I am not a CPA, and won’t pretend to know all of the various ins and outs of last year’s tax reform legislation. That doesn’t mean people don’t want to know about it, which they do.

Instead of reinventing the wheel, I decided to find a short, informative article which hits a lot of the key points. After sifting through a number of them, I found the following to be just about exactly what I wanted. Even so, I will still caution you to seek out professional advice from a CPA when tax time comes!

Enjoy.

2018 Tax Changes: FAQ’s

The Tax Cuts and Jobs Act (TCJA) raises many questions for taxpayers looking to plan for the coming year. Below are answers to some of them.

Do I need to adjust my withholding allowances, given that tax brackets have changed?

You may notice a change in your net paycheck as a result of the tax law, which alters tax rates, brackets, and other items that affect how much tax is withheld from your pay. The IRS has already issued new withholding tables, and your employer should adjust its withholding without requiring any action on your part. But you may want to take the opportunity to make sure you are claiming the appropriate number of withholding allowances by filling out IRS Form W-4. This form is used to determine your withholding based on your filing status and other information. The IRS suggests that you consider completing a new Form W-4 each year and when your personal or financial situation changes.

Can I take advantage of the new deduction for pass-through business income?

The new rules for owners of pass-through entities — partnerships, limited liability companies, S corporations, and sole proprietorships — allow them to deduct 20% of their business pass-through income. The 20% deduction is available to owners of almost any type of trade or business whose taxable income does not exceed $315,000 (joint return) or $157,500 (other returns). Above those amounts, the deduction is subject to certain limitations based on business assets and wages. Different deduction restrictions apply to individuals in specified service businesses (e.g., law,

medicine, and accounting).

Can I still deduct mortgage interest and real estate taxes paid on a second home?

Yes, but the new rules limit these deductions. The deduction for total mortgage interest is limited to the amount paid on underlying debt of up to $750,000 ($375,000 for married individuals filing separately). Previously, the limit was $1 million. Note that the new restriction will not apply to taxpayers with home acquisition debt incurred on or before December 15, 2017. Additionally, the deduction for interest on home equity loans (new and existing) is suspended and will not be available for tax years 2018-2025. Note that the law also establishes a $10,000 limit on the combined total deduction for state and local income (or sales) taxes, real estate taxes, and personal property taxes. As a result, your ability to deduct real estate taxes may be limited.

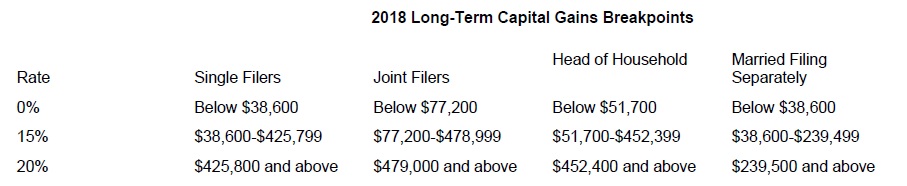

Are there any changes to capital gains rates and rules that I should know about?

The rules concerning how capital gains are determined and taxed remain essentially unchanged. But since short-term gains (for assets held one year or less) are taxed as ordinary income, they will be taxed at the new ordinary income rates and brackets. Net long-term gains will still be taxed at rates of 0%, 15%, or 20%, depending on your taxable income. And the 3.8% net investment income tax that applies to certain high earners will still apply for both types of capital gains.

Can I still deduct my student loan interest?

Yes. Although some earlier versions of the tax bill disallowed the deduction, the final law left it intact. That means that student loan borrowers will still be able to deduct up to $2,500 of the interest they paid during the year on a qualified student loan. The deduction is gradually reduced and eventually eliminated when modified adjusted gross income reaches $80,000 for those whose filing status is single or head of household, and over $165,000 for those filing a joint return.

I have a large family and formerly got to take an exemption for each member. Is there anything in the new law that compensates for the loss of these exemptions?

The new law suspends exemptions for you, your spouse, and dependents. In 2017, each full exemption translated into a $4,050 deduction from taxable income which, for large families, added up. Compensating for this loss, the new law almost doubles the standard deduction to $12,000 for single filers and $24,000 for joint filers. Additionally, the child tax credit is doubled to $2,000 per child, and the income levels at which the credit phases out are significantly increased. Depending on your situation, these new provisions could potentially offset the suspension of personal exemptions.

I have been gifting friends and relatives $14,000 per year to reduce my taxable estate. Can I still do this?

Yes, you may still make an annual gift of up to $15,000 in 2018 (increased from $14,000 in 2017) to as many people as you want without triggering gift tax reporting or using any of your federal estate and gift tax exemption. But TCJA also doubles the exemption to an estimated $11.2 million ($22.4 million for married couples) in 2018. So anyone who anticipates having a taxable estate lower than these thresholds may be able to gift above the annual $15,000 per-recipient limit and ultimately not incur any federal estate or gift tax. Note, however, that the higher exemption amount and many of TCJA’s other changes to personal taxes are scheduled to expire after 2025, unless Congress acts to extend them.