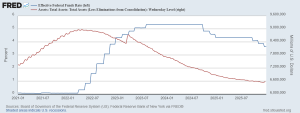

The S&P 500 posted three consecutive calendar years of double-digit percentage gains, recording its seventh best three–year stretch on record (WSJ).1 The U.S. economy, as bifurcated between economic classes as it has been, has held up better than many expected, even with the Federal Reserve’s tight posture from 2022 through most of 2024.2 However, beginning in September 2024, the Fed began loosening its stance by cutting the overnight lending rate and, more recently in December 2025, announcing an end to its quantitative tightening program. Some expect this shift toward net Treasury bill purchases could increase the Fed’s balance-sheet by $35 – $50 billion per month in 2026, potentially contributing to lower yields on the front end of the curve.

FEDERAL RESERVE BALANCE SHEET AND OVERNIGHT LENDING RATE

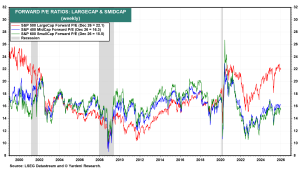

The stock market is a leading indicator of the U.S. economy but it’s not a perfectly clear crystal ball. Plenty of optimism has been reflected in asset prices, particularly that, by 2025’s year–end, the S&P 500 was trading at nearly 22x the forward price-to-earnings ratio, which is elevated relative to historical norms.3 Recent performance has largely coincided with expectations around tax reform, a policy pivot that leans pro-growth in the private sector, easier financial conditions, and expectations of a new wave of efficiencies brought on by artificial intelligence. These factors have kept forward valuations elevated relative to long-term norms.

FORWARD P/E RATIOS: LARGE-CAP VS MID-CAP

So, what’s next for the stock market, for the U.S. economy and for the U.S. consumer? This raises important questions about the sustainability of current market expectations as we move into 2026, given recent changes to both monetary and fiscal policy.

Trump 2.0: First Sour, Then Sweet

The Trump 2.0 economic playbook has been chronologically the opposite of Trump 1.0. In his second term, the president came out of the gate with what many refer to as the “sour” parts of policy – tariffs and tougher trade rhetoric, along with a willingness to lean into uncertainty in hopes of generating a more level footing with international trade.(4) Markets responded with extreme volatility at first, but after negotiations proceeded, the market appeared to look past trade uncertainty and continued to advance despite ongoing uncertainty.

As of today, financial markets have largely moved on from the tariff uncertainty and are instead pricing into the “sweet” portion of the agenda expectations: lower effective tax rates, looser financial conditions, and a friendlier environment for capital formation in 2026, potentially prompted by the One Big Beautiful Bill (OBBB).(5)

Policy uncertainty tends to come early, while benefits lag.

The risk, of course, is that most of the “sweet” news is already priced into equity markets, meaning outcomes in 2026 will need to hit on all cylinders to meet the optimism already baked into the markets.

The Core of 2026 Tax Reform

One of the major developments moving into 2026 is that tax reform provisions passed in 2025 are beginning to materially showing up on household and corporate balance sheets. Many of the provisions passed in 2025 don’t fully materialize until filing season and corporate budgeting cycles move into 2026.

The extension of the lower individual income tax brackets established under the Tax Cuts and Jobs Act (TCJA) provides a material increase in consumer tax refunds. Without congressional action, those brackets would have snapped back to higher, pre-2017 levels. With post-TCJA levels now made permanent, most middle-income households will continue to pay less in federal income tax than they otherwise would have.(6) Add to that inflation-adjusted thresholds for credits like the Child Tax Credit and Earned Income Tax Credit, and the average American family could experience an increase in after-tax income.

U.S. Treasury estimates and private-sector analysis suggest the average tax refund in early 2026 could increase materially – around 25% from roughly $3,000 per family in years’ past. That’s not life-changing money, but it’s not trivial either. It makes up a portion of the projected 0.9% boost to U.S. GDP that the Congressional Budget Office (CBO) & Joint Committee on Taxation (JCT) estimate could materialize in 2026 via the OBBB.(7)

What Does the Average American Actually Do with It?

Now, let’s be honest. Not every dollar of that refund turns into discretionary spending. Some of it goes to paying down credit card balances, some into savings, and some into rent checks or grocery bills that feel permanently inflated. But even if only a portion gets spent, the macro impact is still noticeable.

