This morning, the Bureau of Labor Statistics (BLS) announced the U.S. economy created 150K net, new payroll jobs during October 2023. Of these, only 99K were in the private sector. Both of these observations were less than expected, with the private payroll number being especially soft. They weren’t dreadful, just the economic equivalent of a MoonPie when you were hoping for a fresh eclair.

For its part, the Unemployment Rate ticked up slightly to 3.9%. While still miserly by historical standards, it was been trending higher from the 50-year low of 3.4% in January earlier this year. Like the payroll number, it wasn’t awful, just the equivalent of an RC Cola when you were hoping for a cup of Ethiopian (Yirgacheffe) coffee.

Ah…an RC Cola and a MoonPie. The legendary “working man’s lunch” here on an Employment Friday. To that end, I have always thought MoonPies must have been much bigger back in the day. One isn’t lunch for an 8-year old today, let alone a working man.

Unemployment and the Gig Economy

I am going to step out on a pretty long limb here and predict that the Unemployment Rate is going to continue to creep up. Sure, there are like a zillion job openings in the economy. However, when push comes to shove, more people are going to be without what Charles Dickens would have called “a situation.”

The reason being is pretty simple. The gig economy is going to slow down significantly.

My crystal ball is crystal clear on this.

As I have written in this blog in the past, Pew Research estimates some 3-5 million Americans participate in the gig economy as their primary source of income. And why not? It is a pretty sweet deal for a lot of modestly skilled, former hourly workers.

Shoot. Do you want to have a set schedule working for “the man” making, say, $12/hour? Or would you rather set your own schedule, and potentially make more money, making some deliveries? Carting a few folks around?

You might be saying, if not screaming, I am nuts. Are people really going to stop taking an Uber or Lyft? Not order delivery through Grubhub or DoorDash? That stuff is here to stay, right?

Don’t get me wrong. People will continue to use these apps. They just won’t use them as much.

After a couple of years of higher inflation, higher interest rates and overall higher cost of living, folks are going to be more mindful about cutting, shall we say, unnecessary expenditures. It is about time.

As a result, paying up for convenience will be on the chopping block in a lot of houses. I know it is in mine. Let me give you a good example, at least I think it is good, of what I mean.

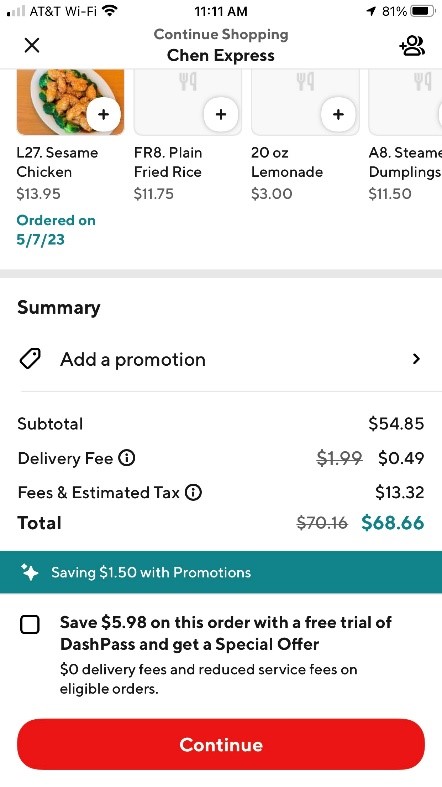

There are a couple of Chinese restaurants in my zip code which offer delivery to my house. While I think them to be virtually indistinguishable, my wife prefers one over the other. I will call this restaurant Chen Express.

We might be the exception, but we tend to over order every time we get Chinese food. We justify it by saying we will take the leftovers for lunch. Unfortunately, a lot of it usually ends up in the garbage can. Regardless, here is a typical order: large hot and sour soup, two egg rolls, sesame chicken and kung pao special dish (beef, shrimp and chicken).

According to the menus on the website, this meal should set us back right at $44 with tax, prior to tipping the delivery driver. Obviously, that is a decent sum of money, but we don’t do this very often. Now, what do you think it would be over on DoorDash?

