What are the effects of rising interest rates on equity markets? It sounds like such a simple question. When looked at in isolation, most would conclude that rising rates would hold back stock prices. Just consider a few of the effects of rising interest rates on stock valuations:

- Borrowing cost for companies will increase, and that should lower corporate earnings.

- Higher interest rates will mean that future earnings will be worth less in today’s dollars. This is the main reason that the price-to-earnings multiple for stocks will traditionally be lower as interest rates move up.

- Higher interest rates should slow loan demand, leading to a slower growing economy.

- Higher bond yields would make bonds a more compelling investment vs. stocks

- As consumer loan rates (mortgages) increase, the consumer should have less disposable income.

Just a quick glance over this list would seem to support the prevailing thought that higher interest rates, in isolation, are a drag on stock valuation. The key word in all of this is isolation. Unfortunately, interest rates rarely move in isolation. They move in reaction to events that revolve around the strength of the economy.

Before we dive any further, let’s clarify what we mean by a rising rate environment. There are two pieces of interest rates moving up. First, the Federal Reserve will adjust the Federal Funds Rate. This is the rate at which commercial banks borrow and lend their excess reserves to each other overnight. This controls short-term interest rates. Longer term interest rates are determined by supply and demand in the open market. For example, when the economy suffers a dramatic downturn, money will flow out of riskier assets (stocks) and into less risky assets (bonds). This move will push interest rates down and bond prices up.

So, what environment do we see interest rates moving up? Consider the Federal Reserve has two mandates: employment and inflation. The economy has to be strong enough for the Federal Reserve to be more concerned about inflation than job creation. That is typically going to happen when the economy is strong, and getting stronger. When investors have confidence that the economic strength will continue, and they sell some of their bond holdings to try and produce a greater return with stocks. This will also push interest rates higher.

We are finally getting to the important question. What is more important for equity returns, low interest rates or a strong and growing economy? Because almost every time, interest rates go down when the economy is weak, and interest rates go up when the economy is strong. I will take a strong economy every time! As we recover from this global pandemic, the stock market can handle rising interest rates, as long as it is accompanied with an economy that continues to get stronger. That is the “secret sauce” for strong equity returns. Most do not believe that the Federal Reserve will start to move the Fed Funds rate up until 2023. Even then, it will most likely be a slow and methodical march up in rates.

This is, simply put, the business cycle in action. Some event will cause the economy to slow or stall, the Federal Reserve steps in and lowers the Fed Funds rate to help employment, investors will try to quickly reduce their risk by selling stocks and buying bonds, pushing interest rates down. Equity prices fall to a level that investors will find some value, and the economy slowly recovers. The economy grows stronger and stronger with time, leading to more optimistic investors shedding their bond holdings, wanting to get into the strong returns provided by stocks. Some new “problem” arises, and we start all over again.

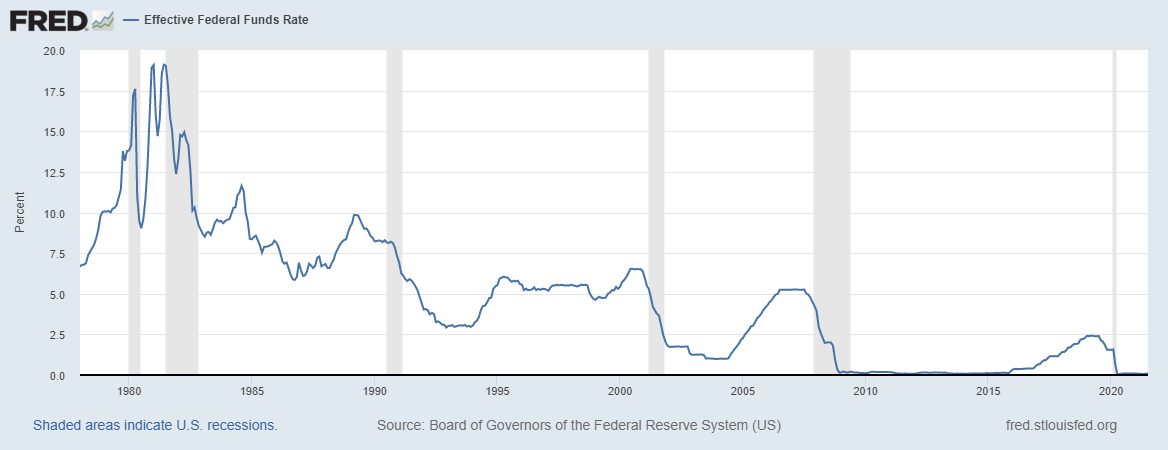

The following chart showing the Federal Funds Rate from 1978 to current day, shows the dilemma that may face the equity market over the next few decades. We can see that interest rates have been falling from their peak in 1981. As one business cycle has morphed into the next, we have seen lower highs and lower lows with interest rates.

That long-term trend down in interest rates has allowed for very strong performance for both stock and bond holders for a long time. It may not be noticeable in any one business cycle, but the tailwind of long-term falling interest rates may be a thing of the past.

After the dot-com bubble burst in 2000, the Fed Funds Rate dropped from 6.5% down to 1%. The Fed then raised rates from 2005 to 2006 up to 5.25%. The financial collapse of 2008 brought the Fed Funds rate all the way down to 0.25%, and stayed there until rates started to move up again in 2016, moving up to just over 2% by 2019. Lower highs (6.5% to 5.25% to 2%) and lower lows. Unless we start to see a negative Federal Funds Rate, we can’t get any lower.

Next week:

Over the next several business cycles, flat to upward trending interest rates will lower bond returns, and make it difficult for the equity markets to match the returns we have seen since 1981. That may make asset allocation decisions a bit more difficult going forward…