After a tumultuous start to the year, the 2nd quarter of 2023 occasionally felt like a collective sigh of relief. Unfortunately, it often felt like déjà vu all over again, too. In its entirety, this past quarter was arguably a little less bumpy than the 1st, but still a bouncy ride.

The news that caused the greatest angst, gnashing of teeth and wringing of hands was the theater surrounding the debt ceiling.

That Washington would eventually come to some sort of compromise was a foregone conclusion, or should have been. After all, the global economy would come to a screeching halt if the U.S. Treasury were to default on its debt.

Essentially, economic reality trumps political rhetoric, as it should.

Other than that, the bank woes from the start of the year faded to the back pages but are still an issue. The war in Ukraine is over a year old, and the Unites States hasn’t been sucked into the quagmire like most initially feared. Headline inflation numbers have been heading in the right direction, but prices still remain high at the grocery. The Federal Reserve probably isn’t completely done raising rates, but is much closer to the end than the beginning.

In essence, a lot of the bricks in our proverbial wall of worry didn’t seem quite as worrisome this past quarter.

By the time the dust settled, the smoke cleared and the cows came home, investors mostly made money during the 2nd quarter. This even though not all that much fundamentally changed. Regardless, as we all know, making money is basically the name of the game.

So, as we start the 3rd quarter of 2023, let me recap:

- The economy is doing better than it probably should be.

- The labor market remains strangely tight.

- On the other hand, the yield curve remains inverted.

- Banks are slowing down the extension of credit.

However, all told, it appears as though that worst-case scenario, a return to 2008, isn’t going to happen. I suppose that alone is enough to make people feel a little bit better about things.

Thank you for your continued support,

John Norris

Chief Economist

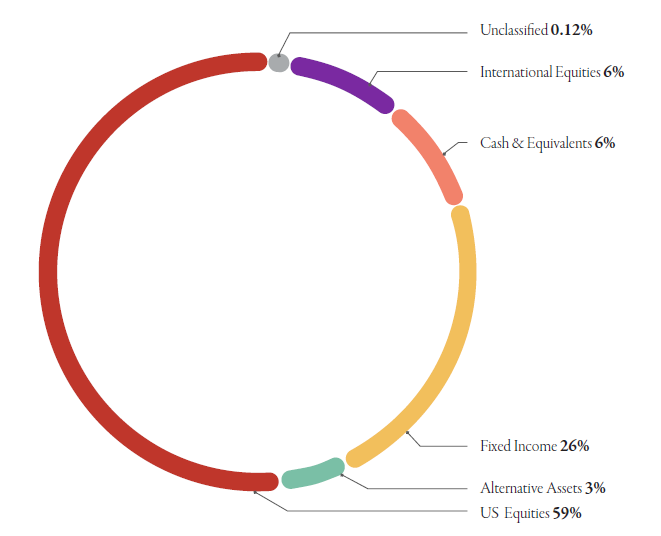

Our Investment Committee distributes information on a regular basis to better inform our clients about pending investment decisions, the current state of the economy and our forecasts for the economy and financial markets. Oakworth Capital currently advises on approximately $1.9 billion in client assets. The allocation breakdown is in the chart below:

The opinions expressed within this report are those of the Investment Committee as of the date published. They are subject to change without notice, and do not necessarily reflect the views of Oakworth Capital Bank, its directors, shareholders or employees.

This content is part of our quarterly outlook and overview. For more of our view on this quarter’s economic overview, inflation, bonds, equities and allocation read our entire 2nd Quarter 2023 Macro & Market Perspectives.