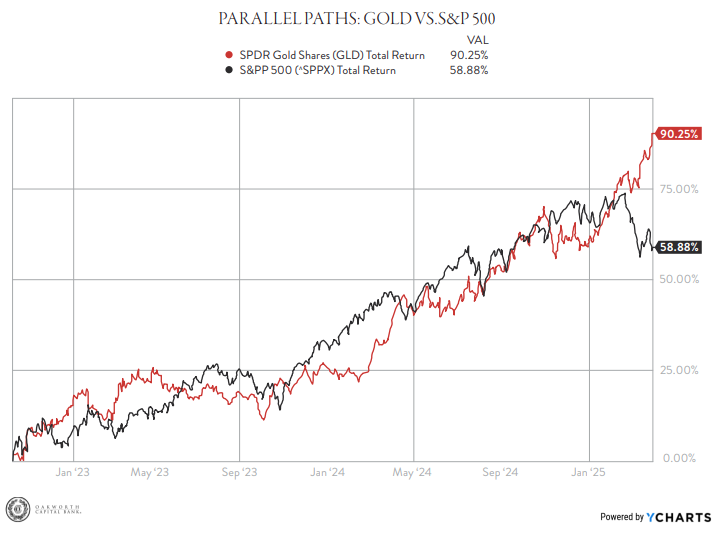

As of March 28, 2025, gold has outpaced the S&P 500 by more than 32% over the past year! What is driving this spike for a metal that we love to look at, but offers no cash flow? After all, only about 1/10 of the amount of gold that is mined each year is used for technology and industrial purposes. So why the recent run up in prices?

A lot of it has to do with the global uncertainty that’s been hanging over us – pandemic recovery, geopolitical chaos, stubborn inflation, and the Russia-Ukraine war. All of this has pushed investors and central banks to flock to gold as a safe haven, and that demand has sent gold prices soaring.

HOW DOES FOLD MOVE WHEN THE FED CHANGES RATES?

The price of gold can be influenced by the U.S. Federal Reserve, and how it implements monetary policy.

Quantitative Easing: Generally speaking, when the Fed cuts the overnight lending rate or increases money supply throughout the financial system (a process called Quantitative Easing, or QE), one could expect gold to generally increase in price. Lower interest rates and more liquidity usually lead to higher inflation expectations, and when the market is worried about inflation, gold is one of the first places cash is rotated into as a hedge. Hard asset prices tend to artificially rise when there is more money sloshing around in the system.

Quantitative Tightening: In contrast, when the Fed raises rates or starts pulling money out of the system (Quantitative Tightening, or QT), one could expect the price of gold to struggle. When monetary policymakers set the overnight lending rate higher, treasuries, bonds and other assets become more attractive, so demand for gold lessens. This situation played out for much of 2021 and into 2022 when it was clear that monetary conditions would soon tighten as inflation risks rose.

GOLD & EQUITIES: UNDERSTANDING THE DUAL RALLY

Surprisingly, gold has been moving in lockstep with the S&P 500 since the most recent bear-market-bottom in October 2022, even as interest rates continued to rise.

Is gold proving to be more than just a safe haven? Or is it the voice of reason while the stock market drifts further from reality?

Gold is typically seen as a refuge when stocks fall, but recent price action has challenged that view. Persistent inflation has only fueled the rally, presenting challenges for monetary policymakers around the globe. Despite the U.S. stock market hitting new highs recently, there’s still plenty of uncertainty lingering in markets. In the U.S., the Federal Reserve has raised interest rates to combat inflation, rattling investor’s nerves about the longer-term economic picture. Even as stocks have recovered, gold has also maintained a stable store of value amid longer-term uncertainty surrounding inflation.

