The 3rd quarter of 2024 was a nice change of pace from the first half of the year, at least in a few respects. You may remember our previous pieces on just how narrow the market has been — or to put it differently, how few companies were contributing to the overall return of the market. This pendulum has started to swing back, and we have seen more and more companies contributing to that return. This includes value-oriented stocks, more sectors, market capitalizations and even more countries.

Our somewhat easy prediction that the lack of volatility in the markets during the first half of the year would normalize has also come true. While the primary predictor for that was election-driven uncertainty, we have seen other sources of volatility emerge, including the complex Japanese yen carry trade and the Federal Reserve’s jumbo rate cut. As a result, the Volatility Index, better called the uncertainty index, has picked back up, and that is before we even get to the election.

As always with this portion of our quarterly piece, the focus is on:

- How we are positioning our portfolios, and

- What changes we anticipate making going forward.

THE MARKET

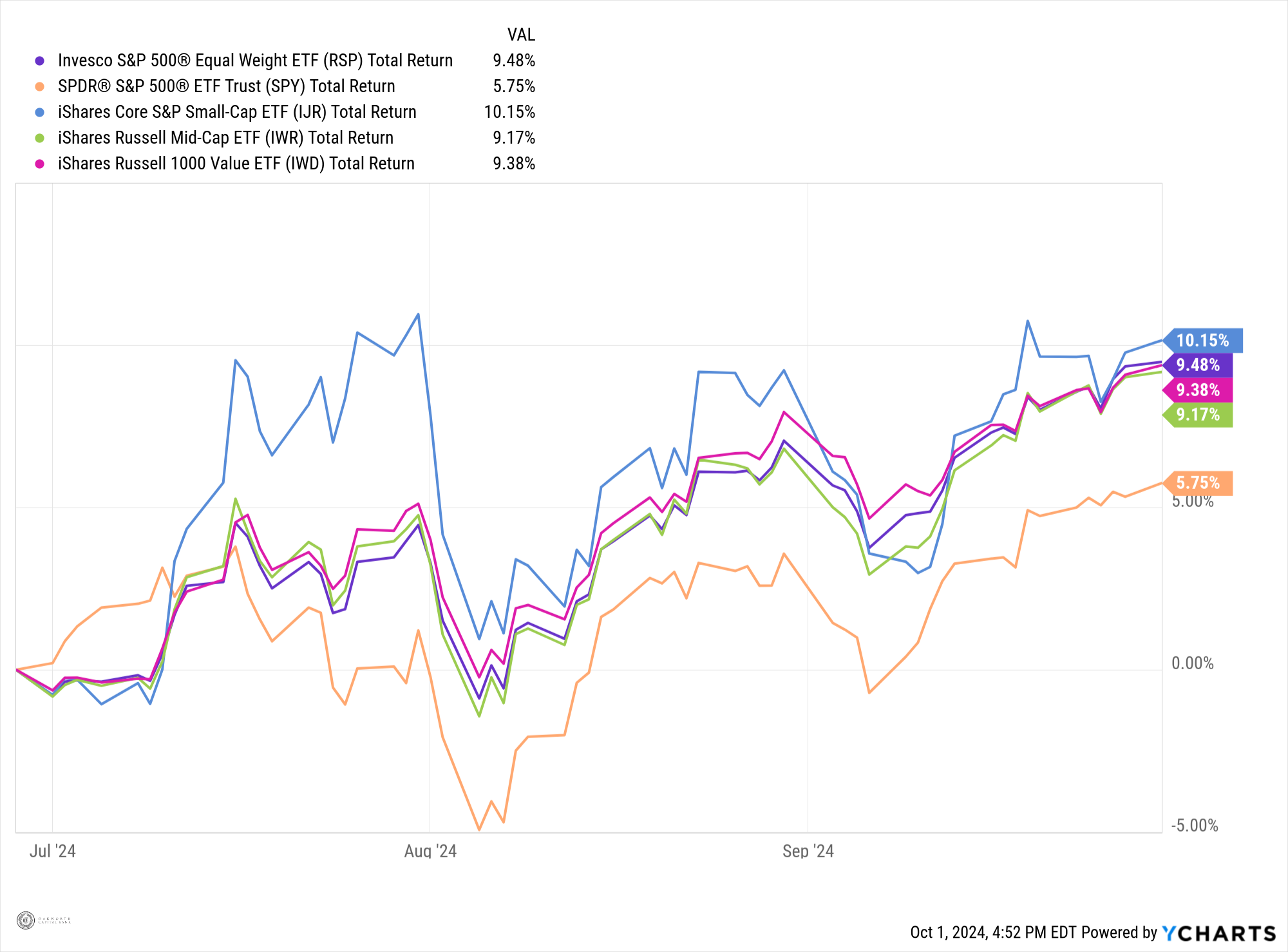

As the S&P 500 continued to be led by large-cap tech, the market’s concentration in that area continued to grow. However, as predicted, the pendulum is swinging back and is broadening in a healthy way — not by large-cap tech underperforming, but by stronger performance across the board. In fact, for 3rd quarter, the equal weighted S&P 500 outperformed the standard cap-weighted index, and that doesn’t include the small-cap stocks that outperformed both the equal weighted and cap weighted. In allocating portfolios, up through this point in the year, we’ve focused on value stocks and small- and mid-cap stocks, continuing to add to them accordingly. As this chart shows, equal-weighted, value, small-, and mid-cap stocks all outperformed the S&P 500 for the quarter.

3RD QUARTER MARKET RETURNS

The lesson learned from value stocks over the past few years? The benefits of diversification. If you were invested solely in value stocks for the first half of this year, you missed out on key outperformance in the growth side of the market. This is something that really helped push things to all-time highs and fully dig us out of the trench created by the bear market of 2022. However, it is worth noting that this outperformance from growth stocks over value stocks was for a very valid reason — earnings. The earnings growth in the market came almost entirely from the same few names driving the outperformance. Funny how that works… the areas of the market whose earnings are outperforming expectations tend to perform the best.

GROWTH VS. VALUE-FIRST HALF PERFORMANCE

As we entered the second half of the year, things started to change a bit. The fast-growing tech names have now been more accurately priced in line with their rapid growth, and, as we remember from 2nd quarter, valuation matters. To us, this didn’t necessarily signal that tech was in for a rude awakening, but rather that the remainder of the market was becoming more appealing as we began to see green shoots of earnings growth. Value stocks and smaller companies started to contribute more as well.

SMALL CAPS