Drum roll please…

$68.66.

Caveat. I made and cancelled this order at 11:11 am CDT on November 2, 2023. Prices can and will vary in the future.

There is nothing underhanded or mysterious about this comparison, and it makes perfect sense. DoorDash is in business to make money, and it has to get it from somewhere. Ergo, the markup on the food and the nebulous “fees,” because I know what the sales tax rate is here.

So, there you have it. I can save, quite literally, $25 on this order simply by calling the restaurant directly and not using the app. If you need another example, compare buying a pizza using the Papa John’s app versus DoorDash. Or try Uber Eats or Grubhub if you like. It doesn’t make any difference, as the results will be similar.

You will find it is cheaper to go straight to the source. To be sure, these differences likely won’t be as great as my Chinese restaurant one.

However, the point remains. In 2024, consumers WILL be looking for easy ways to reduce expenses. This stuff I am discussing is so much low-hanging fruit.

To be sure, people could counter if enough people decide to order direct from the restaurant for delivery, people who were “DoorDashing” could just go work there instead. Perhaps, but wouldn’t that defeat the purpose, at least for the worker? After all, a huge part of the appeal of participating in the gig economy is the flexibility, the ability to set your own hours and not work for “the man.”

Interestingly, or stupidly, enough, I always knew I was paying a little something extra for the convenience of using one of the gig apps on my phone. However, and this is completely my fault, I didn’t fully appreciate exactly how much until relatively recently. As a result, I haven’t ordered anything off of DoorDash in a few months.

Clearly, I am just one person. However, what if there are millions of people, such as I, who have scaled backed on their unnecessary expenditures? Perhaps we could call it their laziness as measured in dollars?

Let’s just say it could have a pretty significant impact on the labor markets.

Labor Markets

While one month does not a trend make, the Labor Force Participation Rate for U.S. workers over the age of 25 with “less than a high school diploma” jumped to 47.9% in October from 46.9% in September. Although a lot of these new entrants into the labor market found jobs, a lot didn’t and the Unemployment Rate for this demographic segment increased from 5.5% to 5.8%.

What’s more, since July 2023 the Unemployment Rate for this group has increased by 0.6%. Over that same time frame, the rate has spike from 3.4% to 4.0% for U.S. workers who are “high school graduates, no college.” Essentially, it is going up the fastest for our unskilled and semiskilled workforce.

If this is already occurring, what will happen if there isn’t enough gig work to pay the bills? That’s right, a lot of these workers, who probably aren’t adequately tracked or otherwise accounted for in the data, will have no choice but to reenter the official workforce.

Many will find jobs, but many will not.

Boom.

This will cause the Unemployment Rate to continue to trend higher, which could impact the Fed’s decision making process towards the second half of 2024.

The question won’t be whether to cut the overnight not or not. No, it will be how many times to cut if the Unemployment Rate gets into the mid-4%.

In the End

If you don’t like higher inflation, higher interest rates and overall higher cost of living, let me make a recommendation: quit using your phone to get stuff delivered to your door. Don’t order the extra drink at dinner, or one at all, and drive yourself to the restaurant. Not only will you be saving money, you will be contributing to higher levels of the officially unemployed. THIS will drive down wage inflation and interest rates.

In the meantime, instead of taking your leftovers from the Chinese restaurant, consider taking an RC Cola and a MoonPie for lunch. While not a terribly healthy meal, you will also start losing weight and people will view you as a “working man.”

There is a certain level of panache to that these days.

Thank you for your continued support. As always, I hope this newsletter finds you and your family well. May your blessings outweigh your sorrows on this any every day. Also, please be sure to tune into our podcast, Trading Perspectives, which is available on every platform.

John Norris

Chief Economist

Please note, nothing in this newsletter should be considered or otherwise construed as an offer to buy or sell investment services or securities of any type. Any individual action you might take from reading this newsletter is at your own risk. My opinion, as those of our Investment Committee, is subject to change without notice. Finally, the opinions expressed herein are not necessarily those of the rest of the associates and/or shareholders of Oakworth Capital Bank or the official position of the company itself.