PARALLEL PATHS: GOLD VS. S&P 500

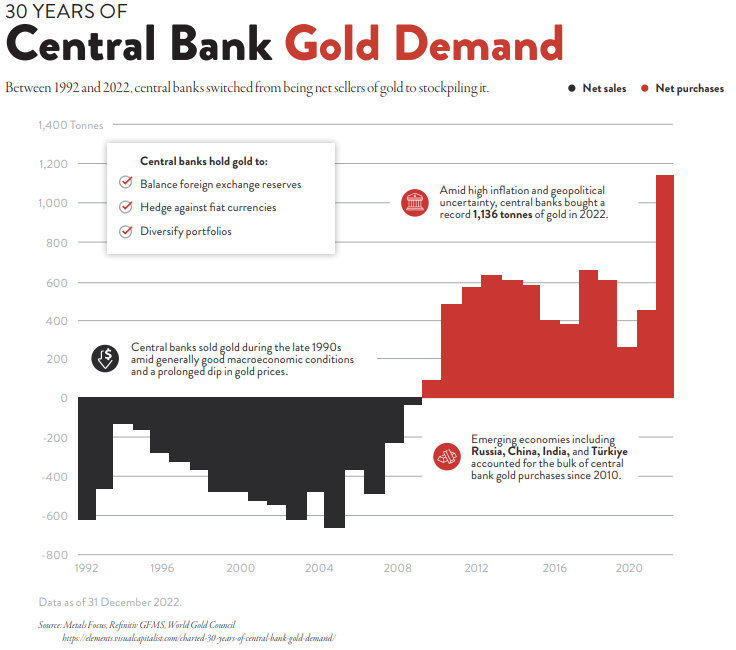

CENTRAL BANKS RUN ON GOLD

In 2022, central banks bought more than 1,100 tonnes of gold —the highest in decades, according to the World Gold Council. Why? Simply put, they want something stable, something that we know the world only has so much of – a scarce resource. Central banks are always looking to protect their economies, and gold is an easy way to do that. It’s a proven hedge against inflation, a buffer against currency devaluation, and it helps diversify reserves. Countries like China, Russia, and India have been big players in this gold rush, aiming to reduce their reliance on the U.S. dollar. By buying up gold, they’re building a buffer for themselves against global volatility.

Ultimately, the gold market’s major shift over the past decade can be attributed to central banks significantly increasing purchases driven by economic, geopolitical and strategic factors. The global economy has faced harsh challenges, such as the COVID-19 pandemic, which led to massive fiscal stimulus, soaring inflation, and increased market volatility. In such an environment, gold acts as a safe-haven asset that preserves value during periods of uncertainty.

Central banks have turned to gold to safeguard their reserves from inflation’s erosive effects – something paper fiat can’t reliably do. Geopolitical tensions, particularly the Russia-Ukraine war, have further highlighted the risks associated with relying on fiat currencies and traditional financial systems. The war and subsequent sanctions have amplified concerns about the stability of global trade and financial systems, prompting central banks to strengthen their reserves by accumulating gold.

Meanwhile, BRICS countries (Brazil, Russia, India, China, and South Africa) are actively working to shift the world away from the U.S. dollar as the world’s reserve currency, and demand for gold has only increased. If not the dollar, what other fiat currency is trustworthy enough to be THE world’s reserve currency? Therefore, many central banks have been increasing their gold reserves to reduce exposure to the dollar and safeguard against fluctuations in foreign exchange markets. These factors, combined with a period of low-interest rates following the Great Financial Crisis and gold’s role as a global liquid asset, have driven central banks to buy gold at levels well above historical norms.

WHAT’S NEXT FOR GOLD?

Bullish sentiment hit a staggering 99.8% according to the Consensus Inc. survey — enough for a contrarian to raise eyebrows. This could be ripe for a pullback, and although pullbacks might occur, overall, conditions remain strong. Central banks are likely to continue buying gold as they diversify away from the U.S. dollar. And with inflation still elevated, gold should continue to be a go-to hedge for investors looking to protect their wealth.

Bottom line: Gold’s role in the global financial system is stronger than ever, and its price will likely keep moving in sync with the broader economic picture. Whether it’s more purchases from central banks, inflation fears, or geopolitical risks, gold’s staying power as a safe asset looks solid. As renowned investor and academic Marty Zweig once said, “the trend is your friend” — and right now, gold’s trend is certainly upward.

This content is part of our quarterly outlook and overview. For more of our view on this quarter’s economic overview, inflation, bonds, equities and allocations, read the latest issue of Macro & Market Perspectives.

The opinions expressed within this report are those of the Investment Committee as of the date published. They are subject to change without notice, and do not necessarily reflect the views of Oakworth Capital Bank, its directors, shareholders or associates.