The 1st quarter of 2025 has been volatile to say the least. The mood and outlook are changing quite literally by the day, reflecting a mixture of global economic uncertainty, geopolitical risks, and changing central bank policies. After a turbulent start to the decade — marked by inflationary pressures, supply chain disruptions, and shifting consumer behavior—the unpredictability has only intensified after a brief reprieve in 2024.

Considering all of this, U.S. markets are seemingly reevaluating what they are willing to pay for future earnings and cash flows. Not only are tariffs and geopolitics a daily concern, but the cracks we have seen in the strong consumer and economy have led us to do the same.

Markets began the year with cautious optimism toward an administration that historically has positioned themselves as “pro-business,” but ongoing geopolitical tensions and softer economic data have caused investors to approach the markets with caution. Stock prices have been volatile, particularly in growth sectors that now appear to be underperforming as investors question how much they are willing to pay for uncertain future earnings.

TECH STOCKS

U.S. tech stocks (a.k.a. Magnificent 7) have experienced the unfortunate realities of a pendulum As we have previously written about, the largest companies in the U.S. market — which undoubtedly led the way up— have also been what has led the way down so far this year. In fact, plenty of areas in the market are still up for the year, although it may not feel that way given the real estate that these mega-cap names hold in people’s minds.

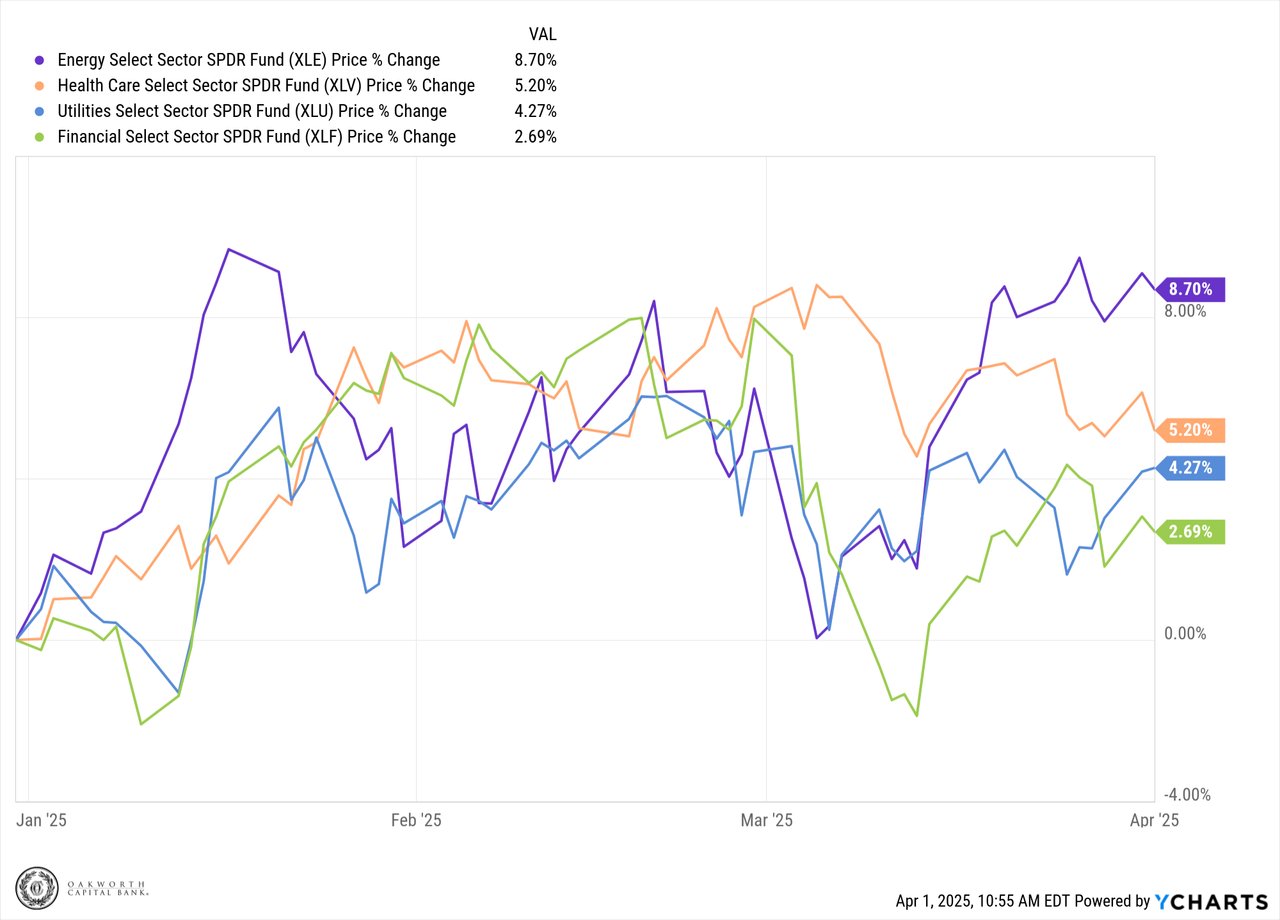

Like the pendulum that swung up in 2024, where if you didn’t own mega-cap tech you might not have done that well, that pendulum has swung the other way this time. In fact, many sectors, such as energy, healthcare, utilities and financials, are up on the year, some quite handsomely.

