Financial Highlights

EPS, diluted and adjusted for significant items*up 45%

Net income up 47%*

Pre-tax, pre-provision income up 54%

excluding significant items*

$1.3 Billion

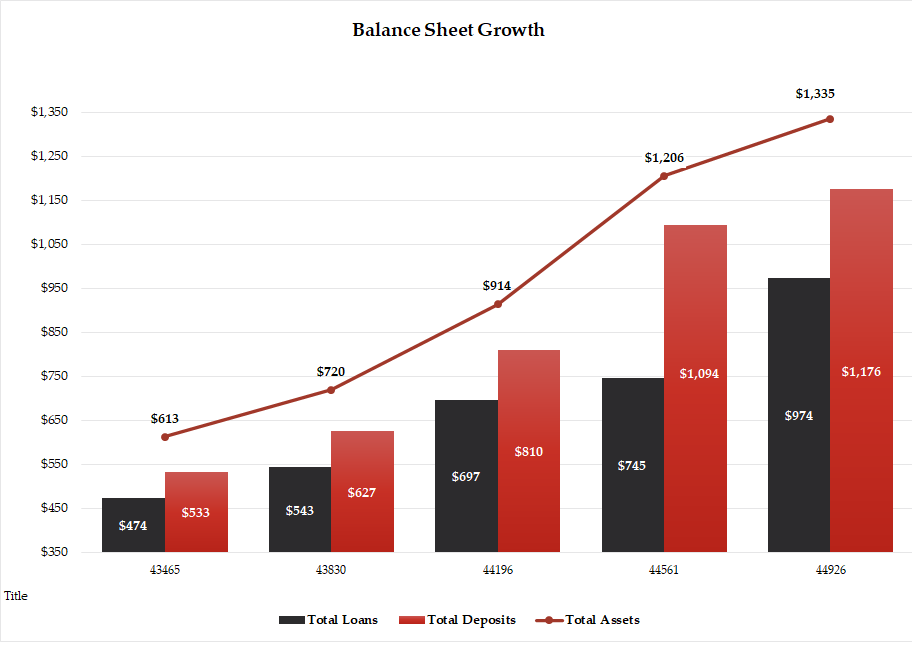

Total Assets

31% growth in total loans year-over-year to $974 million

8% growth in total deposits year-over-year to $1.2B

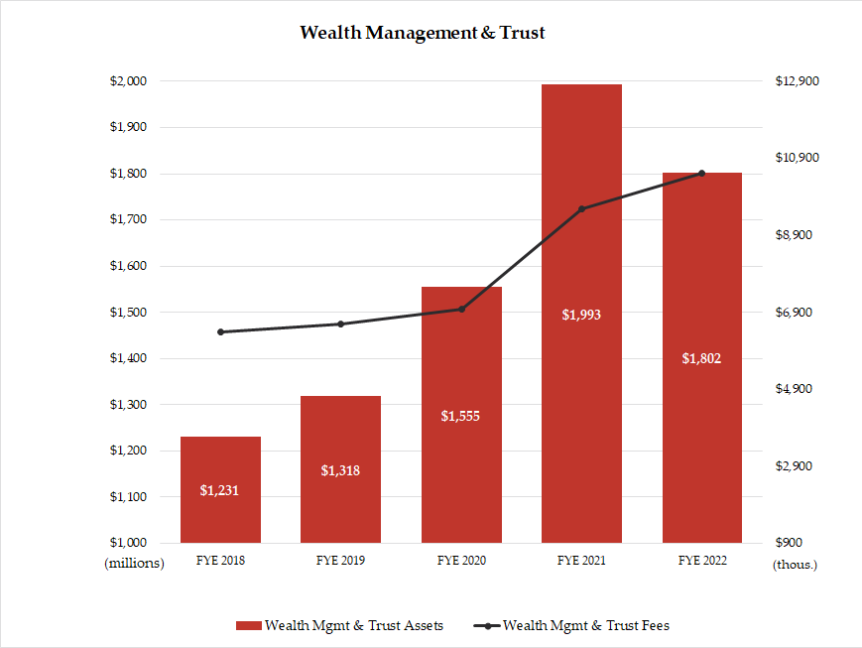

Wealth assets of $1.8B, down 10% from one year ago and impacted significantly by current market conditions

Wealth fees up 10% year over year

$191 MM in new wealth assets in 2022

Book value per share of $21.37 compared to $21.68 one year ago

Impacted by $12MM year-over-year downward ”mark to market” adjustment to the securities portfolio, or $2.51/share

$0.45/share dividend

Record date 12/15/22 and paid on 1/13/23

* For detail on significant items, please see Reconciliation of GAAP Results to Adjusted Results below.

Letter to Shareholders

Oakworth began 2022 with an intentional focus on positioning the company to export our unique business model to additional dynamic markets in the Southeast. Based upon the recent success we have experienced in Middle Tennessee (Nashville), we are encouraged to seek other markets with similar characteristics. The Oakworth approach resonates with our target market of closely held businesses, professionals and successful families. We continue to reach new clients and expand our service to existing clients in our more mature markets (Central and South Alabama). As you have likely seen, we announced our entry into the Central Carolinas and intend to open an office in the SouthPark Towers in Charlotte later this year. Our entry into a new market always begins with finding the right person in a market to lead our effort as we have done with Tim Beck in Central Carolinas.

