It wasn’t that long ago, or so it seems, that bonds and fixed income were referred to, by many financial gurus, as an “afterthought” of an asset class. It’s just a mind-numbing, mathematical-based contraption used to reduce risk in a portfolio, and offer limited returns, right? Now, however, fixed income – ranging from corporate bonds to U.S. treasuries – are receiving some overdue love and attention from both Wall Street and retail investors. What once was a safer but boring asset class, is now a safer, yet cunning, investment.

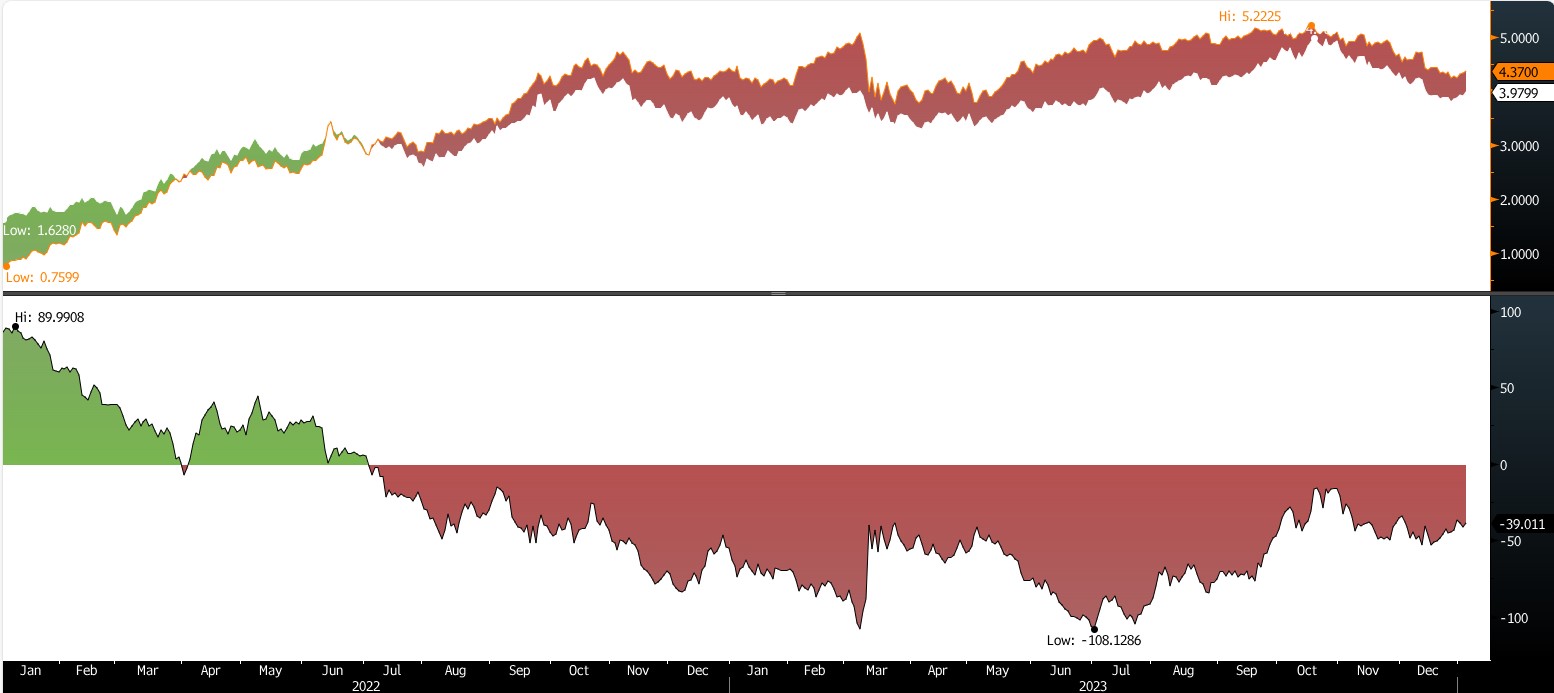

Media’s news cycles and headlines are curious. In a matter of hours, social media posts can spread headlines and make “trending” topics rise to the surface for all to see. The phrase “yield curve inversion” popped onto the scene over a year and a half ago and, while headlines fade, the inversion has persisted. Since July of 2022 the 2-year treasury yield has dipped – and remained – below the yield of the 10-year treasury yield.

