The extremely strong equity returns of the past two calendar years can be attributed to two main causes.

- The persistent strength of the labor market allowed the consumer to continue to spend and drive corporate earnings

- The meteoric rise in value of the largest growth companies known as the Magnificent These seven stocks, which include Apple, NVIDIA, Microsoft, Google, Amazon, Meta and Tesla, turned two very good years (2023 and 2024) into great years for equity investors.

The continued strength of these market catalysts was called into question by the end of 2025’s 1st quarter.

The first major change in the new year was the massive political shift in Washington on January 20, with the transfer of power to the Trump administration. Initially, the stock market was able to absorb the massive amounts of uncertainty, thanks to strong consumer spending and relentless gains from the Magnificent 7 stocks. As those two catalysts wore down, the concerns over tariffs, rising inflation numbers and a weary consumer were simply too much for investors.

On Monday, January 27, reports emerged that a Chinese company, DeepSeek, was able to develop an open-source reasoning model that outperformed OpenAI in several tests. It was reported that this AI model was developed in just a few months at the cost of around $6 million. Most believe that these claims were exaggerated, but it did add some uncertainty in the minds of investors. That day, NVIDIA lost around $600 billion in market value. To give you some perspective, the market cap of the big three auto makers (Ford, General Motors and Stellantis) has a combined market value of $120 billion.

Despite the DeepSeek headlines from January 27, a broad stock market rally continued with the S&P hitting a new all-time high on February 19. The tone shifted abruptly the morning of February 20, as Walmart reported its 4th quarter earnings. The popular company lowered its guidance for 2025 earnings and painted a much darker picture of the American consumer than expected, shaking investor confidence.

Walmart’s earnings questioned the strength of the consumer, while renewed tariff talks brought higher inflation fears back into the discussion. This raised fears that the Federal Reserve might not have the ability to reduce interest rates much further. Investors wanted to de-risk their portfolios, and the easiest and most effective way to do this was to trim back the biggest winners of the past two years. Yes, the Magnificent 7.

- During 2023 and 2024, the Magnificent 7 gained a staggering $12.05 trillion in market

- From January 27 to the end of the quarter, those same seven stocks lost $3.62 trillion in market

Some 30% of the historic gains from the last two years for these seven stocks evaporated in just nine weeks. Most of the decline in the S&P 500 as a whole this past quarter can be accounted for right here.

