If you liked the equity markets in 2023, you probably enjoyed what the stock markets did in 2024. The average stock in the S&P 500 had a solid year, but the index as a whole delivered an exceptional performance.

- Markets enjoyed falling inflation numbers, followed by the first interest rate cuts from the Federal Reserve.

- The labor market remained stronger than most economists feared (much like 2023).

- This led to a resilient consumer in the face of higher prices over the past few years.

- That resilient consumer led to a very strong year for corporate earnings.

With only 4th quarter earnings season left, we should end 2024 with S&P 500 earnings per share around $243, or 10% higher than 2023 earnings.

THE MAGNIFICIENT 7

You can’t discuss the performance of the 2024 stock market without talking about the largest stocks in the index, also known as the Magnificent 7. The performance of these stocks (Apple, NVIDIA, Microsoft, Alphabet, Amazon, Meta and Tesla) continued to pull the return of the S&P 500 to lofty levels. The average return of these companies in 2024 was 61.7%!

When comparing the returns of the S&P 500 to the Equal Weight S&P 500 ETF, you not only see the dramatic impact the Magnificent 7 had on the returns the past two years, but also how similar the past two years have been.

The average return of the 500 stocks that comprise the S&P 500 was just under 14% in both 2023 and 2024. A two-year stretch of around 24% is impressive by any standard, placing it firmly in the range of a historically strong performance.

NVIDIA was the stand-out performer again in 2024, with a return of 176%. NVIDIA started the year with a market cap of $1.19 trillion and ended 2024 at $3.4 trillion – a 12-monthgain of $2.2 trillion. The 21 companies in the S&P 500 energy sector accounted for $1.58 trillion in market value. So, NVIDIA not only matched that but added an extra $620 billion on top. Not a bad year, to say the least.

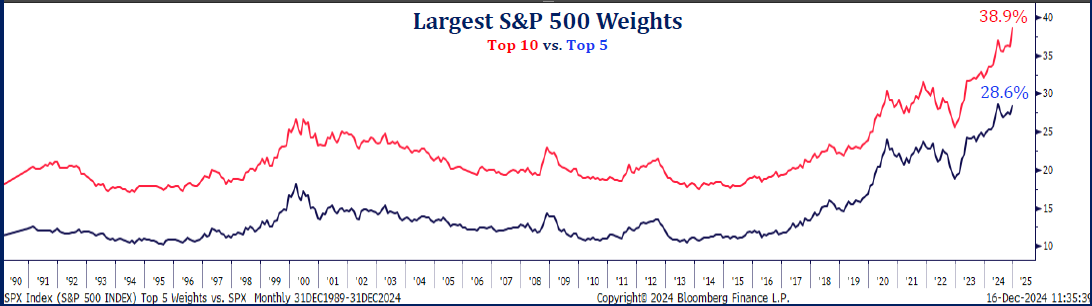

The incredible performance of the Magnificent 7 over the past two years has made the S&P 500 more “top heavy” than at any point in the past. The top 10 stocks now account for almost 40% of the entire index. Back in the dot-com bubble of 2000, the largest 10 companies comprised just under 25% of the S&P 500 index. Today, the largest five companies alone account for almost 29%.

So, what does this mean going forward for the S&P 500?

First, the performance of the largest stocks will have a super-sized impact on the performance of the S&P 500 index, for better or for worse. The past two years it has been for better. Much better!

- For reference, the largest three stocks in the S&P 500 index (Apple, NVIDIA and Microsoft) have the same impact as the bottom 350 stocks combined in the S&P 500.

