TRUMP’S FIRST TERM EFFECTS

Whether you agreed with his policies or not, the stock market loved Trump during his first term in office. The S&P 500 grew at a blistering clip of 64% during his first presidency, averaging roughly 16% per year.1 Tech stocks led the charge, soaring 166%, while Bitcoin posted an eye-popping 3,000% jump.1 Though the

U.S. dollar weakened in relative value, as seen by the DXY index, that wasn’t surprising – and sounds familiar to those who have kept tabs on the U.S. dollar index so far this year.

The bond market, on the other hand, did not enjoy the same rally throughout Trump’s first term. Treasury yields were higher across the board by end of 2019 (excluding the COVID-era disruptions), signaling investor caution.2 The tax cuts proposed in the Tax Cuts and Jobs Act of 2017 appeared to increase investor appetite for risk, leading to a further selloff of bonds.3 It is my opinion that with lower corporate taxes and less regulation expected from the bill, relative value, as seen by the DXY index, the stock market surged. Meanwhile, Trump’s tariff uncertainty and growing deficits from expansive fiscal policies led to an

increase in Treasury issuance, putting downward pressure on bond prices and pushing yields even higher.4 To anyone following financial news during Trump 2.0, you can see the parallels.(5)

TRUMP RETURNS

That takes us to Trump’s 2024 re-election, giving him a second chance at many of the policies he dabbled with in his first term. One of his first moves was the “America First Trade Policy” memorandum, in which he addressed his administration’s desire to review and reassess the U.S. trade policy which emphasized reducing trade deficits, onshoring U.S. manufacturing and strengthening the country’s national security.6

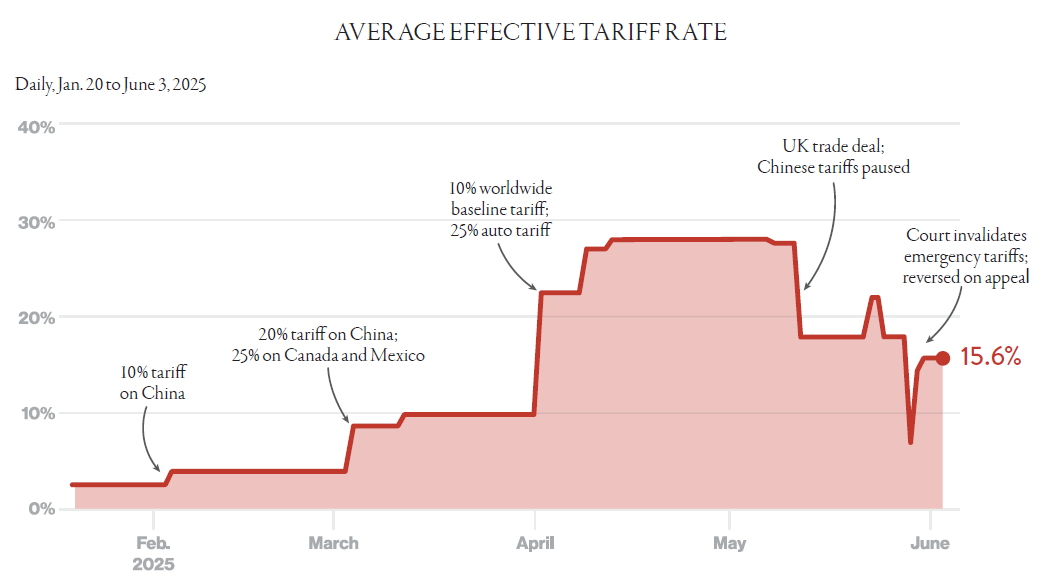

On February 1, he established a 25% tariff on imports from Mexico and Canada, then levied a 10% tariff on all Chinese goods.(7) Tariffs were paused briefly for negotiation, but when no deals were reached, they resumed on March 4. This prompted retaliation from Canada and China, while Mexico opted to continue negotiating.

Then came April 2 — “Liberation Day” — when Trump unveiled a slew of new tariffs across more than 180 foreign countries.8 A blanket 10% global tariff began on April 5. Then on April 9, more severe tariffs were activated for 57 of the United States’ major trading partners. Some highlights include:(8)

- 34% tariff on all goods from China

- 20% on all exports from the EU

- 24% on Japanese goods

- 25% on South Korean goods

Trump also doubled down on the EU, threatening an additional 25% increase on steel, aluminum and auto if no deal was struck before June 1.9 Throughout the following month, China and the

U.S. would appear to play a game of tariff chicken, culminating in a whopping 145% on all Chinese imports bound for the U.S. That is enough tariff talk to make any economist’s head spin. A deal was made with China around May 12 that set a 90-day truce on trade war escalation between the two countries, reducing the effective tariff rate from 145% to 30%. Meanwhile, Trump doubled the steel tariffs on the EU from 25% to 50%.9

So, who is paying for all of these tariffs?

