I wish I could say, “What a great quarter to unplug from the markets.” But the 2nd quarter of 2025 seemed to be one of the more exhausting in recent memories — at least dating back to the mini banking crisis of 2023, or even the onset of COVID. However, given the nature of what we do, unplugging simply is not an option!

The 2nd quarter, while exhausting, was ripe with opportunities. Volatility is a gift to long-term focused investors and that is exactly what we are. The quarter essentially kicked off with the “Liberation Day” tariff announcement from the president and wrapped up with a full-on war between Israel and Iran (with the help of the United States).

POSITIONING & REBALANCING

In looking back on our allocations for the 2nd quarter, I would be remiss if I didn’t recap the moves our Investment Committee made in the 1st quarter. The theme to start the new year was flexibility. For us, that meant minimizing portfolio volatility without fully exiting the equity markets. This included

reducing our tech allocations and, more notably, small-cap stocks selections. As the volatility around Liberation Day unfolded, countless times I found myself saying, “We expected volatility to pick up — just not to this extent.” However, in my opinion, it matters less in the markets that you are right for the right reasons, and more just that you are right. And in this case, our expectations were accurate and volatility did pick up.

We entered the second quarter with a more defensive posture than in recent years — reducing equity exposure and exiting some of the more volatile positions in order to lower overall portfolio risk. When markets fall under pressure, small- cap equities may tend to amplify negative headlines with heightened volatility.

The pullback following the tariff announcement was swift — followed closely by an equally fast market rebound. This activity gave us an extremely narrow window to act. The drop created a unique opportunity to act on the dry powder and flexibility we had created in the 1st quarter by adding to domestic large-cap equities. While the metaphorical baby was being thrown out with the bath water, the sharp reduction in multiples almost overnight seemed to be too good for us to pass up and as a result, we got to work buying.

EQUITIES AND FIXED INCOME

As a result, we decreased our short-term fixed income weighting (which had been added to in the 1st quarter) and brought our equity weighting back up close to neutral from a slight underweight. Even with the market’s recent bounce back, there may still be some real concerns hanging over the market. We don’t feel the economy is falling off a cliff, but in our opinion, it’s clearly not hitting on all cylinders. This puts a high bar on where earnings need to go from here to justify current valuations. While the pullback gave us a chance to get in at better prices, the road ahead still seems uncertain. It has typically been a market that has rewarded patience, solid fundamentals and maybe a bit of caution, too.

There is an old saying that markets tend to take the elevator down and the stairs up. But in recent years, we have seen evidence that the market can take the elevator both ways: the sharp decline in the markets unfolded over just a few days, with the rebound coming just as quickly.