Inverted is used to describe a situation where yields on long-term bonds (the 10-YR) are longer than short-term bonds (the 2-YR). This imbalance from the norm, where the short end of the yield curve offers a smaller yield than the longer end, has historically been a warning sign that the economy is in a risky place, oftentimes a foreboding of a recession.

As shown in the graph below, the inversion was at its largest depth on July 3rd of this year with an astounding -1.08% spread between the 2 and 10-year yields. This represents the widest margin since September of 1981 when double digit inflation was weighing on the country and the economy slipped into a recession for the next 17 months. This all sounds scary, but as we swivel our heads around and take into account all other indicators and the state of the U.S. economy, the current backdrop is not the one we knew in the late 70’s and early 80’s, in part due to the work the Federal Reserve has done to carefully handle the post-Covid inflationary period.

Source: Bloomberg Financial

Source: Bloomberg Financial

After the most aggressive Fed Fund rate hike cycle in history, it should come as no surprise that we have experienced the longest uninterrupted 2/10-year yield inversion in history. As rates have risen, bond prices have fallen due to the inverse relationship between prices and yields. Shorter term rates will move more closely with the Fed’s overnight borrowing rate, or the Fed Funds rate, than longer-dated bonds. As economic outlook turns bleak, investors flock towards longer-dated fixed income to lock in safety and avoid reinvestment risk. That is, until an event or catalyst strikes, causing money managers to react quickly and address the sudden emergence of risk. Just this past March, we saw such an event rattle markets as Silicon Valley Bank fell. Within a week, the 2-year treasury yield plummeted from 5.08% to 3.72% displaying the fragility of financial markets as investors dashed to safety.

“2024 will not be a repeat of 2022 …we hope”

Speaking of headlines, “The 60/40 portfolio had its worst year since 1937” was not a fun one to walk through in 2022. As the euphoria of cheap money wore off and inflation began to permeate the economy, monetary tightening was needed to ensure price stability. But with that comes a cost on almost every asset class, and the generally “safe” fixed income class even plummeted in 2022. With increasing rates, came lower bond prices. 2024, however, offers a much different backdrop.

- Inflation has cooled.

- The consumer is feeling the effects of 8% mortgage rates and 10% car loans.

- Even the U.S. Government will need relief in servicing its $3+ Trillion of additional debt issued in 2023.

Easing is on the way. At least that’s what markets were pricing in to end the 2023 calendar year. The U.S. economy should be entering a much different season with declining rates and, possibly, see investor’s f locking to safer assets. The once “boring” bonds may be turning a new leaf in 2024, with higher yields than what recent history has offered and desirable price appreciation.

CASH IS KING

Historically, cash has been “dry powder” for a portfolio, at best. Up until mid-2022, cash was paying nothing, and that’s not an exaggeration. But with rising rates came higher yields on cash sweeps and money markets. And just like that, cash becomes king. When there’s a 5% yield on cash, lets call it what it is, an asset class. Or at least a sub-class of fixed income. Although cash will not carry principal appreciation potential, investors seeking income to pay for living expenses with zero downside risk found their ideal investment for 2023. We raised cash in our portfolios with all of this in mind.

However, we have been careful to not over stay our welcome in cash, even if yields on the sub-asset class remain in higher than- historical averages. It is important to remain nimble and focus a gaze on the horizon in the investment management line of work. With that in mind, towards the latter half of 2023, the Investment Committee began putting cash to work with a key objective in mind – maintaining a solid yield while creating some principal appreciation opportunity.

We started allocating some of the cash towards the short end of the curve. We viewed this as a tactic to lock in Fixed Income yields comparable to those of 2007, particularly as inflation slows and the Fed begins rolling out rate cuts. Keep in mind, with decreasing yields comes increasing prices, so “buying low”, picking up yield, and “selling high” could be in store for those looking to increase their Fixed Income allocations in 2024.

The opinions expressed within this report are those of the Investment Committee as of the date published. They are subject to change without notice, and do not necessarily reflect the views of Oakworth Capital Bank, its directors, shareholders or employees.

This content is part of our quarterly outlook and overview. For more of our view on this quarter’s economic overview, inflation, bonds, equities and allocation read our entire Annual 2023 Macro & Market Perspectives.