Some estimates suggest total refunds in 2026 could be 20-25% higher than recent norms, potentially returning $400–$425 billion in aggregate cash back into consumers’ pockets.8 With consumers spending roughly $21.15 trillion each year, an additional $200-$400 billion injected into the U.S. economy would only account for an additional 1-2% boost relative to previous norms.(9) That doesn’t sound like a substantial amount, but, again, considering much of the recent success in equity markets can be attributed to a surprisingly resilient consumer, we will likely require a healthy consumer to support continued economic and market momentum. When people feel like taxes aren’t quietly eating their hard-earned money away, they tend to become more flexible with their spending.

While it may not be stimulus in the 2020, COVID-style sense, it’s enough to keep demand strong and the consumer afloat. Anything helps given current valuations in equity markets.

Leverage on the Corporate Side

If the consumer gets a bump, corporate America could reap benefits that give it leverage.

Arguably, one of the most important aspects of the OBBB for businesses is the return of full expensing. Allowing companies to immediately deduct the cost of equipment, software, and R&D changes the math on investment decisions by pulling projects forward.10 This financial strategy encourages corporate executives to “go for it” and build an additional storefront, purchase new machinery, or – most relevant these days – build out AI-driven efficiencies. According to estimates from major investment banks and industry researchers, AI-related investment could top $500 billion in 2026. While tax policy doesn’t create that demand, it can help “green light” it.(11)

Goldman Sachs estimates that businesses could receive around $100 billion in tax-related cash flow benefits in early 2026 alone, much of which may be allocated to capital expenditures.

The Market Has Already Noticed

Equity markets have continued to ascend, even with expensive valuations. However, there are still plenty of ways things can go sideways. Deficits could push yields higher if economic growth can’t lessen the burden on our $38 trillion national debt.12 The Federal Reserve could challenge balancing persistent inflation against a weakening (or even an AI-disrupted) job market. None of these are base cases, but they aren’t off the table, either. Optimism and expectations are high, and any disappointment – whether it be underwhelming effects from policy changes, stubborn inflation, or global shocks – could lead to volatility. The consumer will need to realize the anticipated benefits from fiscal policy, while AI will need to deliver expected efficiencies, if equity markets are to align with current expectations. The U.S. economy has shown resilience, but resilience isn’t invincibility from risk.

Conclusion: Cycles Churn

In many ways, 2026 feels like a familiar cycle:

- Policy tightens, then loosens.

- Markets front-run reality.

- Consumers adapt.

- Businesses invest when incentives align.

Nothing is perfect, but things keep moving forward.

Tax reform most likely won’t pull the U.S. out of its record debt, nor will it miraculously restore affordability. But it does shift the odds modestly in favor of growth, and in an economy this large, even modest shifts can at least maintain an expansionary phase. Equity markets appear to have gotten a head start over “sweet” fiscal policy that is expected in 2026. Whether the fundamentals ultimately justify the current valuations will depend on earnings growth, execution on policy and the broader economic conditions.

SOURCES

- Wall Street Journal – “U.S. Stocks Defy ‘Sell America’ Warnings and are Ending 2025 Near Record Highs.” (December 30, 2025)

- Federal Reserve Board – FOMC Statements & Historical Federal Funds Rates; Federal Reserve press releases.

- FactSet – S&P 500 Forward P/E Ratios; Yardeni Research, S&P 500 Valuation Metrics

- CNBC – Trump Tariffs Inject More Uncertainty Into Global Economy (August 1, 2025)

- Tax Foundation – “FAQ: The One Big Beautiful Bill, Explained.” (July 23, 2025)

- IRS – One, Big, Beautiful Bill Provisions (July 4, 2025).

- CNBC News – “Your Tax Refund Could Be $1,000 Higher in 2026. Here’s Why.” (November 25, 2025).

- Tax Foundation – “Tax Refunds and the One Big Beautiful Bill Act.” (December 17, 2025).

- Federal Reserve Bank of St. Louis – Personal Consumption Expenditures (December 29, 2025).

- Cornell Law School – Accelerated Cost Recovery System.

- Goldman Sachs – “Why AI Companies May Invest More than $500 Billion in 2026.” (Dec. 18, 2025).

- Treasury.Gov – “Debt to the Penny.” (January 6, 2026).

This commentary is for informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Investing involves risk, including loss of principal. Forward-looking statements are subject to uncertainty and actual outcomes may differ materially.

This content is part of our quarterly outlook and overview. For more of our view on this quarter’s economic overview, inflation, bonds, equities and allocations, read the latest issue of Macro & Market Perspectives.