FIRST: REVIEWING THE PATH TO 2025

At the start of 2025, investors just wanted to know what the U.S. economy and stock markets could do for an encore after 2024’s surprising strength. By the end of the 1st quarter, all they wanted was either a Xanax or a stiff drink.

Let’s just say the first 3 months of the year were perplexing.

- At the end of March, investors still didn’t have a good handle on the true strength of the labor markets. After all, the official data from the Bureau of Labor Statistics (BLS) has been a little peculiar over the past 18-24 months.

- Also, despite the Federal Reserve’s best efforts, sluggish money supply growth and tepid loan demand, the official inflation gauges have remained stubbornly high.

- Throw in the new administration’s nearly frenetic behavior, and few could tell you exactly what was happening with any confidence.

What impact would Washington’s repeated tariff threats on the United States’ leading trade partners mean for the average U.S. consumer? What would they mean for domestic manufacturers, given the globalized nature of the economy? How would they impact inflation and corporate profitability? Did President Trump mean for them to be permanent? Or were they meant to be temporarily in order to influence a certain type of behavior?

TRIMMING THE BUDGET

On top of this, the Department of Government Efficiency (DOGE) hit the ground running in a big way. Headed by Elon Musk, DOGE was able to uncover a large number of instances of government waste and questionable spending. At first, the headlines from the group were arguably invigorating. Unfortunately, by the end of the quarter, the ease with which DOGE could expose Washington’s inefficiencies was almost numbing.

Just how bloated had the Federal government become? Even more, how many redundant or nonessential jobs would DOGE eliminate, or propose to eliminate? How many contracts would it terminate? Subscriptions? Travel plans? Commercial leases? Vehicle leases? Cell phones? Duplicating systems?

Trimming the Federal budget is necessary to ensure the government will be able to function effectively in the future.

After all, a redundant job is still a job. That person has a paycheck with which they purchase goods and services. A questionable contract provides revenue for the company on the other side. The list goes on and on.

All of that money, whether the government is spending it wisely or not, is still ending up in the economy in some form or fashion. Obviously, this is beneficial in the short-term, even if it is long-term foolish.

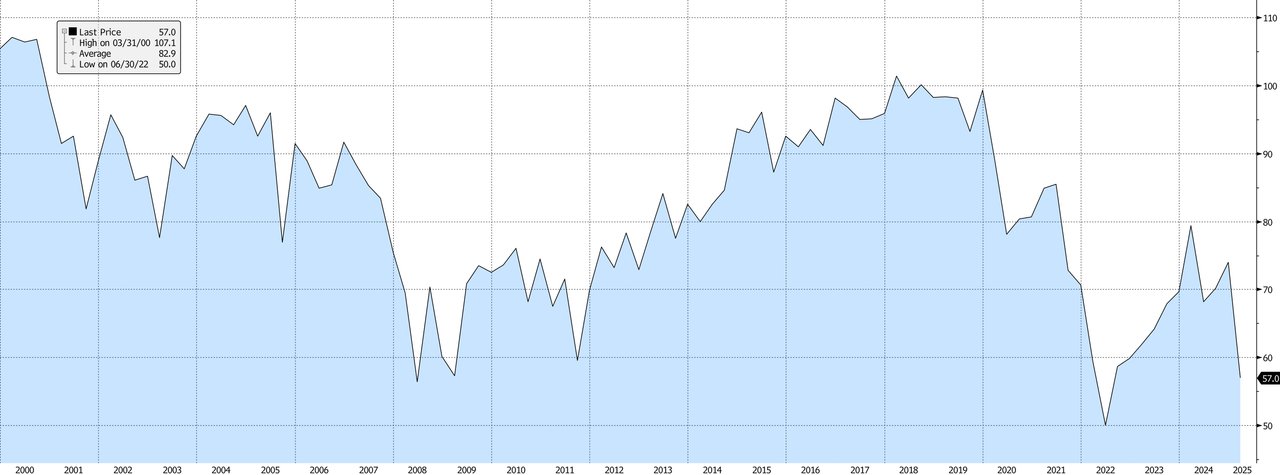

CONSUMER SENTIMENT

Not surprisingly, with everything happening in the world —and at such a rapid pace — the U.S. consumer grew increasingly concerned as the quarter progressed. Intuitively, that doesn’t always bode well for economic growth.

CONSUMER CONFIDENCE COULD USE A BOOST

Unfortunately, investors can’t control what the president or DOGE is going to do next.

- They don’t know which country will be the next to draw the short straw when it comes to tariffs.

- They have no idea just how much money Elon Musk is going to save.

- No one knows the next steps when it comes to Greenland, the Panama Canal, ending the war in Ukraine or whether Vice President Vance will even be allowed in Germany again after his speech in Munich.