INTERNATIONAL POSITIONING

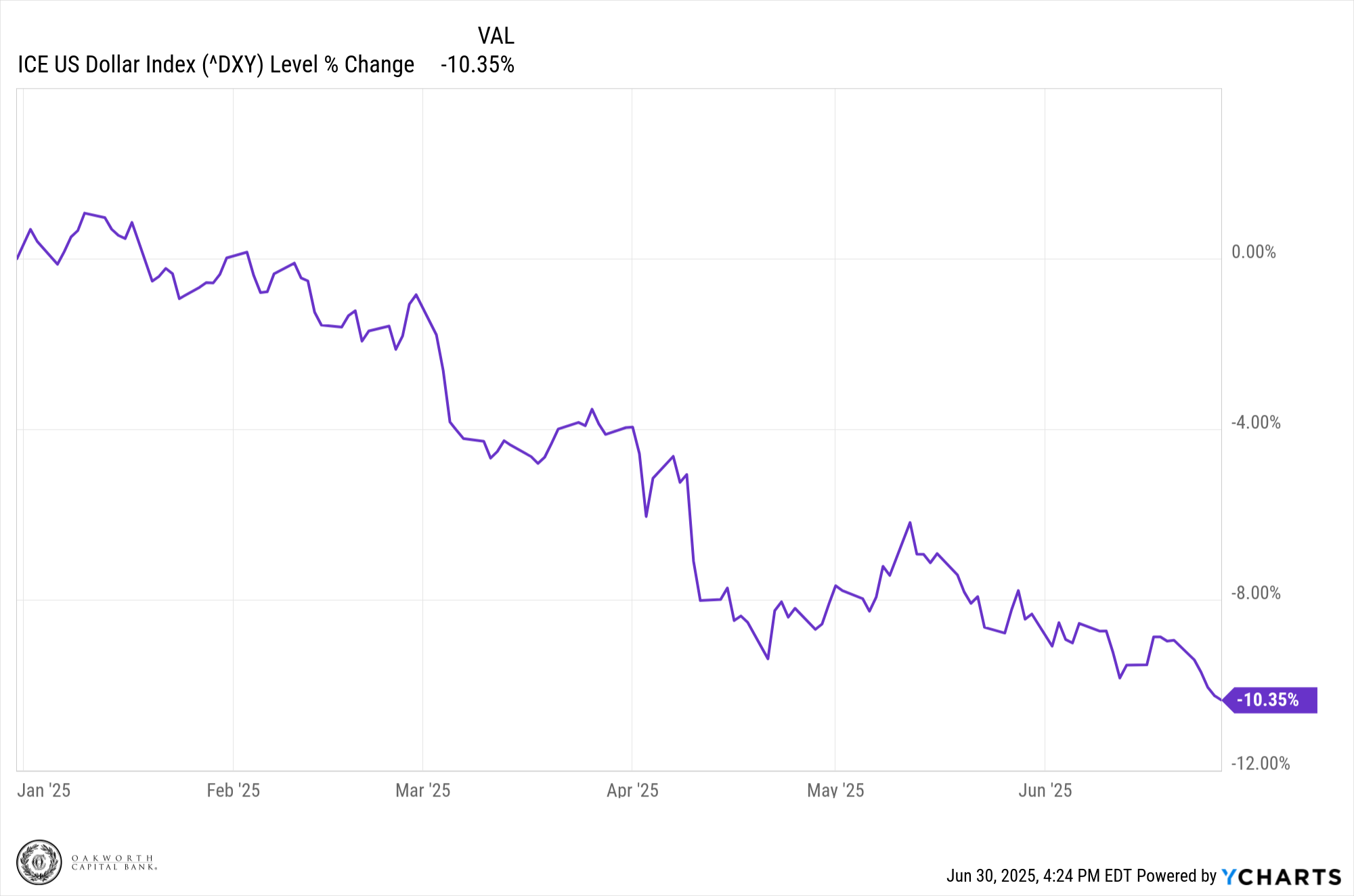

Another subtle theme of the 2nd quarter was continued weakness in the U.S. dollar, beginning in Q1 and ending the halfway mark down roughly 10%. International equities, which outperformed in Q1, continued to benefit throughout the 2nd quarter. In response, we reduced our underweight to international exposure – though carefully.

We continue to maintain our opinion that domestic markets offer more long-term potential, but in the short term, international equities have outperformed — supported by a weaker dollar and increased stimulus, largely in western Europe.

THE DOLLAR CONTINUES TO DIP

FIXED INCOME

Fixed income continues to be the ballast of our portfolios. We don’t like to expose ourselves to risk in this space so we have continued to maintain a high-quality, short-duration portfolio that continues to benefit from elevated yields as the Federal Reserve continues to hold off on rate cuts.

LOOKING AHEAD

While we are biased toward equities in the long run, the short-term outlook is more complex. Headwinds such as a softening economy and elevated earnings expectations have created an environment where we still value flexibility and optionality. Our additions to equities in our portfolios in Q2 were thoughtfully made with a long-term view that also understands these headwinds.

We may not have expected the volatility to be as significant as it was in the 1st quarter, but it served as a powerful reminder of the benefit of dry powder. We still have a cautious view of what the remainder of the year is going to look like and will adjust our portfolios in both directions, depending on which way the volatility goes. As always, we will continue to focus on what the future holds and how that forecast may impact our clients’ portfolios. While there seem to be many unknowns this year, there is still plenty to be optimistic about. Our team will stay laser focused on capturing opportunities as they present themselves.

This content is part of our quarterly outlook and overview. For more of our view on this quarter’s economic overview, inflation, bonds, equities and allocations, read the latest issue of Macro & Market Perspectives.

Advisory Services, including investment management and financial planning, are offered through Oakworth Asset Management LLC a registered investment advisor and is owned by Oakworth Capital Bank, Member FDIC. Investment products and services offered via Oakworth Asset Management LLC are independent of the products and services offered by Oakworth Capital Bank, and are not FDIC insured, may lose value, have no bank guarantee, and are not insured by any federal or state government agency. Because of the ownership relationship and involvement by Oakworth Asset Management LLC associates with Oakworth Capital Bank, there exists a conflict of interest to the extent that either party recommends the services of the other. Oakworth Asset Management LLC does not provide tax or legal advice. You should consult your tax advisor, accountant, and/or attorney before making any decisions with tax or legal implications. For additional information about Oakworth Asset Management LLC, including its services and fees, send for the firm’s disclosure brochure using the contact information contained herein or visit advisorinfo.sec.gov.

This communication contains general information that is not suitable for everyone and was prepared for informational purposes only Nothing contained herein should be construed as a solicitation to buy or sell any security or as an offer to provide investment advice. The information contained herein is based upon certain assumptions, theories and principles that do not completely or accurately reflect

any one client situation. This communication contains certain forward-looking statements that indicate future possibilities. Due to known and unknown risks, other uncertainties and factors, actual results may differ. As such, there is no guarantee that any views and opinions expressed herein will come to pass. Investing involves risk of loss including loss of principal. Past investment performance is not a guarantee or predictor of future investment performance.

Any reference to a market index is included for illustrative purposes only as it is not possible to directly invest in an index. The figures for each index reflect the reinvestment of dividends, as applicable, but do not reflect the deduction of any fees or expenses, the incurrence of which would reduce returns. It should not be assumed that your account performance or the volatility of any securities held in your account will correspond directly to any comparative benchmark index. This communication contains information derived from third party sources. Although we believe these sources to be reliable, we make no representations as to their accuracy or completeness.

All opinions and/or views reflect the judgment of the authors as of the publication date and are subject to change without notice.