Like all tough questions, the answer usually is: it depends. One of the factors at play is the type of product and who is using it. Tariffs on intermediary goods— like steel — usually affect businesses more than consumers. The end consumer may see some change in prices, but it will largely — in the short term — be absorbed in the cost of goods sold. Inversely, some direct-to-consumer products, especially from China, already appear to be showing price increases. Chinese Amazon executives mention their largest sellers looking to increase prices directly for goods shipped to the U.S., while others have thought about pausing operations in the U.S. entirely while searching for less costly markets.10 Amazon executives have even proposed breaking the tariff costs out on the checkout page, showing exactly how much of the cost was passed along to the customer, although this was shut down by the Trump Administration.11 Walmart has also warned of direct price hikes, citing disruptions to supply chain operations.12

Official data has been mixed — but Federal Reserve surveys show many firms — from New York to Atlanta — have either passed or plan to pass tariff-related costs on to consumers, with about 20% passing on all costs associated with the tariffs.13

INFLATION

Usually, with price hikes come inflation worries. In June, the president of the Richmond Fed Thomas Barkin warned of renewed price pressure — though later clarified it wouldn’t rival recent inflation spikes.14 Despite his comments, recent PCE Price Index data shows that inflation continues to cool — with April’s reading of 2.2% the lowest since 2021 — and May inching up slightly to 2.3%. (15)

*Sources – Data: Budget Lab at Yale; Chart: Axios Visuals

Most members of the Fed Board of Governors do not believe we will see the impact of price hikes on the inflation reports.16 Moreover, some are looking toward “front loading” as an explanation, where consumers and purchasing managers were buying goods in excess in anticipation of tariffs going into effect. Evidence for this theory can be found in the US Retail Sales report for the month of April, which surged upward 1.7%.17

TRADE NEGOTIATIONS: A WORK IN PROGRESS

The only major economically impactful nation that Trump has signed a trade agreement with has been the UK. After softening some of the initial tariffs (28% to 10% on cars and adding maximum quota caps),(18) the U.S. was able to finalize a deal. Additionally, a 90-day truce with China proved to be a positive development, reducing the massive 145% tariffs to around 30%.(19)

- India appears to be the next likely trade deal candidate after PM Modi has met with Trump.

- Additionally, spokespeople in the administration have stated they are working with Japan, the EU, Canada, South Korea, Vietnam, and more. (20)

With the reciprocal July 9 tariff deadline looming large, Trump’s team is trying to ink deals as soon as possible to avoid another tariff shock. (5)

MARKET REACTIONS

As expected, markets have reacted sharply. Immediately after “Liberation Day” (April 2) markets went into a freefall. The S&P 500 fell 4.9%, while the Nasdaq dropped 6%, the worst day since 2020. The sectors that were the most impacted included the most import-heavy and tariff-sensitive industries, such as retail, tech, and small-caps.21 Yet the Nasdaq and S&P rebounded rapidly in May and June during the tariff pause — hitting all- time highs — and continued to push upwards.

It was a different story for bonds.

- Treasury yields spiked due to the unstable environment.(2)

- Longer-term yields increased due to higher long-term inflation expectations and were compounded by the market expectation of delayed rate cuts. (22)

- Furthermore, foreign investors began selling off their treasury holdings, causing prices to fall and yields to rise. (22)

Trump’s $4 trillion “One Big Beautiful Bill” seemed to fuel deficit concerns, worrying investors about new inflation risks and the overall financial health of the United States government. In practice, as long-term yields rise, so do borrowing costs. This affects businesses, especially small ones, as higher borrowing costs can flow directly to their bottom line. Consumers are often impacted too, with rising rates on mortgages and auto loans, which are often tied to long-term Treasury yields.

LOOKING AHEAD

Trump’s second term has reintroduced tariffs as a central policy tool, reshaping the global trade landscape. While intended to rebalance trade relationships and promote domestic manufacturing, the 2025 tariffs have introduced global volatility and uncertainty.23 While it remains to be seen just how much of an impact this will have on domestic businesses and consumers, the recent effects have been somewhat muted. The stock market seems to have proven surprisingly resilient, rebounding from initial shocks to reach record highs,21 but tariff-sensitive sectors continue to remain anxious.

Bond markets may reflect deeper concerns, with rising yields fueled by inflation fears and fiscal instability. Ongoing negotiations with key trade partners — including Japan, India, and the EU — highlight the foreign response to U.S. economic assertiveness and the careful equilibrium between protectionist policies and globalization. As we move into the second half of 2025, the success of Trump’s tariff strategy will hinge not only on diplomatic breakthroughs abroad, but also on the ability of the U.S. economy to remain resilient amid trade tensions.

