Next to the word “boredom” in the dictionary should be the following two things:

- The 1st quarter of 2024 Gross Domestic Product (GDP) report

- Recent GDP estimates for the 2nd quarter of 2024

Neither good nor bad, but slightly more bad than good. That is unless you think better than 1% but less than 2% to be good for GDP growth rate.

It has been the economic equivalent of having McDonald’s for your birthday dinner. Hey, there is nothing wrong with the #1 Value Meal when you are on the interstate, but for your birthday? Of course, I am assuming no one under the age of 8 is reading this.

What’s more, until the Fed starts cutting the overnight lending target, this sort of tepid growth is probably the best we can expect. In fact, it is sort of surprising the economy is as strong as it is, at least officially. At some point, you would have to think the U.S. consumer would collapse from the exhaustion brought on by persistent inflation and sobering financing costs.

While that could indeed happen, it isn’t likely as long as the economy continues to create jobs. Unfortunately, as long as it does so, the Fed will be forced to keep borrowing costs at a higher rate for longer. You can almost think of it as the U.S. economy being in a collar or sleeve. However, if pressed, I would have to argue the threats to our well-being are to the downside.

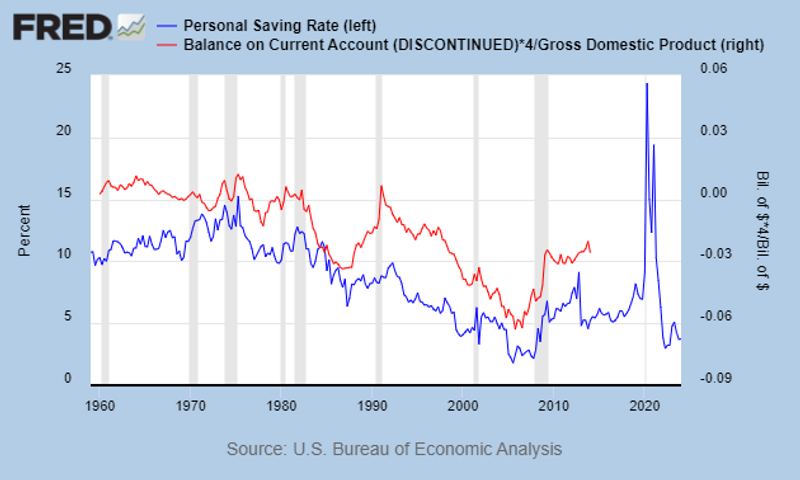

Since the end of 2021, the “U.S. Personal Savings Race as a Percent of Disposable Personal Income” has essentially vanished. Over the past 50 years, this number has averaged 7.5%. The most recent observation for May 2024 was 3.9%. Given the gargantuan size of the United States, that difference works out to be $753.3 billion in “dry powder” the consumer no longer has.

To put that number in perspective, it would be the 10th largest state economy in our country and slightly greater than the entire economic output of Sweden. Trust me, that is a lot of krona.

THE U.S. CONSUMER IS RUNNING OUT OF DRY POWDER

This decrease in savings rate would suggest the average U.S. worker is increasingly working from paycheck to paycheck. This isn’t surprising, due to significantly higher financing costs over the last several years. Anyone who has been paying the monthly minimum on their revolving debt credit card certainly knows a little something about this.

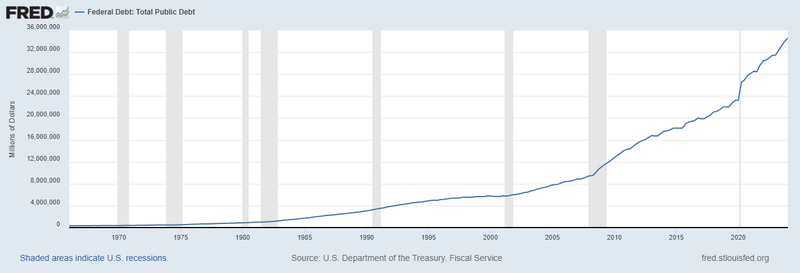

Further, the sheer mountain of debt Washington has accumulated since the end of 2019 will eventually have a negative impact on output. The reason is simple. The Treasury’s debt service will continue to increase. This will crowd out potential expenditures on other, arguably more economically advantageous, items.

Managing The Debt

As a result, Capitol Hill is going to have to get a handle on its spending, or dramatically increase economic growth in order to shrink our annual deficits. This will require either slashing entitlement programs or the Department of Defense OR completely unshackling the U.S. economy to grow as rapidly as possible.

By unshackling, I mean:

- Slash corporate and marginal personal income tax rates.

- Abolish capital gains taxes to ensure money moves around the financial system more freely and to its best use.

- Shred expensive regulations and shrink the size of the bureaucratic state.

I am talking about getting serious about this stuff and putting the hammer down. Unbridled capitalism, free markets and explosive innovation.

Now, what do you think the likelihood of either of those last two is? Slash government spending? Oh, do go on. Slashing government power? That is a sharp sauce, isn’t it?

