I have a crystal ball in my office. Seriously, I do. It was a gift from a client, who happens to be my old T-ball coach. Every time someone says something along the lines of “I know you don’t have a crystal ball,” I stop them and let them know I do.

Not surprisingly, I get a lot of “mileage” out of the thing in this manner. Unfortunately, it doesn’t do a very good job of actually predicting the future. When I am looking for visions of what is to come, the only thing I see in my crystal ball is my upside-down reflection.

Actually, due to the ball’s convexity, I think it might be my refraction I see. However, this isn’t a physics paper.

This is unfortunate, because the economic data is increasingly confusing, at best. At worst, it is a bit troublesome. Enough so to make me want to believe in the fabled efficacy of crystal balls, tea leaves, horoscopes and tarot cards.

I won’t mince words. In aggregate, the U.S. consumer seems exhausted and a little skittish. I suggested as much in this newsletter a couple of weeks ago. Today, I am removing any suggestion and laying it all on the line.

IF “personal consumption expenditures” are higher in the 1st quarter 2025 Gross Domestic Product (GDP) report than they were in 2024, on average, I will let our CEO, Scott Reed, hit me in the face with a pie AND the marketing department can post it on social media. This is an easy bet, because it will never happen.

Shoot, I don’t need my crystal ball for such low-hanging fruit. However, a “working” one would be useful in determining just how long consumer expenditures will be lower than their potential. Is it just the one quarter? Or is it two or three?

Personally, I suspect it will be around 2 and one-third quarters, also known as 7 months. There is no magic to that other than 2 quarters sounds a little too tidy and 3 seems a little too long, at least as I type here on February 28th. After all, the economy isn’t necessarily broken as much as it needs a bit of a breather.

The reason for this relative pessimism is because a large chunk of U.S. households is already in a recession. This is an open secret, a big one.

Consider this snippet from a somewhat scary article by Allysia Finley in The Wall Street Journal recently:

“In 2007, 35% of new FHA borrowers had debt-to-income ratios above 43%. By 2020, 54% did. As housing prices and inflation surged, borrowers became more stretched. The FHA kept insuring mortgages to borrowers who were increasingly leveraged. About 64% of FHA borrowers last year exceeded the 43% threshold.

The FHA loan portfolio is far riskier than it was before the 2008 housing crisis. The American Enterprise Institute’s Ed Pinto and Tobias Peter estimate that 79% of FHA first-time borrowers have a month or less in financial reserves—not enough to make mortgage payments if their household expenses rise, as most have owing to inflation.”

In case you were wondering, FHA loans are ideally for first-time homebuyers and/or middle- to lower-income households. The goal of the program is to increase homeownership rates amongst these demographics. What the selected paragraphs tell us is that the target market for FHA loans is increasingly no longer the target market, and not in a good way.

Think about that statement: “79% of FHA first-time borrowers have a month or less in financial reserves—not enough to make mortgage payments if their household expenses rise, as most have owing to inflation.”

That is the very definition of living paycheck to paycheck. We are talking about no savings and barely enough to cover the bills.

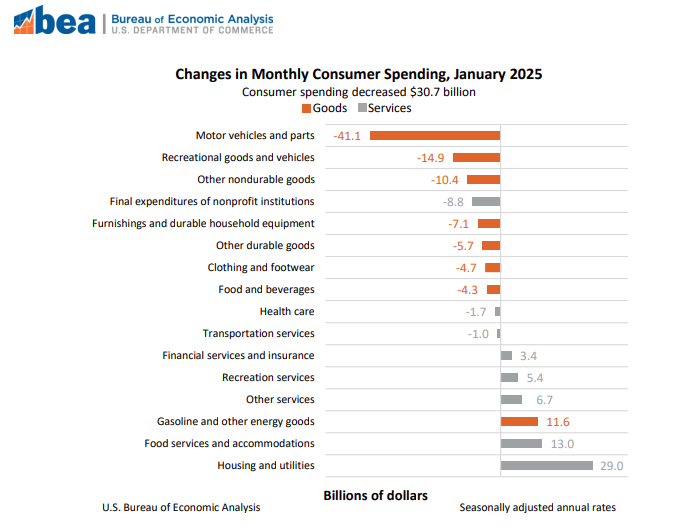

To that end, take a look at the table below to see just how the American consumer spent its money in January 2025. Remember, these numbers are all seasonally adjusted. So, you are looking at how they spent this January relative to other Januarys in the past. That might not be a perfect definition, but it is good enough for tailgate conversation.

So, what don’t you see in the table? Spending on “stuff,” perhaps? If that is the case, exactly how did the U.S. consumer spend its money in January? Again, these numbers have been “seasonally adjusted.”

Let’s see. Housing and utilities? Check. Food services? Yep, it is in there. Gasoline and other energy goods? Sure. Basically, last month, the U.S. consumer spent money to “get by.” It didn’t spend money like it needs to generate meaningful economic growth.

Of course, one month does not a trend make. However, when you couple the two stories here with the recent sizable drop in Consumer Expectations, the picture gets a little darker and the crystal ball a little foggier. If you think my phrasing is depressing, let me cut & paste the actual verbiage from The Conference Board:

“The Expectations Index—based on consumers’ short-term outlook for income, business, and labor market conditions— dropped 9.3 points to 72.9. For the first time since June 2024, the Expectations Index was below the threshold of 80 that usually signals a recession ahead.”

Okay. Don’t freak out about that word in the last sentence, recession. This drop in “expectations” isn’t a guaranty we will have one. It simply means it is characteristic of past recessions.

If that seems confusing, consider this: All Americans like apple pie. William likes apple pie. Is William an American? Perhaps.

All of this is to say, there is enough evidence out there right now to suggest the 1st quarter GDP report could be a little ugly. By ugly, I mean there could be a negative sign in front of it. Psst, unless something dramatic happens in March, it will.

However, even that doesn’t mean we will have a recession.

After all, one bad quarter does not a recession make. Sometimes even 2 bad quarters doesn’t mean we are officially in a recession, at least not immediately. After all, the BEA can always go back and “revise” the data later. This is why the powers that be don’t define a recession until it is well in the rearview mirror.

With this all said, at the end of March, we will likely be closer to a recession that we were at the start of the year. The consumer is weaker than originally believed, and a lot of folks are struggling to make ends meet. There, I have said it.

Still, overall, it isn’t a Doomsday scenario at this time.

It just makes me wish my crystal ball, from my old T-ball coach, actually worked.

Thank you for your continued support. As always, I hope this newsletter finds you and your family well. May your blessings outweigh your sorrows on this and every day. Also, please be sure to tune into our podcast, Trading Perspectives, which is available on every platform.

John Norris

Chief Economist

Please note, nothing in this newsletter should be considered or otherwise construed as an offer to buy or sell investment services or securities of any type. Any individual action you might take from reading this newsletter is at your own risk. My opinion, as well as those of our Investment Committee, is subject to change without notice. Finally, the opinions expressed herein are not necessarily those of the rest of the associates and/or shareholders of Oakworth Capital Bank or the official position of the company itself.