SNAPSHOT OF 2025 SECTOR PERFORMANCE

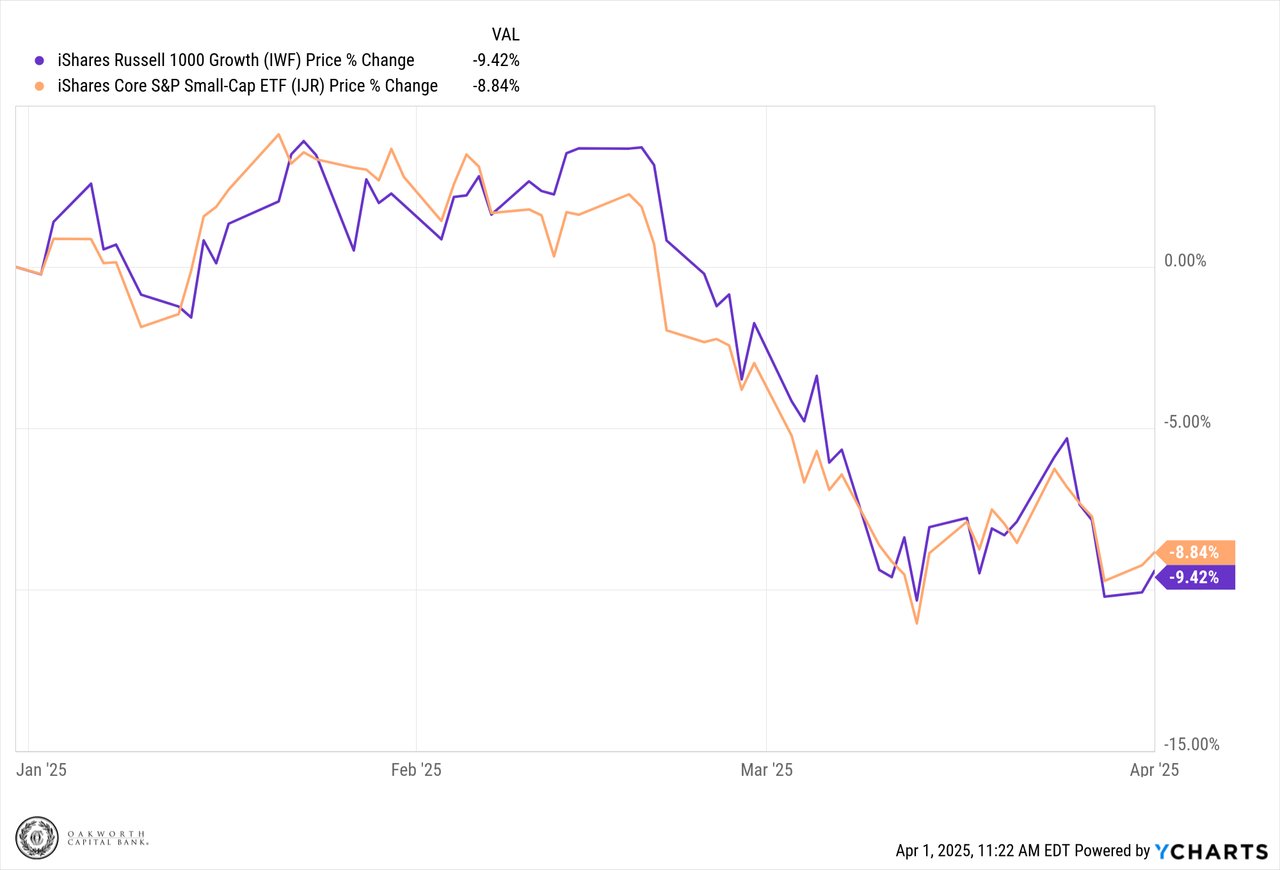

So far this year, we have continued to move the portfolio to a more conservative position with less exposure to large-cap tech and small cap. Both areas are known for higher beta, or more volatility, and our goal has remained consistent – to decrease the overall volatility in the portfolio in anticipation of last year’s market doldrums dissipating and a return to more typical market swings. To date, these have been the right calls as both areas are what have led the way down.

GROWTH AND SMALL-CAP STOCKS ARE FEELING THE PRESSURE YTD

INTERNATIONAL STOCKS

International stocks have been one of the bigger surprises to start 2025. While we believe that the United States economy remains positioned better than G7 counterparts and emerging markets, international markets have responded in lock step to the weaker dollar, which boosts their earnings and subsequently their stocks. Whether this trend continues will likely depend on the relative actions of central banks, as well as United States political policies which have led to more uncertainty being priced in.

BONDS

Volatility, however, has not been exclusive to the equity markets. Wild swings in bond prices, while less exciting to the mainstream media, have been a massive contributor to the uneasiness that has been felt so far, and the reasons have been obvious. Trade wars and inflation have had an impact, but when you add uncertainty around the Federal Reserve, over $2 trillion in new debt each year, and a murkier economic forecast — that’s a recipe for wild swings.

What sets treasury yields apart from equities is the flow through they have on the real economy. Almost every financial instrument is tied back to treasuries, either directly or indirectly.

- Rate cuts from the Fed impact everything from bank deposit rates to home equity lines of credit and credit card

- The 10-year treasury rate impacts where mortgage rates will be and what valuation people are willing to pay for future equity

