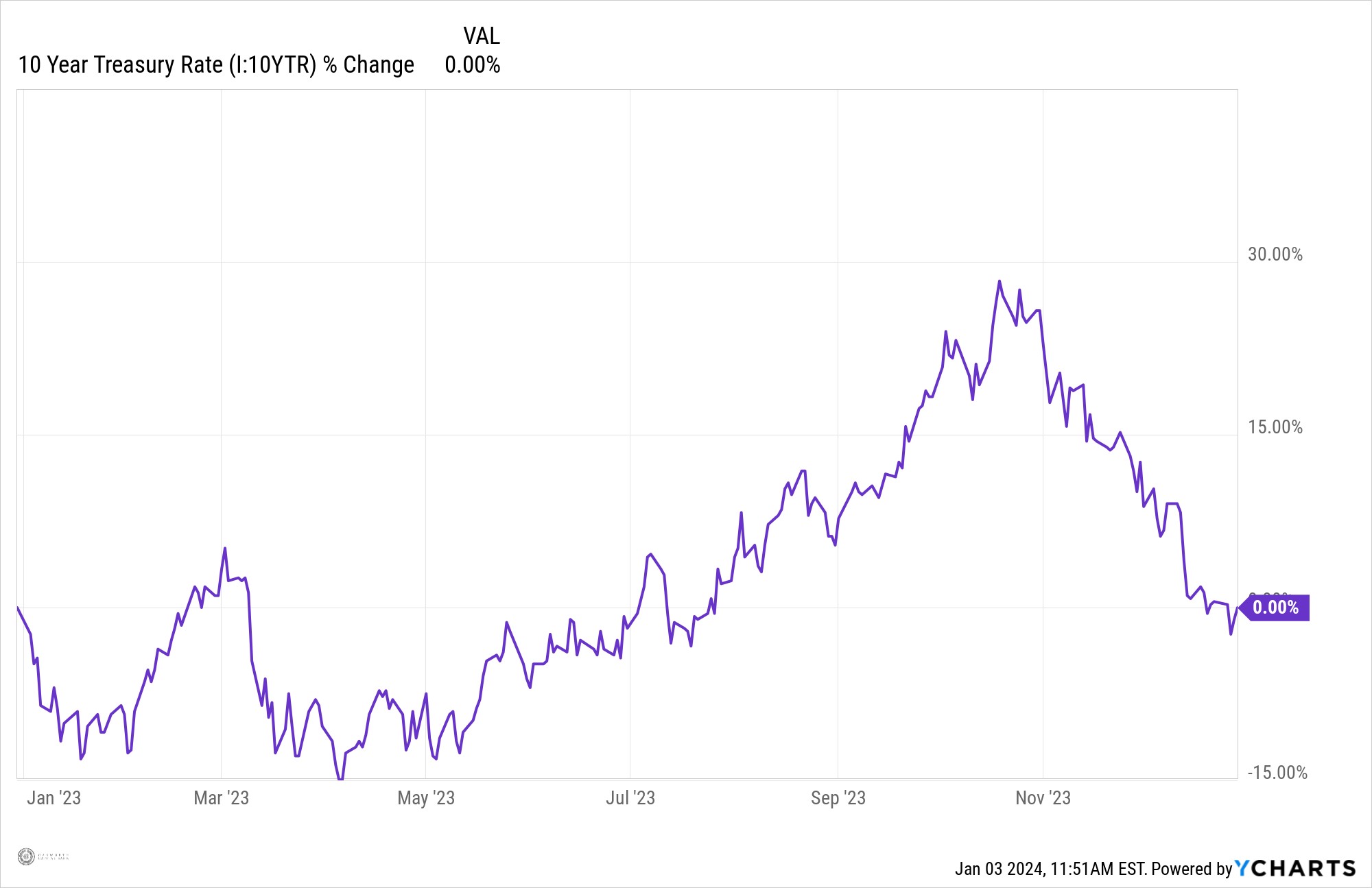

If you have been asleep since the beginning of the year and just woke up to check the bond market (highly unlikely but not impossible), you would have probably thought this was a pretty uneventful year.

The 10-year treasury is exactly where it was to start the year. However, this has involved a low of 3.30% and a high of nearly 5%. That is a wildly volatile year.

10-YEAR TREASURY

THE BOND MARKET

The bond market had a tough time deciphering things this year. With varying messages coming from Federal Reserve officials, a mix of weak and strong economic data, and a substantial influx of new treasury bonds, the interest rates pendulum swung drastically. What this meant for us and our allocation was to keep duration short to start the year. This short duration bond portfolio insulated us as best as possible from the rate hikes that we expected and subsequently saw. In the 3rd quarter, however, it became pretty clear. The Fed was done even though they didn’t say it as clearly. Much like a birthday wish that, if said out loud, won’t come true.

