As we entered the second quarter, the equity markets had a few topics gathering most of our attention.

- First, will the banking issues that beleaguered us in early March be limited to a few institutions that made poor decisions with risk management, or would those issues become contagious amongst other banks?

- Second, would the weight of high inflation for the past two years finally catch up to the consumer, and see either a mild or even sever recession grip the U.S. economy? Throw in the fear that our leaders in Washington D.C. could not come to some compromise with raising the debt ceiling, and… for the first time ever, would we default on our nation debt?

As we progressed through April, May and June, it started to become clear that a deep recession was not materializing for 2023. The labor market was showing no signs of weakening, and thus consumer spending was not slowing as much as feared. Inflation continued to fall from its peak last summer. Finally, both political parties wanted to continue to spend money, and the debt ceiling was lifted. All of this allowed the stock market to add on to the gains provided in the first quarter.

The first half of 2023 in the equity markets have been characterized by strength in just a few names.

- Large cap stocks outperformed smaller stocks

- Domestic stocks outperformed the international equity index

- The S&P 500 has returned 8.3% for the second quarter and a solid 15.9% year to date, but those returns can be a bit deceiving as the average stock showed a much lower return.

In total, just seven stocks accounted for the bulk of gains.

THE MAGNIFICIENT SEVEN

These handful of outperforming stocks have been playfully dubbed the “magnificent seven.” These stocks, which include Apple, Microsoft, NVIDIA, Amazon, Alphabet, Tesla and Meta currently comprise 27.7% of the S&P 500. Their average return for the second quarter was 27.5%, with a staggering average year to date return of 89%.

You need to travel back to the height of the dot-com bubble in late 1999 / early 2000 to find such a small handful of names that have had this dramatic of an impact as the “Magnificent Seven” on the return of the S&P 500.

The good news? Valuation levels are currently much lower than we experienced at the end of the dot-com phase.

SECTORS

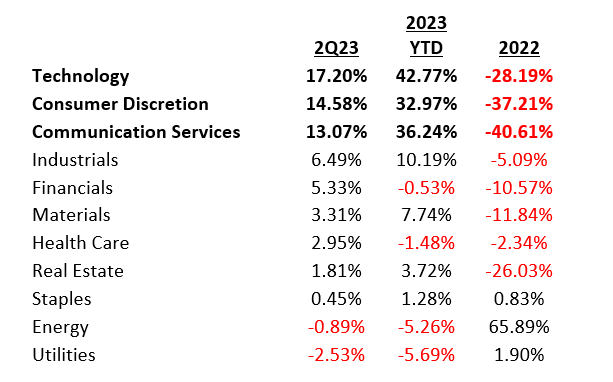

Not surprisingly, the three sectors that hold those Magnificent Seven stocks saw the best performance for the second quarter. The clear winners for the quarter were as follows:

- Technology (+17.2%)

- Communication services (+14.6%)

- Consumer discretion (+13.1%)

The financial sector, on the other hand, after an extremely challenging 1st quarter, saw a return of 5.3% in the 2nd quarter, as the banking crisis that gripped this sector late in the first quarter eased.

This continued desire for additional risk for investors in the second quarter was not good news for the three defensive sectors of the stock market. Utilities (-2.5%), consumer staples (+0.5%) and healthcare (+3.0) failed to keep pace with the broader market. The other sector that struggled was the energy sector, with a loss of 1.3%. The much slower reopening of China from their COVID shutdown has made worldwide demand for oil come in weaker than expected, keeping oil prices down.

This wide disparity of returns between economic sectors was a carbon copy of the first quarter, but a mirror image of 2022.

Interestingly, the three economic sectors that have provided massive returns so far in 2023 were the same sectors that were hammered in 2022.

LOOKING FORWARD

One important component of the market’s valuation is corporate earnings. This year, expected earnings have decreased while stock prices have increased. As we started the year, the annual expected earnings for the S&P 500 were $230, while the S&P 500 started the year trading at 3,839. In other words, we were trading at 16.7x earnings. Over the first six months of 2023, the price of the S&P 500 has climbed up to 4,450, while the 2023 earnings expectations for the index had dropped to $220. The current multiple for the S&P 500 is 20.2x earnings.

We still have three quarters of earnings results left for this year, but actual earnings need to come in quite a bit above current estimates for the rally in the stock market to continue. We won’t have to wait long as second quarter earnings season will be in full swing by the end of July.

The other component that has been driving the market has been the decline of headline inflation. This year, the market believes that the Federal Reserve is finally nearing the end of their rate hiking cycle. The belief held by the stock market just a few months ago is that we would see interest rates dropping in response to a potential recession. This is no longer the case. We are now looking for one or two more interest rate hikes, followed by a pause from the Fed.

How quickly will core inflation recede over the next six months? Each inflation reading will be closely scrutinized by both the market and the Fed. Cooling inflation numbers would allow for the Fed to finally put an end to this tightening cycle. The more important question then becomes will that cooling inflation data be coupled with a slowdown in the economy. As we start the third quarter, not many signs point to a rapidly cooling economy. Hopefully that does not mean core inflation will remain stubbornly high for the remainder of 2023.

For more from our Investment Committee in our 2nd Quarter 2023 Macro & Market Perspectives, click the image below.

The opinions expressed within this report are those of the Investment Committee as of the date published. They are subject to change without notice, and do not necessarily reflect the views of Oakworth Capital Bank, its directors, shareholders or employees.