The stock markets kicked off 2024 on a high note, building on an incredibly strong finish at the end of 2023. That market momentum continued, and stocks realized

solid returns in the first quarter.

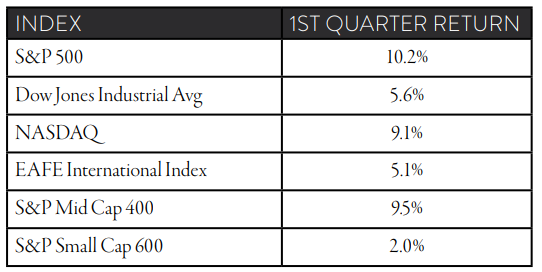

- The S&P 500, with a 10.2% return for the quarter, showed its strongest opening to a year since 2019.

- The last trading day of the quarter, the S&P 500 logged its 22nd all-time high over the last three months.

- All major indices were up in the 1st quarter.

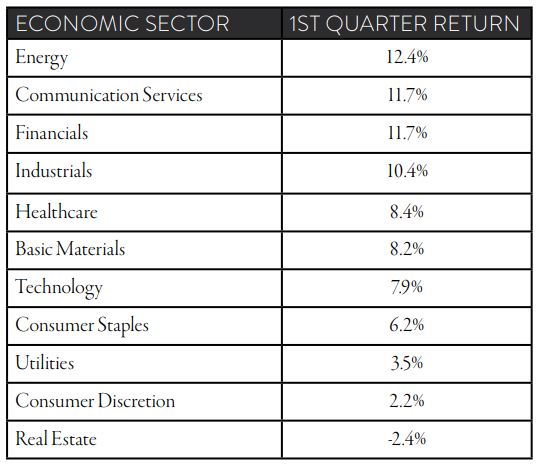

SECTORS

As we turn to economic sector returns, we have a surprising sector leading the pack: energy. Energy was the beneficiary of rising oil prices, with a barrel of oil increasing from $71 up to $83 in just three months. Communication services also stood out, led by Meta and a nice rebound in Disney shares, which surged by 35%.

The consumer sectors, both discretionary and staples, as well as utilities and real estate, were among the slowest performing over the last three months.

THE MAGNIFICENT SEVEN

In recent quarters, we discussed the stellar performance of the Magnificent 7 stocks, and the narrow market leadership through most of 2023. The first quarter of 2024, however, saw the breakup of the Magnificent 7. Two of the seven stocks continued at a remarkable pace, with NVIDIA (+82.3% for the quarter) and Meta (+35.6%)

showing significant gains above the overall market. Amazon (+17.5%), Microsoft (+12%) and Alphabet (+8%) had solid performances in the quarter as well. The two laggards were Apple (-11.3%) and Tesla (-30.6%).

Both Apple and Tesla were hit with concerns over slowing growth, a situation that is never good for stocks with valuations significantly above the market average. Their underperformance capped the returns on both the technology sector (where Apple is a major player) and the consumer discretionary sector (significantly influenced by Tesla) in the last quarter.

NVIDIA

The standout individual stock of the first quarter was, again, NVIDIA. After a great 2023, NVIDIA gained roughly 1 trillion sixty-nine billion dollars ($1,069,000,000,000) in valuation in the first quarter of 2024 alone. To put this performance in perspective, the market capitalization of Chevron, IBM, American Express, Pfizer, General Electric and Citigroup has a combined value of $1.056 trillion as we ended the 1st quarter. The market capitalization of NVIDIA increased over the last 12 weeks by more than the total market value of those six companies combined.

NVIDIA’s valuation gain in Q1 2024 > combined market capitalization of: Chevron + IBN + American Express + Pfizer + General Electric + CitiGroup

Consider this: Apple was the first U.S. company to have a market cap of over $1 trillion, and that was in 2018. NVIDIA gained more than $1 trillion of valuation in three months. Simply amazing! At some point, the law of large numbers will make it very difficult for a company this size to continue to grow at its current pace.

LOOKING AHEAD

The stock market is considered a leading economic indicator – meaning the market will start to move before we see the evidence that the economy is changing. Given the sharp upward trend over the last five months, what future economic conditions is the market anticipating?

The market is interpreting signs of slowing inflation as a signal that the Federal Reserve might start lowering interest rates at some point this year. There is growing optimism in the stock market that the Federal Reserve will be able to navigate a “soft landing” for the economy. This means that the Federal Reserve will be able to bring down interest rates to a more normal, neutral, level without causing the economy to fall into a recession.

Continued strong economic data over the last 3 months has reduced the number of anticipated interest rate cuts expected by the markets this year. Initially, the stock market had priced in six to seven interest rate cuts (of 0.25% each), but as we finish the quarter that expectation has dropped to 3 rate cuts. This makes the 10.2% return for the S&P 500 in the 1st quarter even more impressive.

There is also growing optimism around the potential that artificial intelligence, or AI, will allow corporations to become more efficient. At some point, this should allow profit margins to expand, resulting in higher earnings. However, we are still early in the AI story, and it certainly does not appear that AI will significantly boost corporate earnings much higher anytime soon. As a matter of fact, not much has pushed corporate earnings higher this past year.

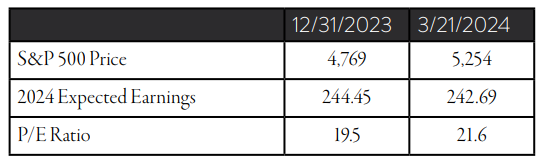

Whatever the reason, stocks continue to have momentum on their side as we move into the 2nd quarter. With earnings expectations for the year drifting down over the last three months, the rise in equity prices have made this market more expensive.

There are two ways stock prices move up: either earnings improve or the market trades with a higher P/E multiple. With P/E now at 21.6 times expected earnings, it would be difficult to call this market inexpensive. With the market already well above a more typical valuation of 18 times earnings, we could really use some significant upside surprises in corporate earnings over the next few quarters.

For 2024, the first quarter is projected to have the smallest expected growth compared to the same period from last year. It would certainly help validate the current valuation of the stock market if we can show first quarter earnings well above the current expected 3% growth over first quarter 2023 earnings.

If we do not see corporate earnings come in well above current estimates, it would not be surprising to see the stock market bounce around current levels, at least until we get election results in November.

This content is part of our quarterly outlook and overview. For more of our view on this quarter’s economic overview, inflation, bonds, equities and allocation read our most recent issue of Macro & Market Perspectives.

The opinions expressed within this report are those of the Investment Committee as of the date published. They are subject to change without notice, and do not necessarily reflect the views of Oakworth Capital Bank, its directors, shareholders or employees.