The year 2022 was a good reminder of what the risks can be, even for treasuries, as long duration treasuries were down over 30% that year! We view fixed income as a place to hit singles, not swing for the fences, and our positioning philosophy. Given the continued risks and uncertainty in the bond markets, we maintain a short-duration fixed-income portfolio with a high credit quality consisting of treasuries as well as short-term corporate bonds.

While credit spreads have by no means “exploded” (the amount of higher return investors require for riskier bonds), the risk remains to the upside there, so by no means do we want to stick our necks out. Again, with fixed-income we prefer repeatable singles.

While we have reduced the volatility in our portfolios, this should not be interpreted as a sign of doom and gloom. There is nothing in the tea leaves to suggest we are on the edge of a severe recession. However, as discussed in other parts of this magazine there is undoubtedly some sluggishness.

The lack of volatility in 2024 was great and we enjoyed it while it lasted, but this was never going to last forever. Scott Bessent, the new treasury secretary, even stated that what is abnormal is for markets to only go up. Without risk (also known as volatility), there are no excess returns.

A word that has stuck with us for 2025? Flexibility. We are not trying to fully get out of equities, or positioning for a significant contraction — history has told us that markets tend to go up. Instead, we are trying to create flexibility and optionality before we need it, similarly to how one thinks about insurance.

As always, we will continue to focus on what the future holds and how that forecast impacts our clients’ portfolios. While there are a lot of unknowns this year, there is still plenty to be optimistic about and our team will be laser-focused on capturing opportunities as they present themselves.

This content is part of our quarterly outlook and overview. For more of our view on this quarter’s economic overview, inflation, bonds, equities and allocations, read the latest issue of Macro & Market Perspectives.

The opinions expressed within this report are those of the Investment Committee as of the date published. They are subject to change without notice, and do not necessarily reflect the views of Oakworth Capital Bank, its directors, shareholders or associates.