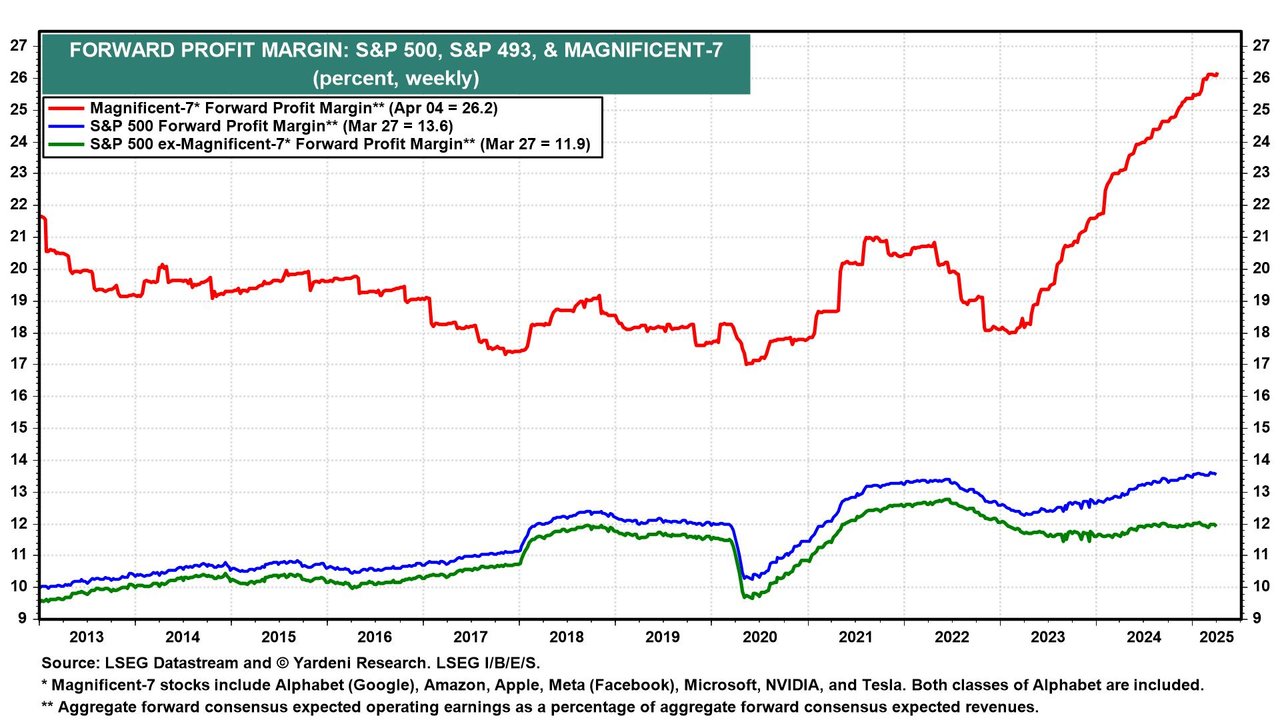

Make no mistake, the strong earnings of the Magnificent 7 have been a major contributor to corporate earnings growth in the S&P 500 these past few years. The growth in profit margins for this group of stocks has been historic. Many investors believe we have seen a peak in their ability to keep margins at such elevated levels.

HISTORIC HIGHS: MAGNIFICENT 7 PROFIT MARGINS

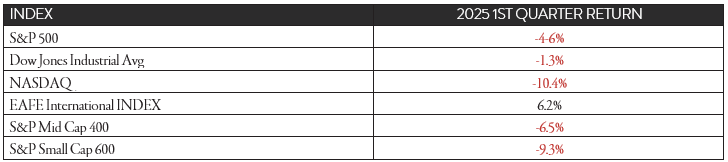

The 1st quarter ended with negative returns across all domestic equity indices. The only positive return was provided by the main international index, the EAFE(Europe, Asia Far East) Index, with a 6.2% return. Evenwith lower valuations, the small- and mid-cap stocks struggled as recession risks grew throughout the1st quarter.

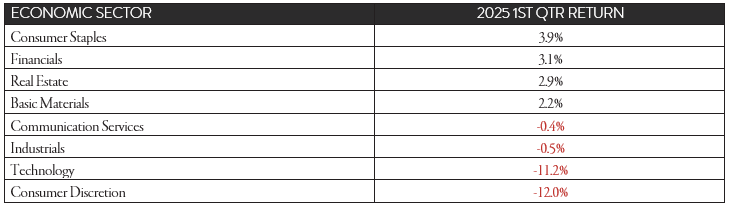

SECTOR PERFORMANCE

Looking at the performance of the 11 economic sectors showed the negative impact of the largest growth stocks had on the overall performance.

Seven of the 11 economic sectors showed a positive performance for the quarter, and two showed just a small loss. The large declines in both the technology and consumer discretion sectors were simply too much for the S&P 500 to overcome. Five of the Magnificent 7 are housed in those two sectors.

The communication services sector provides a great example of what happened in the quarter.

Several of the largest stocks from this sector had very strong returns, including AT&T (+27% in the 1st quarter), T-Mobile (+22%) and Verizon (+16%). The problem? Google and Meta carry so much weight in the sector that Google’s negative performance overshadowed strong gains from other stocks.

LOOKING FORWARD

The stock market faces an unusual number of “unknowns” as we move into the 2nd quarter. Some of these questions include:

- Will the falling consumer confidence numbers lead employers to start trimming their workforce for the first time since the beginning of the COVID pandemic in 2020?

- What will happen with the pending tariff announcements from the White House in the first week of the new quarter?

- How will those tariffs affect the stubborn inflation numbers, and will the Federal Reserve have the ability/willingness to cut the Fed Funds two or three times this year, as the stock market currently has priced in?

- Will uncertainty about the remainder of the year force companies to bring down their earnings guidance as we kick off earnings season in mid-April? If so, how far down will they come?

- Will the Magnificent 7 be able to keep profitability at current lofty levels, or will some slowing of cap spending dampen profit margins moving forward?

The amount of volatility we have seen in daily trading the last few months is directly related to some of these unknowns. The silver lining? The stock market tends to rise as clarity emerges on the health of the consumer, the economy, and the Fed’s monetary policy response to the first two questions.

It maybe too much to ask to have all these issues resolved by the end of this quarter, but I do believe it is fair to hope for a clearer picture in the second half of 2025 than the economic and political fog that we are navigating now.

This content is part of our quarterly outlook and overview. For deeper insights into this quarter’s economic trends, including inflation, bonds, equities and allocations, read the latest issue of Macro & Market Perspectives.

The opinions expressed within this report are those of the Investment Committee as of the date published. They are subject to change without notice, and do not necessarily reflect the views of Oakworth Capital Bank, its directors, shareholders or associates.