At the beginning of the 2nd quarter, many people questioned how things could get any more chaotic than they were in the first. It didn’t take long to find out.

On April 2, speaking from the White House Rose Garden, President Trump announced a broad slate of tariffs on the remainder of the world. The larger the U.S. trade deficit with an individual country, the higher the tariff. Everyone, however, got at least a 10% tariff, as the president exercised authority under the International Emergency Economic Powers Act of 1977.

Let’s just say the markets’ reaction wasn’t very positive. In fact, the U.S. stock market, as defined by the S&P 500, fell from 5,670.97 at the close of trading on April 2 to 4,982.77 at the end of April 8. That is roughly a 12.13% principal decline over four trading sessions.(1) Obviously, that wasn’t a lot of fun.

Then came the waiting game.

We spent the remainder of the quarter agonizing over tariff announcements, parsing the president’s social media posts and speculating about the Federal Reserve’s next move. Would it cut the target overnight lending rate again? If not if, then when?

Unfortunately for those wanting an immediate rate cut, the economic data during the quarter wouldn’t cooperate. The numbers were just a little too strong. The official unemployment rate best illustrates this, which was 4.2% at the start of April and 4.1% at the end of June.(2)

Inflation, as defined by the trailing 12-month Consumer Price Index (CPI), came in at 2.4% in March, 2.3% in April and 2.4% in May 2025. While those numbers are much better than the peak of 9.1% back in June 2022, they still aren’t as low as the Fed-desired 2% target.(3)

Then, as if all of this weren’t maddening enough, the Israelis started bombing Iran on June 13, 2025. The Iranians quickly retaliated, and for a moment, it appeared as though the world might be on the cusp of a major meltdown. In a surprising turn, however, on June 22, the United States joined the conflict by striking several key Iranian nuclear sites, and the situation deescalated shortly afterward.

Whew. Given all the turmoil, you’d expect investors to be anxious and rattled — but you’d be wrong.

When the dust settled and smoke cleared at the end of June, the S&P 500 had reached an all-time high of 6,204.95 — marking a principal return of roughly 10.56% for the 2nd quarter of 2025.1 On the flip side, crude oil prices, as defined by the Generic 1st Crude Oil WTI futures contract, actually declined during the quarter. That isn’t what one might have expected, given all the geopolitical uncertainty.4

In the end, it wasn’t just the craziness of what was happening in the world that made the 2nd quarter of 2025 so unusual. It was how investors responded to it. Regardless, whether everything and everyone was crazy or not, few people complain when the major U.S. stock indices generate positive results.

Thank you for your continued support.

John Norris

Chief Investment Officer

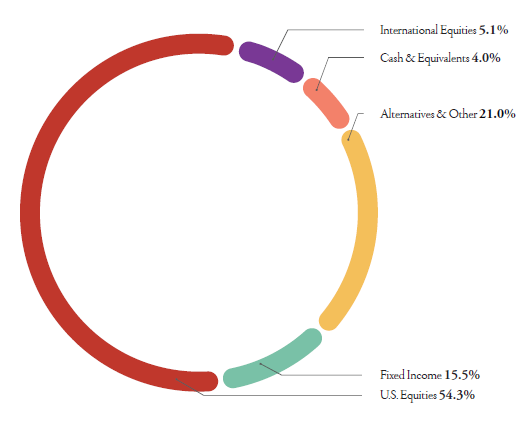

Our Investment Committee distributes information on a regular basis to better inform our clients about pending investment decisions, the current state of the economy and our forecasts for the economy and financial markets. Oakworth Capital currently advises on approximately $2.37 billion in client assets. The allocation breakdown is in the chart below.

SOURCES :

- Federal Reserve Bank of St. Louis – S&P 500

- U.S. Bureau of Labor Statistics – The Employment Situation

- Federal Reserve Bank of Richmond – The Origins of the 2 Percent Inflation Target

- MarketWatch, 2025 – Crude Oil WTI (CL.1)

This content is part of our quarterly outlook and overview. For more of our view on this quarter’s economic overview, inflation, bonds, equities and allocations, read the latest issue of Macro & Market Perspectives.

Advisory Services, including investment management and financial planning, are offered through Oakworth Asset Management LLC a registered investment advisor and is owned by Oakworth Capital Bank, Member FDIC. Investment products and services offered via Oakworth Asset Management LLC are independent of the products and services offered by Oakworth Capital Bank, and are not FDIC insured, may lose value, have no bank guarantee, and are not insured by any federal or state government agency. Because of the ownership relationship and involvement by Oakworth Asset Management LLC associates with Oakworth Capital Bank, there exists a conflict of interest to the extent that either party recommends the services of the other. Oakworth Asset Management LLC does not provide tax or legal advice. You should consult your tax advisor, accountant, and/or attorney before making any decisions with tax or legal implications. For additional information about Oakworth Asset Management LLC, including its services and fees, send for the firm’s disclosure brochure using the contact information contained herein or visit advisorinfo.sec.gov.

This communication contains general information that is not suitable for everyone and was prepared for informational purposes only Nothing contained herein should be construed as a solicitation to buy or sell any security or as an offer to provide investment advice. The information contained herein is based upon certain assumptions, theories and principles that do not completely or accurately reflect

any one client situation. This communication contains certain forward-looking statements that indicate future possibilities. Due to known and unknown risks, other uncertainties and factors, actual results may differ. As such, there is no guarantee that any views and opinions expressed herein will come to pass. Investing involves risk of loss including loss of principal. Past investment performance is not a guarantee or predictor of future investment performance.

Any reference to a market index is included for illustrative purposes only as it is not possible to directly invest in an index. The figures for each index reflect the reinvestment of dividends, as applicable, but do not reflect the deduction of any fees or expenses, the incurrence of which would reduce returns. It should not be assumed that your account performance or the volatility of any securities held in your account will correspond directly to any comparative benchmark index. This communication contains information derived from third party sources. Although we believe these sources to be reliable, we make no representations as to their accuracy or completeness.

All opinions and/or views reflect the judgment of the authors as of the publication date and are subject to change without notice.