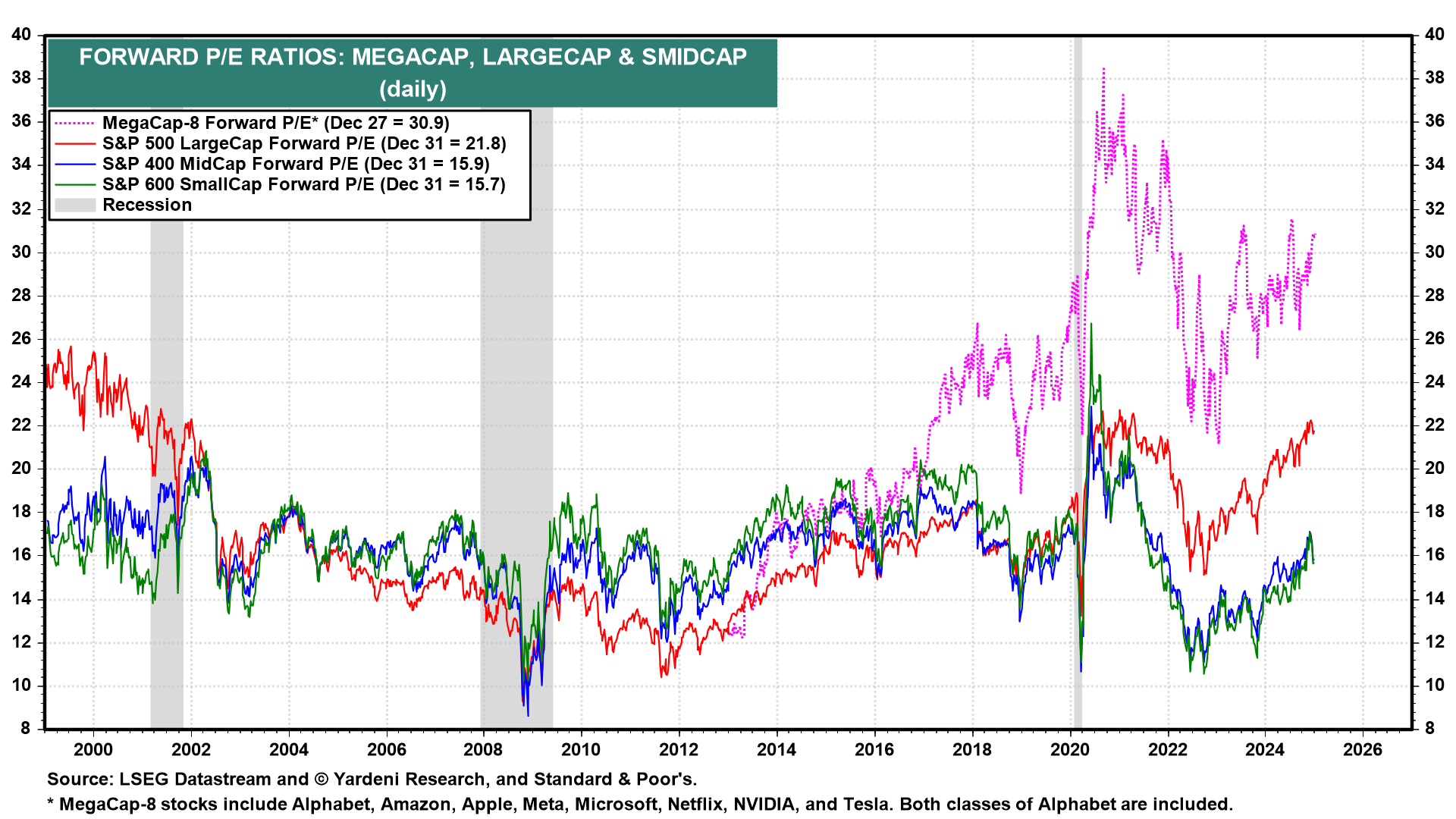

The valuation of the S&P 500 is higher than it has been in sometime, driven by growth stocks, which typically trade with higher P/E multiples than value stocks. This concentration in growth stocks has pulled the S&P’s forward P/E 500 ratio to 21.8x the next 12 months earnings.

As reference, the last two times the S&P 500 approached this valuation was early 2022 and during the dot-com bubble in 2000.

The potential for volatility within the S&P 500 is going to be higher than we have seen in some time.

P/E RATIOS ACROSS DIFFERENT MARKET CAPS

THE S&P 500

Most investment analysts talk about the stock market and the S&P 500 interchangeably. I, for one, am guilty of this.

An investor who is solely invested in the S&P 500 has never been less diversified. Large concentrations in equity portfolios can both build and destroy wealth.