This means we have to play the hand the powers that be have dealt us. As such, we will have to worry about inflation, the unemployment rate and the Fed. Laughingly, we will have to worry about the diseases the government inflicts and the cures that only it can deliver.

I apologize for the cynicism. However, it is all sort of comical.

- The Treasury increases the size of the public debt in excess of $11 trillion over the past five years.

- The Federal Reserve keeps the overnight rate too low for too long.

- As a result, inflation, unsurprisingly, rears its ugly head.

- The cure? Have the Federal Reserve increase the overnight rate to slow the economy, slowing inflation in the process.

To put that $11 trillion number into perspective. It took the federal government over 232 years to run up the first $11 trillion. We have done it in less than five.

THE PUBLIC DEBT IS ACCELERATING AT AN ACCELERATED BASE

Labor Markets

Then, there is employment. All of this money sloshing about the system encourages U.S. employers to hire more workers. The more free money there is the more people businesses will hire.

- However, too much money leads to too many workers.

- Too many workers lead to too much inflation.

- In order to get rid of inflation, we have to raise interest rates.

- If we do that, businesses will fire people, which will slow down the economy. However, no one really wants that.

- So, Washington continues to spend money it doesn’t have to prop up jobs the country doesn’t need.

Have you ever seen a dog bite its tail and spin around in a circle? Yeah, me too. It is kind of circular, literally and figuratively, not unlike the current state of things.

This leads me to the following probable-case scenarios, which are far easier to list in bullet points than to explain in longer prose:

- U.S. GDP will continue to be tepid through the remainder of 2024.

- The official inflation gauges will continue to show improvement, even as consumers remain frustrated with higher prices.

- The official unemployment rate will edge slightly higher, with younger workers bearing much of the brunt.

- The healthcare and education economic sectors will produce the most jobs in the private sector, possibly by far.

- Government jobs will remain reasonably plentiful due to public coffers remaining healthy, with some notable exceptions like California.

- The Federal Reserve will likely cut the overnight rate at its September 2024 Federal Open Market Committee meeting.

- The banking industry, in aggregate, will be quicker to cut deposit rates than it was to increase them when the Fed was raising rates.

- Personal consumption expenditures will show signs of slowing, but not collapsing, as job growth cools As pointed out earlier in this section, most of the “dry powder” has already been spent. So, new jobs will be the primary source of growth, if not the only, for the consumer.

- The Federal Reserve will eventually completely abandon its “quantitative tightening” program, and will quit shrinking its balance This will keep longer-term interest rates from reaching a true market equilibrium, as the Fed plays backstop for the Treasury, gobbling up the continued surge in government debt.

- If the Fed doesn’t start cutting the overnight rate by the end of the year, economic growth will be increasingly hard to achieve in 2025. It doesn’t matter who is president or controls Capitol Hill.

- Remember this, the larger the government is as a percent of the GDP equation, the smaller the private sector. Which is a better generator of wealth and a more efficient allocator of precious resources?

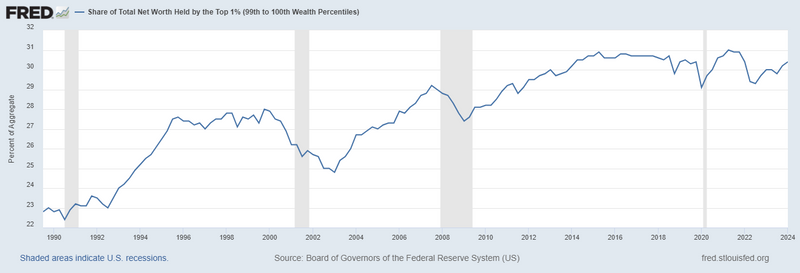

If you are struggling to answer that last question, consider this. Since the end of 2019, the U.S. economy has grown roughly $6.367 trillion through March 31, 2024. By comparison, the outstanding public debt has grown $11.385 trillion. Where did the extra $5 trillion go? The chart below, which shows the share of net worth held by the Top 0.1% illustrates it best.

THE RICH ARE GETTING RICHER

Although I am supposed to say past performance is not indicative of future results, I am also of the belief that chose who don’t learn from history are doomed to repeat. Suffice it to say, this sort of wealth creation in the hands of the very few, in such a short period of time (relatively speaking), could have a debilitating effect on future economic growth and societal cohesion.

In the meantime, what the country produces, its aggregate output, will continue to be somewhat boring for the next couple of quarters. This may not be the most effective way of increasing the overall economic pie for the masses, and will be a huge reason the data the government generates and what the average American experiences will be two different things.

This content is part of our quarterly outlook and overview. For more of our view on this quarter’s economic overview, inflation, bonds, equities and allocations, read the latest issue of Macro & Market Perspectives.

The opinions expressed within this report are those of the Investment Committee as of the date published. They are subject to change without notice, and do not necessarily reflect the views of Oakworth Capital Bank, its directors, shareholders or employees.