As we expand, it is vitally important to maintain the distinctive level of service to which our clients have become accustomed. The Oakworth Way is our method of formalizing those behaviors that our clients say make their experience truly differentiated and consistent. We continue to relentlessly measure our client and associate satisfaction through objective measures like the Net Promoter Score (96), client retention (>95% since inception), and associate retention (96% in 2022). Further confirmation of associate satisfaction is being named the #1 Best Bank to Work For in the U.S. by American Banker for the 5th year in a row.

Additionally, we prioritize Safety and Soundness and being a well-capitalized institution. We are pleased to earn BauerFinancial’s 5-Star Rating in their most recent review.

2022 included some firsts for Oakworth. One of those was our entry into the subordinated debt market. We successfully raised $35 million in a well-received offering in August. Our reputation in the industry and our compelling story resulted in Oakworth receiving premium pricing relative to similar offerings. The proceeds of this debt offering will be used to support our continued growth moving forward.

We also invested in our infrastructure in 2022. As examples, we added a dynamic marketing professional who is already increasing our visibility and enhancing our ability to tell our story in a meaningful way. A data engineer joined us to provide leadership in effectively and efficiently leveraging our valuable data to gain further insight into our business and to serve our clients more fully.

- While we invested significant resources in our future, our team drove a 47% increase in core* earnings and a 34% increase in core* revenue while maintaining exceptionally high client and associate satisfaction.

- Profitability improved significantly with an 11.3% return on average equity, excluding significant items.*

- Revenue and profit growth were driven by growth in our balance sheet and adding new wealth relationships.

- Deposits increased 8%, in spite of industry trends to the contrary, and loans grew an exceptional 31%.

- Wealth assets ended the year at $1.8 billion and reflect nearly $200 million of new additions during the year.

- Our revenue mix remains favorable with 24% of revenue coming from non-interest fee income.

- Our net interest income benefitted from an expanding net interest margin throughout the year and from the significant loan growth noted earlier.

As we enter 2023, our fourth quarter net interest margin (NIM) was 3.68% compared to full 2022 NIM of 3.38%. While deposit costs are increasing across the industry, this beginning run rate along with continued expectations of double-digit loan growth bode well for revenue growth this year. With zero non-accrual or non-performing loans and no charge-offs in 2022, we are confident in the quality of our loan portfolio entering 2023.

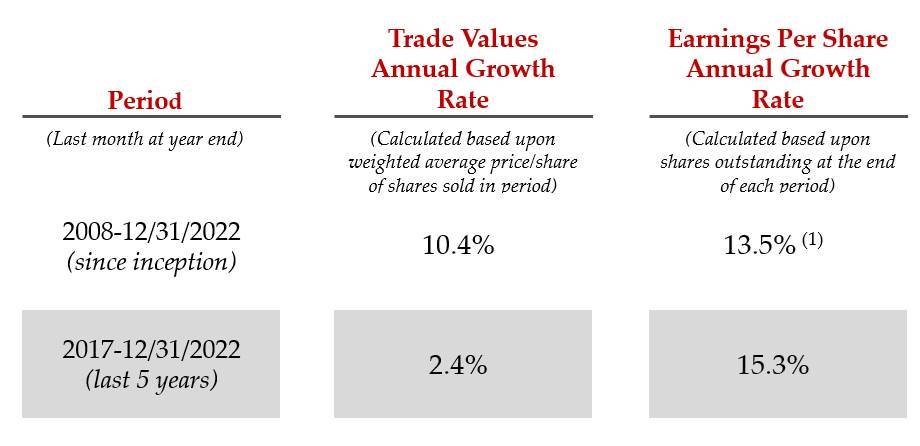

Recently, I have fielded some questions about the trade values of Oakworth stock (OAKC). Earnings is the fundamental driver of value for a company and trade values will (or should) reflect similar increases over time. That is apparent in the “since inception” figures shown in the chart below. It is also apparent that while EPS has accelerated over the past five years, the trade value has not tracked a similar growth rate. The very good news is that over time, trade values and earnings will approximate the same rates. Our efforts to move the trading of stock to the OTCQX should help. We will go through a natural transition phase in this move, but we firmly believe that this is a very good move for all shareholders. We are becoming more visible across markets and have taken steps to educate the broader markets regarding our successful financial results, future expectations of growth and the fact that OAKC is available for sale via the OTCQX Best marketplace.

Recently, I have fielded some questions about the trade values of Oakworth stock (OAKC). Earnings is the fundamental driver of value for a company and trade values will (or should) reflect similar increases over time. That is apparent in the “since inception” figures shown in the chart below. It is also apparent that while EPS has accelerated over the past five years, the trade value has not tracked a similar growth rate. The very good news is that over time, trade values and earnings will approximate the same rates. Our efforts to move the trading of stock to the OTCQX should help. We will go through a natural transition phase in this move, but we firmly believe that this is a very good move for all shareholders. We are becoming more visible across markets and have taken steps to educate the broader markets regarding our successful financial results, future expectations of growth and the fact that OAKC is available for sale via the OTCQX Best marketplace.

We thank you for your support and belief in our vision of Redefining Financial Services. We thank our associates for making all of the results I reported to you possible.

Sincerely,

Chairman and CEO