Great news, no one is getting a new job!

This year marks my 30th year in this industry, and I am still sometimes caught off guard when bad news for the economy is good news for the stock market. We had a very weak ADP employment report on Thursday, yet the stock market rallied most of the day on the news. The next morning, the August labor report showed more evidence that the job market is slowing, with a measly 22,000 jobs created last month. Per the Bureau of Labor Statistics, this economy had created 107,000 jobs, or just under 27,000 per month.

From the beginning of 2022 to April of this year — 40 months of data — we have had two months with job growth of less than 100,000 (78,000 in August 2024 and 43,000 in October 2024). There is no longer a question of whether or not the labor market is slowing, and the stock market knows that the Federal Reserve sees it, too. The market is now expecting a rate cut at the next Fed meeting on September 17.

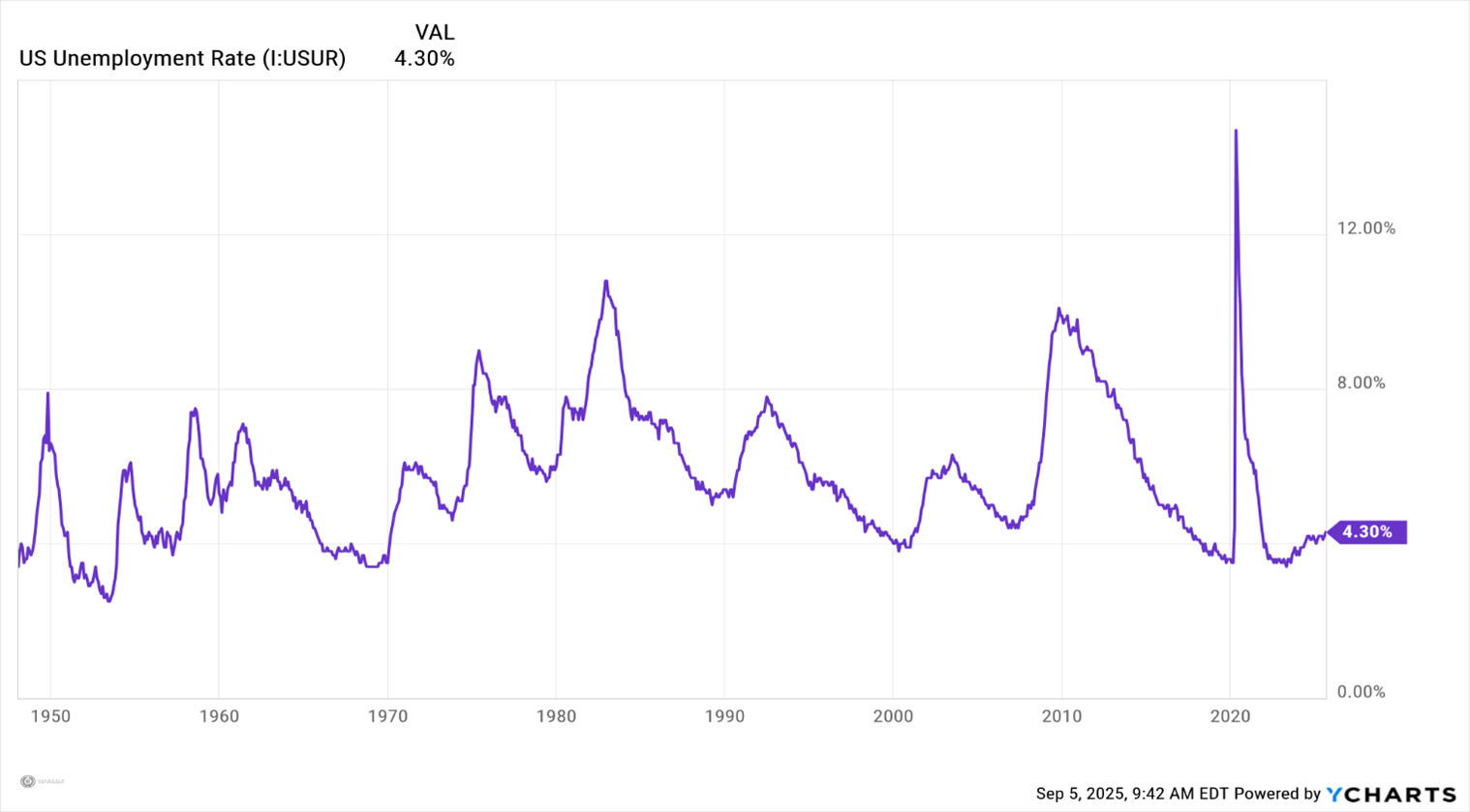

Now, I understand why the stock market rallied once it became clear that the Federal Reserve plans to reduce the Fed Funds rate in a week and a half, with a strong possibility that even more cuts are coming soon. The unemployment rate ticked up to 4.3%, the highest rate we have seen since late 2021, but if you look historically (see chart below), a 4.3% unemployment rate is still extremely low.

We are in what I would consider the “Goldilocks zone” with the labor market. It is weak enough to allow the Fed to cut rates, but not weak enough to have a negative effect on corporate earnings. Not many people are getting hired, but not many are getting laid off either. The consumer still has enough job security to continue spending.

We are just about done with 2nd quarter earnings season, which was much better than feared. With 98% of S&P 500 companies reporting, earnings are 11.9% above the 2nd quarter of 2024. That does not sound like a miserable economy, especially given all the uncertainty around tariff rates and potential price increases.

One thing that would be surprising is a combination of a weaking labor market and a strengthening consumer. Looking at that long-term unemployment chart, you can see that the unemployment number has been drifting higher for the past few years. Looking back, however, the unemployment rate in the past does not “drift up” for long periods of time. It will spike up due to a recession, and then drift lower throughout the remainder of that business cycle.

As consumer spending cools, corporate profits slide with it. In turn, corporations “adjust” their labor needs all at the same time, pushing unemployment rate higher. Before you know it, we have a recession. We are not there yet, and may not get there for some time.

