Talking money can feel tacky, but there is a time and a place for it – especially with your professional wealth advisors and your family when the moment is right. Without open communication, years of planning and preparation can be easily undone by an unexpected moment or event.

Today, November 8th, is National Talk Money Day, an annual opportunity to break down the stigma that surrounds financial discussions, align on personal goals, and promote open communications with those you love.

Whether you are a millennial, Gen X, or Baby Boomer, you will likely be affected by the Great Wealth Transfer in one way or another. As assets transition to heirs, entities or charitable causes, this transfer becomes significantly more efficient and meaningful when all parties understand the basics. Everyone has a different opinion on discussing the estate plan, but research highly suggests that early conversations result in a stronger, more intentional legacy.

So, what is the Great Wealth Transfer?

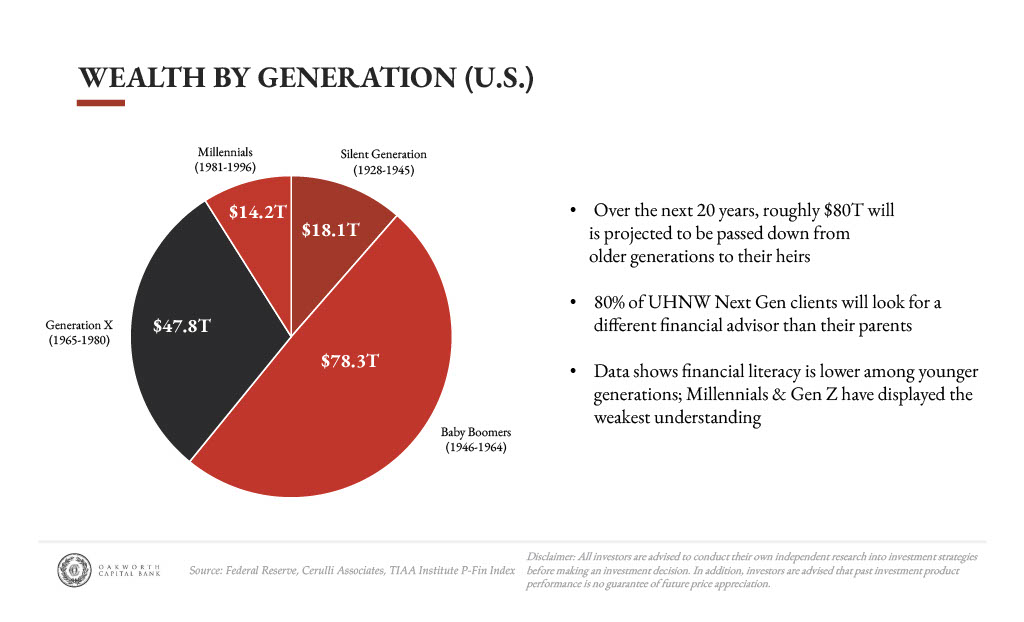

Over the next several decades, the Baby Boomers and Silent Generation are forecasted to hand off the largest transfer of wealth in history, with their Generation X, Millennial, and Generation Z children as primary beneficiaries. Over $70 trillion is set to be inherited by the next generation, with over $10 trillion destined for charities (Cerulli). The data also shows that financial literacy and confidence decreases with the younger generations. As we approach the “Sunset” of the historically high lifetime exemption, the Great Wealth Transfer presents a unique intersection of estate planning and family education. As high net worth individuals continue to minimize their taxable estates, the communication with family becomes even more important with so many assets and entities in motion. With grantor retained trusts, lifetime access trusts, and charitable bequests being primary gift options within the lifetime exemption limits, it is common that the balance sheet of a high-net-worth family will include a variety of trusts, entities and investment vehicles. With those different vehicles come different stipulations around the access, path, and overall inheritance. When passing on assets, explaining the “why” behind them often matters more than explaining “what” they are.

By holding a family meeting with your wealth management team, your attorney, and your CPA, the “why” can be answered most effectively. Your team is not just there to put your plan in place, but to educate your heirs by answering key questions while all parties are present and before any transfer is in motion. By using visuals such as flow charts, balance sheets, and estate summaries, your team should be well equipped to educate the entire family and ensure your legacy is communicated and upheld.

Communication within families, particularly around finances, can be challenging. Money aside, it is hard enough to get holiday plans aligned with the many branches of the family tree. In a survey conducted by asset manager Edward Jones, over 70% of respondents stated they feel comfortable discussing wealth with the next generation. However, only a quarter of those respondents have put the wheels in motion and accomplished that feat. In order to cement any assumptions into a clearcut understanding, initiating the conversation is essential. A successful family meeting starts with preparation – ensuring that all parties are present and comfortable, and that the conversation remains candid. Above all, the communication must be clear, and the question “why” must be answered.

![]()

The Family Meeting

To create a successful and productive family meeting, the family must establish an agenda that allows each participant time to share insights. The Wealth team can discuss the products in play and suitability involved, while the estate attorney can focus on the estate plan, and the CPA can review the tax information. By parceling out an agenda, it can keep the meeting concise and educational. It is also extremely important to establish ground rules and expectations prior to the meeting. For example, some families may not be as comfortable sharing exact dollar amounts or inheritance projections during this stage. The last step before kicking off the meeting is to discuss goals and expectations with the family and check in on those throughout the meeting. This is a great way to open and encourage communication, while also a great icebreaker to kick things off. The purpose of the meeting is to educate and discuss what wealth means to the family, while also establishing open communication. A successful family meeting should leave all parties with a clear understanding of the origins, direction and purpose of the family’s wealth.

It is only fitting that the man on the one-hundred-dollar bill coined the phrase “nothing is certain except death and taxes.” Coincidently, both play a major role in your wealth transfer. To keep as many Benjaman Franklins in motion to their intended destination, communication is key. Starting the discussion early not only ensure the proper time and effort to prepare for this transfer, but it also allows for all parties to be in sync. By discussing your plan with the next generation heirs, it will ensure that they are properly equipped and prepared to be educated stewards of the wealth that you have created and preserved.

One of my favorite financial proverbs says: “the first generation builds the wealth, the second generation lives off it, and the third generation loses it.” To avoid this pitfall and to preserve wealth across generations requires careful planning, effective tax minimization and responsible stewardship over time. The first step in this process is to “Talk Money” with strategy and intention.

This document is being provided for informational and educational purposes and is not meant to be taken as specific advice. Oakworth Capital Bank does not provide tax or legal advice. All decisions regarding the tax and/or legal implications of these strategies should be discussed with your tax and/or legal advisors before being implemented.

Sources: