Social media has emerged as a powerful force in investing and political engagement. What began as a way of keeping up with friends and family online has evolved into a platform that can guide individuals into speculative “investing”. Retail trading surged after brokerage firms introduced zero-commission based trading in 2019. This decision democratized access to stock markets, enabling individual investors to actively trade in capital markets, specifically equity markets, which was previously dominated by institutional players. Once trading became a popular “past time”, it didn’t take long for the masses to share their trading ideas and strategies on social media sites.

Additionally, it didn’t take long for Aunt Sue to stir up political opinions on her favorite social media platform. Beyond that, social media posts, advertisements, and bots have been targeted by both political parties as “election interference.”

U.S. elections have shed light on the integrity of democratic processes, as platforms increasingly serve as conduits for misinformation and strategic manipulation.

Undoubtedly, social media has transformed retail trading behaviors, resulting in interesting and sometimes frustrating market movements, while also making it difficult to decipher the truth during heightened electoral periods.

THE RISE OF RETAIL INVESTING AND SOCIAL MEDIA

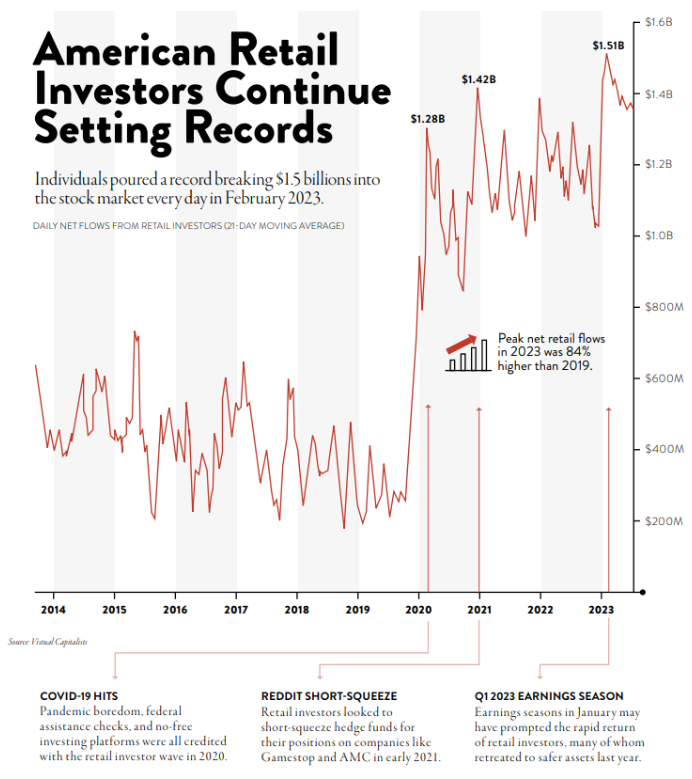

The arrival of zero-commission brokerage trading, initially made popular by platforms like Robinhood, has significantly lowered the barriers of entry for retail investors. The growth of low-cost trading coincidently expanded in the months leading up to the surge of stay-at-home trading during the COVID-19 pandemic. Lockdowns and the distribution of stimulus checks catalyzed an influx of new traders into the market, many of whom sought to capitalize on market volatility, and many of whom were just bored. Social media platforms, particularly Reddit and Twitter, emerged as primary venues for sharing investment ideas and strategies, leading to the phenomenon known as “meme stocks.”

MEME STOCKS AND INVESTMENT TRENDS

Meme stocks, the most popular being GameStop (GME) and AMC Entertainment holdings (AMC), became symbols of a new era in retail trading, fueled by social media narratives similar to that of the Robinhood legend of “seizing from the rich and powerful.”

Hedge funds will, from time to time, short stocks (borrowing shares to then sell at the current price, with an expectation that the price will drop, and then buying them back at the lower price to return to the owner) of companies they believe are entering a challenging environment. In early 2021, it was discovered that two favorites of the social media crowd, GME and AMC, were being heavily shorted by large institutions. What began as retail trading quickly turned into something more than just a quick profit. All of a sudden, an entire online community shifted its focus, taking a stand against powerful institutional players. Retail traders pursued a “hold the line” movement in a virtuous attempt to save GME and AMC stock.