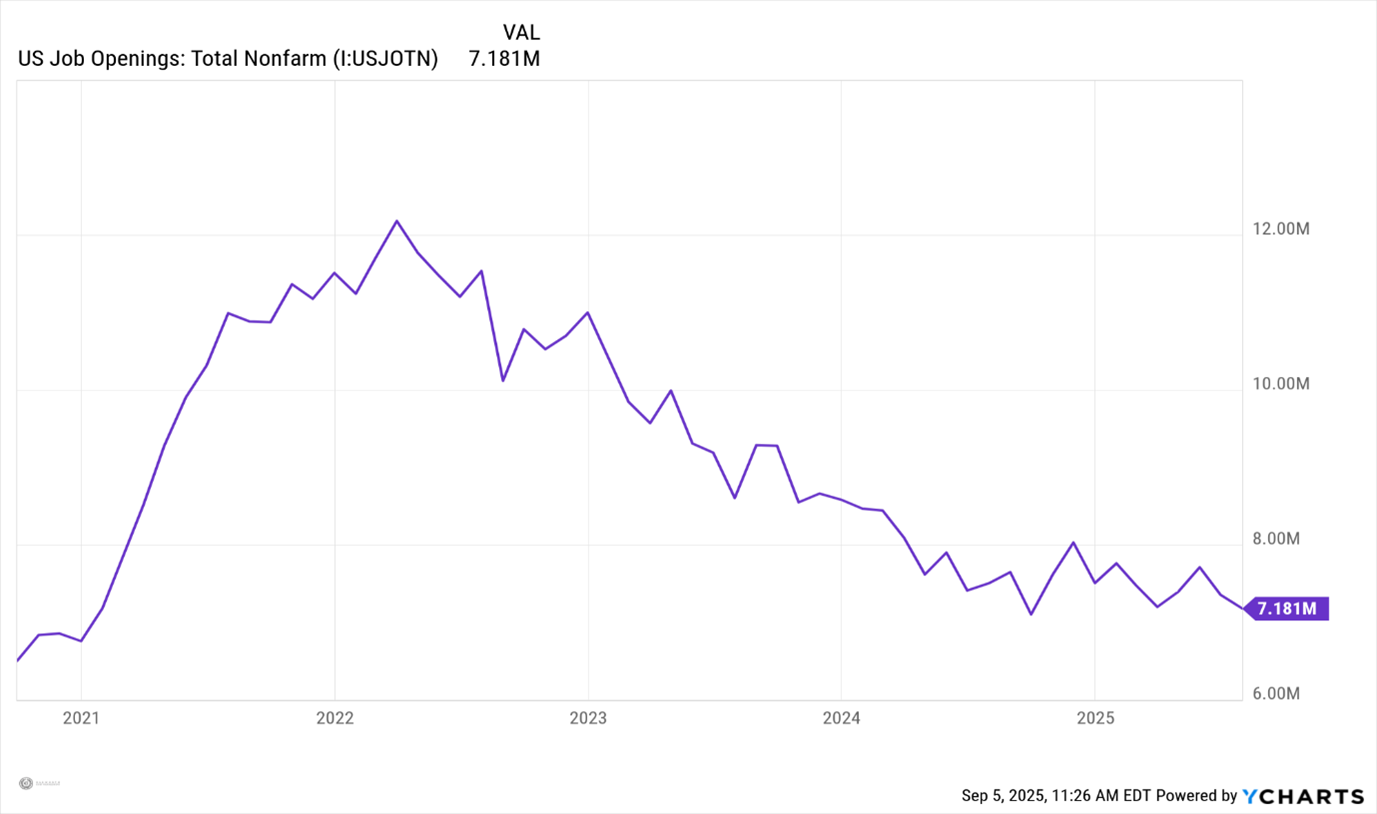

I try to look at the labor market in a simple way. Before a company starts reducing their workforce, two things could happen.

- First, a company would take down the help wanted sign.

In economic terms, this is the total number of job openings in the U.S., which was released on Wednesday. The 7.18 million job openings was lower than expected, and dropped from the peak of 12.12 million job openings recorded in March of 2022. We are now close to the levels seen pre-COVID.

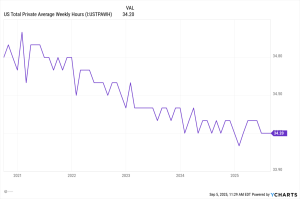

- Next, they would reduce the hours of the employees they have.

This number is included with the monthly job report, and you can see that this number has also been trending downward.

Just because a store owner took down the help wanted sign and reduced the hours worked by current employees does not mean that anyone is going to get laid off. But they might. And that is the best way to describe the current labor market.

The old proverb of “be careful what you ask for, you may get it” seems fitting here. The stock market rooting for the Federal Reserve to lower interest rates is understandable. If the labor market continues to weaken, however, and corporate profits start to drift lower, a lower Fed Funds rate may not be enough to lift investors spirits, or their net worth.

Thank you for your continued support. As always, I hope this newsletter finds you and your family well. May your blessings outweigh your sorrows on this and every day. Also, please be sure to tune into our podcast, Trading Perspectives, which is available on every platform.

David McGrath, CFA®

Managing Director, Portfolio Manager

This communication contains general information that is not suitable for everyone and was prepared for informational purposes only. Nothing contained herein should be construed as a solicitation to buy or sell any security or as an offer to provide investment advice. The information contained herein is based upon certain assumptions, theories and principles that do not completely or accurately reflect any one client situation. This communication contains certain forward-looking statements that indicate future possibilities. Due to known and unknown risks, other uncertainties and factors, actual results may differ. As such, there is no guarantee that any views and opinions expressed herein will come to pass. Investing involves risk of loss including loss of principal. Past investment performance is not a guarantee or predictor of future investment performance.

Any reference to a market index is included for illustrative purposes only as it is not possible to directly invest in an index. The figures for each index reflect the reinvestment of dividends, as applicable, but do not reflect the deduction of any fees or expenses, the incurrence of which would reduce returns. It should not be assumed that your account performance or the volatility of any securities held in your account will correspond directly to any comparative benchmark index. This communication contains information derived from third party sources. Although we believe these sources to be reliable, we make no representations as to their accuracy or completeness.

All opinions and/or views reflect the judgment of the author as of the publication date and are subject to change without notice.