The critical question is whether American businesses can absorb the short-term pressures before new agreements are secured — or if those pressures will continue to build until we see a red, white and blue explosion.

This content is part of our quarterly outlook and overview. For more of our view on this quarter’s economic overview, inflation, bonds, equities and allocations, read the latest issue of Macro & Market Perspectives.

SOURCES

- Y-Charts Nov 2016 through Nov 2020 – S&P 500

- US Treasury Yield Curve, Retrieved July 2025.

- The Wall Street Journal – Bond Market Sends Warning to Trump and Republicans on Tax Plans

- Seeking Alpha – The Impact of the Tax Cut on the Bond Market

- Tax Foundation – Trump Tariffs: Tracking the Economic Impact of the Trump Trade War

- The White House – America First Trade Policy

- The Wall Street Journal, July 2025 – Where Things Stand with Trump’s Tariffs

- The White House, July 7, 2025 – Fact Sheet: President Donald J. Trump Continues Enforcement of Reciprocal Tariffs and Ann ounces New Tariff Rates.

- AP News, June 3, 2025 – Trump’s Tariffs Have Launched Global Trade Wars. A Timeline of How We Got Here.

- Reuters – Exclusive-Chinese Sellers on Amazon to Hike Prices or Exit U. S. as Tariffs Soar

- Time, April 29, 2025 – In Fight with Bezos, White House Calls Amazon Showing Tariff Costs a ‘Hostile’ Act

- Investopedia – Who Is Paying for Trump’s Tariffs?

- CBS News – The Trump Tariffs Aren’t Causing U. S. Prices to Spike. Here’s Why.

- Reuters – Fed’s Barkin Says Tariffs Will Start Pushing Up Inflation

- Bureau of Economic Analysis: Personal Consumption Expenditures Price Index

- Reuters – June 24, 2025 – Powell Repeats Rate Cuts Can Wait as Fed Studies Tariff Impacts

- United States Census Bureau June 17, 2025 – Advance Monthly Sales for Retail and Food Services.

- The Guardian, May 8, 2025 – UK Politics: Tariffs Cut on UK Cars, Steel and Aluminum in US Trade Deal

- PBS News May 12 , 2025 – Dow Leaps 1,100 Points Following a 90-Day Truce in the U. S.-China Trade War

- PBS News, April 6, 2025 – Trump Advisers Say More than 50 Countries Have Reached Out for Tariff Talks with White House

- Y-Charts 2025 – S&P 500

- The Wall Street Journal July 8, 2025 – Treasury Yields Keep Rising Amid Tariffs Concerns

- EY, April 3, 2025 – What Are the Implications of US President Trump’s Reciprocal Tariffs on Global Trade

Advisory Services, including investment management and financial planning, are offered through Oakworth Asset Management LLC a registered investment advisor and is owned by Oakworth Capital Bank, Member FDIC. Investment products and services offered via Oakworth Asset Management LLC are independent of the products and services offered by Oakworth Capital Bank, and are not FDIC insured, may lose value, have no bank guarantee, and are not insured by any federal or state government agency. Because of the ownership relationship and involvement by Oakworth Asset Management LLC associates with Oakworth Capital Bank, there exists a conflict of interest to the extent that either party recommends the services of the other. Oakworth Asset Management LLC does not provide tax or legal advice. You should consult your tax advisor, accountant, and/or attorney before making any decisions with tax or legal implications. For additional information about Oakworth Asset Management LLC, including its services and fees, send for the firm’s disclosure brochure using the contact information contained herein or visit advisorinfo.sec.gov.

This communication contains general information that is not suitable for everyone and was prepared for informational purposes only Nothing contained herein should be construed as a solicitation to buy or sell any security or as an offer to provide investment advice. The information contained herein is based upon certain assumptions, theories and principles that do not completely or accurately reflect

any one client situation. This communication contains certain forward-looking statements that indicate future possibilities. Due to known and unknown risks, other uncertainties and factors, actual results may differ. As such, there is no guarantee that any views and opinions expressed herein will come to pass. Investing involves risk of loss including loss of principal. Past investment performance is not a guarantee or predictor of future investment performance.

Any reference to a market index is included for illustrative purposes only as it is not possible to directly invest in an index. The figures for each index reflect the reinvestment of dividends, as applicable, but do not reflect the deduction of any fees or expenses, the incurrence of which would reduce returns. It should not be assumed that your account performance or the volatility of any securities held in your account will correspond directly to any comparative benchmark index. This communication contains information derived from third party sources. Although we believe these sources to be reliable, we make no representations as to their accuracy or completeness.

All opinions and/or views reflect the judgment of the authors as of the publication date and are subject to change without notice.