At the end of 2023, very few had high expectations for the upcoming year. There were any number of headwinds facing the economy, and the U.S. stock markets had just had a surprisingly strong year. The U.S. was going to have a contentious election season, and the geopolitical climate was a mess.

So uncertain were the prospects for 2024, most folks would have been more than happy with middling economic activity and modest investment returns. As we all well know now, both the economy and stock market more than exceeded expectations.

- Employers kept adding jobs, creating consumers in the process.

- The federal government spent trillions of dollars it didn’t have.

- Local and state governments, awash in tax receipts thanks to inflation, went on a buying spree.

- Businesses invested massive sums in new technologies.

In fact, the best way to describe 2024 is that just about everything behaved much differently than anticipated.

There was one noticeable exception. What passes for civil discourse in our society remained decidedly uncivil.

Toward the end of what had already shaped up to be a good year, the Federal Reserve finally decided inflation was contained enough to start cutting the overnight rate. This seemed to add a fuel to the proverbial fire, as did November’s election results.

Now, whether people can tolerate Donald Trump’s personality or not, it seems business owners, consumers and investors liked the prospects for an extension of the Tax Cuts and Jobs Act of 2017, perhaps even a permanent one. Further, the presumption is that the Republican Party will be more “business-friendly” than the Democrats, what with the promise of lower corporate tax rates and less regulation.

Whether these things come to pass is still anyone’s best guess, but investors apparently remain hopeful.

Still, the question remains: what can the U.S. economy and stock market do for an encore after a surprisingly strong 2024? Will they have enough fuel to generate similar results in 2025?

The path of least resistance is to anticipate more, shall we say, subdued returns. That doesn’t mean the markets or the economy are going to fall apart. Far from it. Still, a repeat of this past year’s outsized performance isn’t statistically likely. It would be like expecting the Dodgers’ Shohei Ohtani to hit 50 home runs and steal 50 bases again this upcoming season.

Can he do it? Sure. However, considering he was the first person to ever do this in one season, and he had never previously done either until this past year, it remains far more of a possibility than a probability.

Therefore, let’s look back on this past year as one that exceeded everyone’s expectations, and be happy about it. As for moving forward, it is best to be hopeful for a decent, if unremarkable, year.

We shall see.

Thank you for your continued support.

John Norris

Chief Economist

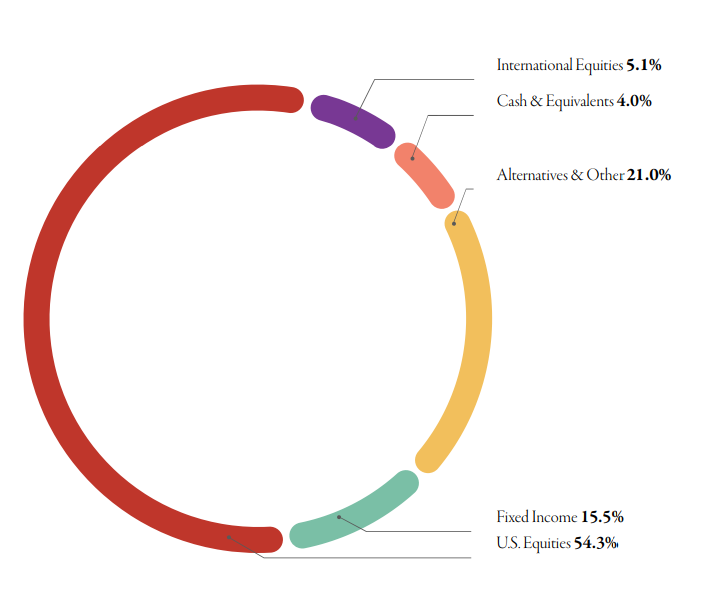

Our Investment Committee distributes information on a regular basis to better inform our clients about pending investment decisions, the current state of the economy and our forecasts for the economy and financial markets. Oakworth Capital currently advises on approximately $2.2 billion in client assets. The allocation breakdown is in the chart below.

This content is part of our quarterly outlook and overview. For more of our view on this quarter’s economic overview, inflation, bonds, equities and allocation read latest issue of Macro & Market Perspectives.

The opinions expressed within this report are those of the Investment Committee as of the date published. They are subject to change without notice, and do not necessarily reflect the views of Oakworth Capital Bank, its directors, shareholders or associates.