Phrases like “HODL,” an acronym born from a misspelled forum post advocating to hold assets for the long term, and “diamond hands,” symbolizing steadfast conviction despite volatility, quickly became mantras of the community. Both depicted the ethos of this Robinhood-like movement that led to an over 371% pop in GME and a 531% surge in AMC within a few trading days. The WallStreetBets community on Reddit, spearheaded by influencers like Keith Gill (online forum name: Roaring Kitty), utilized memes to humorously and creatively promote these stocks, which sparked a buying frenzy and created the astronomical price increases mentioned earlier. This grassroots mobilization highlighted the power of social media in shaping abnormal and irrational investment behaviors within market trends.

There are two sides to every coin, though.

It is one thing if hedge fund managers fundamentally believe economic headwinds will present monetary challenges for a company and then attempt to profit from a possible drawdown. It is another thing when the social media induced-retail trading boom – largely focused on the buying and holding of heavily shorted stocks – is exploited by short sellers who use social media to disseminate negative sentiment about companies and utilize unauthenticated information in order to drive down prices.

A notable example is Globe Life. The firm Fuzzy Panda posted disparaging content that accused the insurance company of committing widespread fraud in April 2024. The allegations triggered others to sell or even further short the stock, which created artificial selling pressures and led to a 60% drop within a single day. The stock has nearly recovered all losses (at least at the time of this writing), but the pain was borne by shareholders for months. Such rapid spread of harmful (mis)information on social media can lead to swift shifts in investor sentiment, resulting in significant market impacts, particularly for smaller companies less equipped to withstand speculative attacks.

SOCIAL MEDIA’S INFLUENCE ON U.S. ELECTIONS

Social media has also presented separate, yet parallel, challenges in the political arena for several cycles now. While platforms provide political discourse and engagement, they can also facilitate the spread of misinformation and negative sentiment, often from accounts that do not belong to an actual human.

One of the most concerning aspects of social media’s dynamic in politics is the use of bot accounts – automated accounts designed to simulate human interaction and amplify specific messages via mass algorithmic coding.

In late 2022, Elon Musk bought Twitter for $44 billion. The multi-billionaire said he made the purchase to “help humanity”. One of the major undertakings he and his team assumed was to rid the platform of as many bot/spam accounts as possible. They successfully removed roughly 11% of these accounts, aiming to create a more trustworthy and open space for users to communicate and share content reliably.

Those on both sides of the aisle accuse each other – and their supporters – of distorting political hot topics by flooding social media feeds with negative content about candidates. This strategy aims to shape public perception through sheer volume and repetition. These accounts can be programmed to mimic human behavior, engaging with real users and amplifying disinformation. While the freedoms of such a vast platform are available for all, the customizable aspects of the app create echo chambers, which can negate the power of open discourse.

- How do we know what truth is?

- How do we know that we don’t know XYZ?

- Does all our information come from a single, or likeminded, channel/outlet?

Understanding personal and subjective limitations when digesting information would enable social media to be a tool rather than a rage room to fulfill its usefulness.

SOCIAL MEDIA, DONE RIGHT

The impact of social media on both investing in the stock market and on U.S. elections is multifaceted. Retail trading has seen unprecedented growth, fueled by platforms that have eliminated transaction fees and social media sites/apps that stir up trading frenzies. Simultaneously, the electoral landscape is being transformed by the ability of social media to shape narratives and influence voter behavior through the deployment of bots and algorithmic manipulation. The balancing act of personal freedoms, such as free speech, in relation to ensuring the integrity of financial markets and elections, will require diligence at the individual’s level.

Ultimately, the intersection of social media with investing and politics is a testament to the evolving nature of influence in the digital age.

This content is part of our quarterly outlook and overview. For more of our view on this quarter’s economic overview, inflation, bonds, equities and allocations, read the latest issue of Macro & Market Perspectives.

The opinions expressed within this report are those of the Investment Committee as of the date published. They are subject to change without notice, and do not necessarily reflect the views of Oakworth Capital Bank, its directors, shareholders or employees.