What they can do, however, is analyze the economic data that Washington continues to provide in order to determine what they should do next in their portfolios. As is almost always the case, they want to know what is going to happen to consumer prices and the consumer itself. If they can figure that out, they can better predict the Federal Reserve’s next move.

Basically, everyone is trying to pinpoint when the next rate cut will be. More than that, they want to know just how many cuts the Fed has remaining in this easing cycle and when it will be finished. IF they can ascertain these things, they can either make a lot of money OR save it.

So, what is going to happen with both inflation and the U.S. consumer?

As everyone reading this magazine undoubtedly knows, consumer spending makes up over two-thirds of the Gross Domestic Product (GDP) equation for the United States. Therefore, how goes the U.S. consumer is how goes the U.S. economy. Since a paycheck is the single biggest source of income for most American households, it is fair to say how goes the U.S. job market is how goes the U.S. consumer.

LABOR MARKET

As such, you can’t talk about the U.S. economy without talking about the U.S. labor markets. If this seems a little circular, it is. This is the reason it ordinarily takes some form of shock or exogenous event for the economy to go into a deep recession.

After all, as long as the economy is creating jobs, it is creating paychecks. As long as it is creating paychecks, it is creating consumers. As long as it is creating consumers, it facilitates additional spending. As long as this happens, the economy continues to grow. Essentially, in this scenario, growth begets growth, to a point.

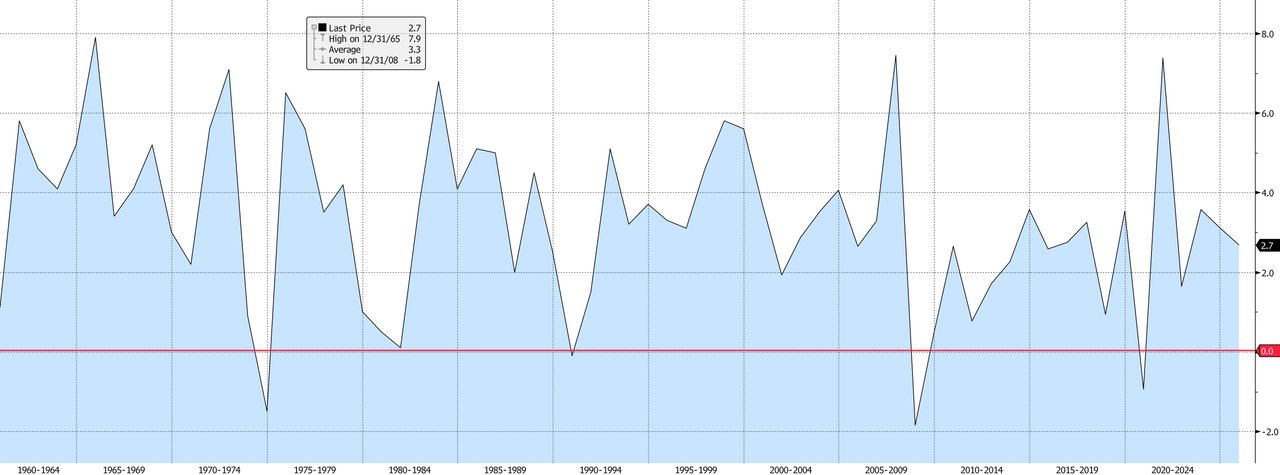

This is the reason “U.S. personal consumption expenditures chained dollars year-over-year” have only been negative 4 years since 1960 (note: chained dollars = inflation-adjusted dollars). The most recent two were in 2008 and 2020. In short, the only things that have been severe enough to derail the U.S. consumer since 1990 were a financial system collapse in 2008 and a global pandemic in 2020.

THE U.S. CONSUMER CONTINUES TO SPEND

Even so, official job growth since the pandemic’s lowest point has been pretty strong, almost surprisingly strong. Just how long can U.S. employers keep adding to their payrolls at the same pace or to the same extent? Even more so since borrowing costs, and therefore debt service, are as high now as they were at the end of 2007.

Great question— and one that would suggest a likely slowdown in hiring in the months ahead. This doesn’t mean businesses will start cutting jobs. It simply means they likely won’t be creating as many of them as they have been. That is simply what happens when “tighter money” starts to impact the income statement.

Since December 1959, the median monthly payroll growth in the United States has been 176K. As such, monthly job gains in excess of that number might imply faster-than-average economic activity. Obviously, the inverse is also true.

Due to where “we” are in this economic life cycle coupled with the Fed’s relatively restrictive monetary policy AND what promises to be tighter fiscal policy in Washington, it is hard to imagine the economy suddenly accelerating at this juncture. Therefore, job growth moving forward in 2025 should average less than 176K per month. Voila.

How much less is the $64K Question.