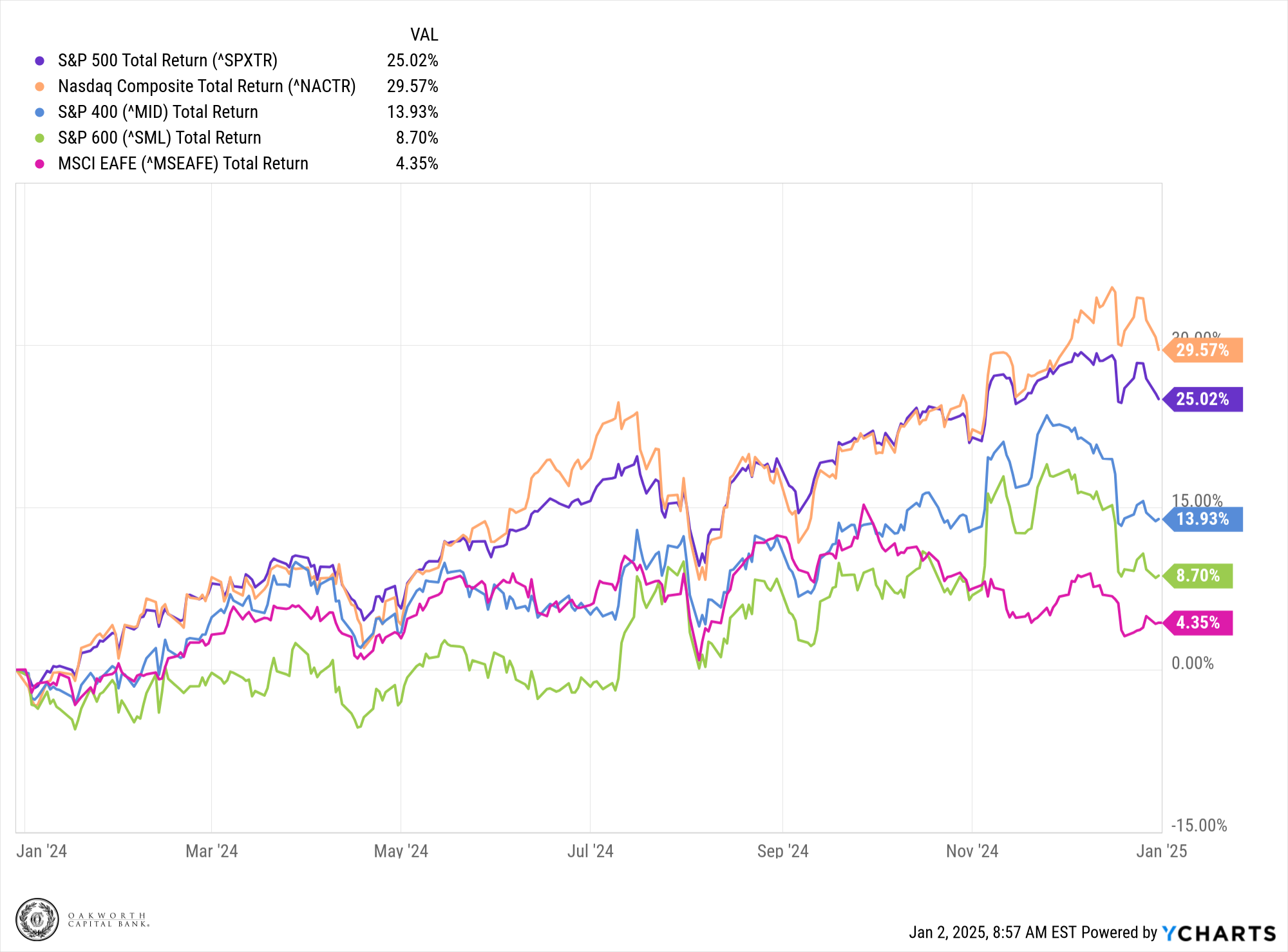

And if you thought those seven stocks held a large weight in the S&P 500, it’s even more pronounced in the NASDAQ Composite, where the Magnificent 7 makes up nearly 54% of the index. Not surprisingly, the NASDAQ index had a great 2024. The mid- and small-cap sectors performed more in line with the equal weighted S&P 500, while the EAFE international index continued to struggle when compared to any of our domestic stock indexes.

2024 TOTAL RETURNS: A LOOK ACROSS MAJOR EQUITY INDICES

SECTOR PERFORMANCE

Looking at the 11 economic sectors of the stock market, strong returns from the technology, consumer discretion and communication services sectors come as no surprise. However, the standout performance of the financial and utility stocks was a more unexpected highlight.

Financial Stocks: Financial stocks benefitted from the strong consumer, along with changes in interest rates. With short term interest rates moving down and longer rates moving higher, banks will make more profit from new loans as the cost of deposits move down and the interest rates on loans move higher.

The new Trump administration has given some indication that the regulatory environment should become a bit softer for financial institutions as compared to the outgoing Biden administration. This has been a tailwind for financial stocks.

Utility Stocks: The rise of artificial intelligence (AI) and the continued adoption of electric vehicles (EVs) are driving a surge in electricity demand. Electricity consumption will only continue to grow. Even after a difficult 4th quarter, the utility sector closed 2024 with a 20% return.

On the negative side, the healthcare, real estate, energy and materials sectors all struggled in the 4th quarter, leading to flat performance for the year.

LOOKING FORWARD

As we move into 2025, can the market sustain such strong returns as we’ve seen in the past two years? While it’s unlikely we’ll see the S&P 500 returning 24% a year, that does not mean investors can’t also have a very nice year in 2025.

As in any year, stock returns are usually driven by corporate earnings. For 2025, we are expecting the S&P 500 to produce earnings up another 10% from 2024 earnings. Earnings estimates for the year ahead are often overly optimistic, but that was not the case in 2024. If we can repeat that in 2025, we would be off to a great start. Even with no multiple expansion in 2025, this level of earnings growth should allow for a nice stock market return. And if the new Trump administration reduces tax rates on either the corporate or individual front, earnings could come in even higher, much like they did with the tax cuts of 2017.

Again, much will depend on the strength of the labor market and the resilience of the U.S. consumer. Hiring has slowed, but we have not seen any significant layoffs in the current labor market.

The market is also expecting another 50 basis points in rate cuts from the Federal Reserve. If we can see core inflation move closer to the Fed’s 2% target, the market would be very receptive to any additional help from the Federal Reserve.

The markets will also be very interested in the success of the new Department of Government Efficiency. The (growing) $36.2 trillion national debt should hamper economic growth over time, and any potential help on that front would be welcomed by equity markets.

This content is part of our quarterly outlook and overview. For deeper insights into this quarter’s economic trends, including inflation, bonds, equities and allocations, read the latest issue of Macro & Market Perspectives.

The opinions expressed within this report are those of the Investment Committee as of the date published. They are subject to change without notice, and do not necessarily reflect the views of Oakworth Capital Bank, its directors, shareholders or associates.