This meant if they flipped so dovish, the market would front run them entirely and not give them the chance to loosen policy as they may have desired.

We saw through this though.

The Fed was and is done, and with that, we had the green light to shift duration out. Not exponentially, but to around neutral, enabling us to “lock in” those higher rates that were clearly not set to last with the Federal Reserve taking their foot off the pedal. This was the right call. At the time of our trades, the ten-year treasury was over 4.80%, and is currently nestled around 3.90%.

There are two main ways to make plays on fixed income: Changing duration and changing credit quality. We have leaned on the former, as credit spreads have not widened, making the risk reward unattractive by our estimation.

But you can’t talk about stocks without discussing the Magnificent Seven, as mentioned earlier. These names, funny enough, are often viewed as tech stocks; however, only three them technically are (Apple, Microsoft,

and Nvidia).

- All seven were up tremendously with Nvidia and Meta leading the way both up over 200% for the year.

- All seven contributed to the Nasdaq being up over 50% for the year.

These names emerged as leaders for a whole host of reasons that I could expand on; however, I will focus on one particular trend that has been, and will likely continue to remain, significant – the swinging of the pendulum. As much as all of these names were up this year, the pendulum swung in the opposite direction in 2022, with the Nasdaq experiencing a decline over 32%. This decline was led by the likes of Meta and Tesla, down over 60% each.

Up until the last two months, the market under the surface of these names did not have a good year. As I mentioned earlier, the equal weighted was down for the year as recently as the beginning of November. Small and mid-caps were down as well. This was the opposite of the “everything rally”. I’ll call it the “almost-nothing rally”. For us and our allocation, we have maintained a roughly-neutral-weighting to the large-cap growth stocks leading the “almost-nothing rally”.

With this, as the year has gone on and the rally has largely continued, we have found opportunities to add to some of the more value-oriented cyclical sectors that have not contributed to the rally. This included things such as small-cap stocks, as well as Energy and Financials.

“We have found opportunities to add to some of the more value-oriented cyclical sectors that have not contributed to the rally. This included things such as small-cap stocks, as well as energy and financials.”

ENERGY

The case for Energy can be made as complex as one would like; however, it can also be made simple. The demise of oil dependency has been greatly exaggerated; most barrels of oil are bought and sold in U.S. dollars. As the Fed begins to cut rates, the dollar should weaken… meaning it will take more dollars to purchase the same barrel of oil. Oh, and the sector is largely cheap (undervalued) and has robust cash flow generation. See? It’s quite simple, really.

FINANCIALS

Financials on the other hand have become the boogeyman of sectors, ever since the Silicon Valley Bank collapse. One that scared analysts into having to actually do their due diligence and understand the assets of the companies they track. It was not necessarily elevated interest rates that hurt banks, rather it was the rapidity at which rates increased and the unexpectedness that caught many off guard. Higher rates are frankly not bad for banks. Regional and Money Center banks have large amounts of non-interest-bearing deposits, meaning they have very healthy margins, especially when the rates they charge on their loans go up.

“As long as the balance sheet is healthy, and the investments made are wise, banks can continue to turn a healthy profit.”

SMALL-CAP STOCKS

Small-cap stocks are attractive for several reasons. First of all, they’re cheap. The companies in the S&P 600 small-cap index are trading at forward earnings multiple of 12x. This is the case, even after the 20+% rally the sector experienced during the last two months of the year. Secondly, this sector is more diverse across sectors than large-cap, with the three largest sector weightings being Financials, Industrials, and Consumer cyclical. All areas we think will do well.

OUR THOUGHTS

Take all of this and put it together, and it means in our view, the pendulum should swing back slightly. This doesn’t mean Tech will fall apart, or even that it demands a pull back, rather the “almost-nothing rally” should continue to broaden out and include more names outside of the Magnificent Seven. With the large recoveries we have seen in those names, it is our view that a broader range of companies will begin generating stronger returns. If the Fed is able to cut rates due to lower inflation rather than an economic slowdown, as currently anticipated, it is expected to have a positive impact on market confidence and will continue to broaden out.

As always, we will remain open minded to the incoming data and how it fits into the mosaic of the overall economic outlook, with a focus on generating the best possible risk adjusted returns for our clients.

The opinions expressed within this report are those of the Investment Committee as of the date published. They are subject to change without notice, and do not necessarily reflect the views of Oakworth Capital Bank, its directors, shareholders or employees.

This content is part of our quarterly outlook and overview. For more of our view on this quarter’s economic overview, inflation, bonds, equities and allocation read our entire Annual 2023 Macro & Market Perspectives.