At the end of the 1st quarter of 2025, the good-case scenario for payroll growth over the next month would be the above stated 783-month median of 176K. The bad case scenario would be the upper bound of the 4th quartile of the observations, which is 61K. Smack dab in the middle, the 37.5 percentile, would be a change in monthly payrolls of 125K. For grins and comparisons, the monthly median has been 224.5K over the past 26 months.

More than likely, this type of cooling in the labor markets would result in a slowdown in consumer spending from 2024’s roughly 3.1% to around 1.5-2.0%, or thereabouts.

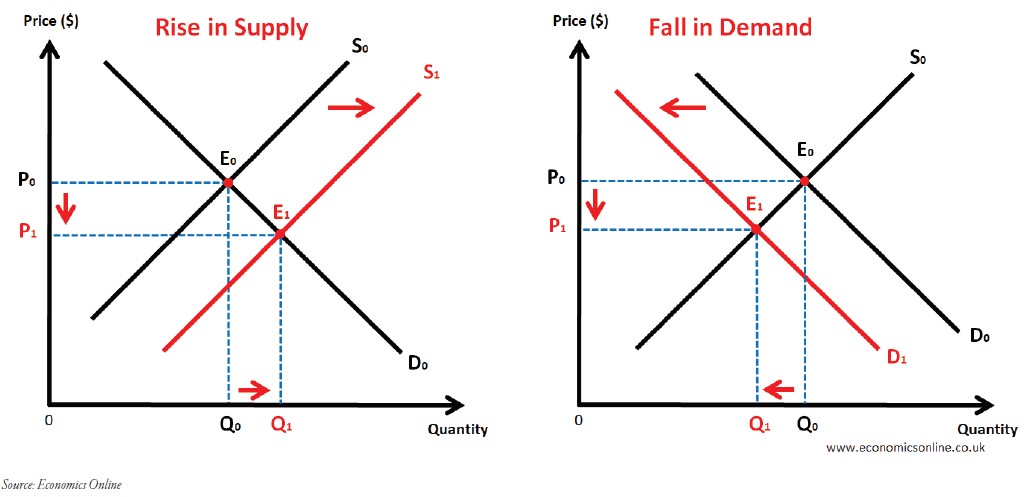

Keeping this in mind, and absent the potential impact of any tariffs or other trade restrictions, consumer prices should trend downward in this economic scenario. After all, prices are a function of supply and demand. If the economy is creating fewer jobs, it is creating fewer paychecks and, therefore, consumers. Fewer consumers, all other things being equal, means a decrease in aggregate amount. Unless supply slows in tandem with the decrease in consumer demand, prices should fall.

HOW PRICES WORK

When the supply of ingredients decreases but demand stays the same, prices go up. When supply remains constant, but demand decreases, prices fall.

That is simply the way it works. The way it has always worked, and the way it will work in the future.

THE HOUSING MARKET

Due to recent changes in immigration policy, it is highly likely that fewer people will enter the United States, in aggregate, over the next several years. Not only will this have the potential to depress prices at the grocery and the pump, but it could also serve to put a lid on rents and housing prices.

After all, according to most estimates, some 1.5-2.0 million people made their way into our country last year, and upwards of 8 million over the past 4 years. What if that annual number falls by, say, half? That’s roughly 1 million fewer folks looking for a place to put their head at night. That isn’t insignificant.

If fewer people are looking for Class C apartments, landlords will lower their rents in order to fill up their properties. Obviously, this will mean there will be an increase in supply of Class B units, and the owners there will also look to reduce prices. This, then, would create a little bit of a snowball effect, only going uphill.

To be sure, prices for homes in the more upscale sections of town might not ever get the message. However, as immigration slows due to recent changes in policy, there is no way there won’t be downward pressure on general housing prices. There will simply be fewer heads needing fewer beds.

When you consider the likely prospects for the consumer, inflation and the economy, the Federal Reserve will likely be in a position to be more aggressive in cutting the overnight rate by the end of 2025. Currently, the Fed is predicting it will make a total of 50 basis points (0.50%) in cuts by the end of December. In all probability, it will do more than that during this calendar year.

In summation, the U.S. economy is positioned for sluggish growth through the end of the 2nd quarter of 2025. However, this does not mean there will be a sharp contraction. Absent an unforeseen shock to the system, there likely will not be.

Fortunately, we should end the year on a relative high note in terms of activity and enter 2026 with greater tailwinds than are currently present.

This content is part of our quarterly outlook and overview. For more of our view on this quarter’s economic overview, inflation, bonds, equities and allocations, read the latest issue of Macro & Market Perspectives.

The opinions expressed within this report are those of the Investment Committee as of the date published. They are subject to change without notice, and do not necessarily reflect the views of Oakworth Capital Bank, its directors, shareholders or associates.