Small-cap stocks have struggled for what feels like years, and the investor sentiment followed suit. In recent years, it was not uncommon to find someone asking if small-cap stocks were worth investing in anymore. This isn’t exactly rocket science, as the areas of the market that were in the forefront of the new economy happened to be the largest tech companies. Like value stocks, the smaller companies have seen an uptick in earnings. Additionally, the yield curve starting to steepen and normalize is providing a huge tailwind for the space.

Smaller companies are naturally more sensitive to changes in interest rates. Their balance sheets are typically less flush with cash than those of their large-cap counterparts. This makes these companies extremely sensitive to changes in the yield curve. An inverted yield curve is about as bad as it gets for a small company’s ability to borrow. Banks are less incentivized to lend money when the spread is tight.

What we have seen lately is the flip side of this.

The Federal Reserve has started cutting rates while the economy remains strong, resulting in a steepened yield curve. Coupled with increasing earnings in the sector, this has created a favorable environment for these companies to succeed, and we are beginning to see the effects. While smaller companies tend to be more volatile than larger companies, this two-pronged positive environment for smaller companies has drawn us to continue to increase our exposure in this space.

FIXED INCOME

Fixed income is never as exciting to talk about as equities. Frankly, if the goal of the fixed income portion of a portfolio is to be a ballast, it probably shouldn’t be. We have continued to lean on Treasuries for fixed income, as it has felt like the safest option. Any fixed income instrument outside of United States Treasuries carries additional risk, because bond issuers, unlike the United States Government, are not the controller of the currency (which also happens to be the global reserve currency). To take on this additional risk, you need a justifiable rate of additional return, and that has largely been nonexistent. Essentially, the bond market is saying things look pretty good, with strong company balance sheet, as they are not demanding a significant premium. There is an adage that the bond market is smarter than the stock market because it focuses on balance sheets, not cash flow. There is some truth to this, and these tight credit spreads we are seeing support the sentiment that the economy is still chugging along.

In summary, our allocation still prefers stocks over bonds and cash, and we anticipate a continued broadening out of the stocks contributing to the portfolio’s returns. This has been the case for 3rd quarter, and this trend should continue.

As always, we will continue to stay focused on the ever-changing landscape in front of us and remain committed to our goal of generating the best possible risk-adjusted returns for our clients.

This content is part of our quarterly outlook and overview. For more of our view on this quarter’s economic overview, inflation, bonds, equities and allocations, read the latest issue of Macro & Market Perspectives.

The opinions expressed within this report are those of the Investment Committee as of the date published. They are subject to change without notice, and do not necessarily reflect the views of Oakworth Capital Bank, its directors, shareholders or employees.