For over a decade, international markets have been viewed as the slower-growing “little brother” to the United States — constrained by legislature, financially cautious and lagging in innovation. But in early 2025, that narrative began to change. A combination of fiscal spending, increased defense investment and improved global sentiment toward valuations of international equities has begun to reshape how international markets are viewed within the broader investment narrative.

The United States now stands at a pivotal moment. As its involvement in global affairs continues to evolve with a foreign policy shaped by an “America First” approach, it remains to be seen whether U.S. markets can sustain their longstanding leadership or whether recent performance reflects a broader, more durable shift toward international equities as market conditions evolve.

Global equities significantly outperformed domestic equities over the last year. There has been no shortage of headlines about this, with many commentators linking this to a shift away from U.S. dominance. But as is often the case with sensational headlines, there is always more to the story, and outcomes remain uncertain.

2025 EQUITY PERFORMANCE

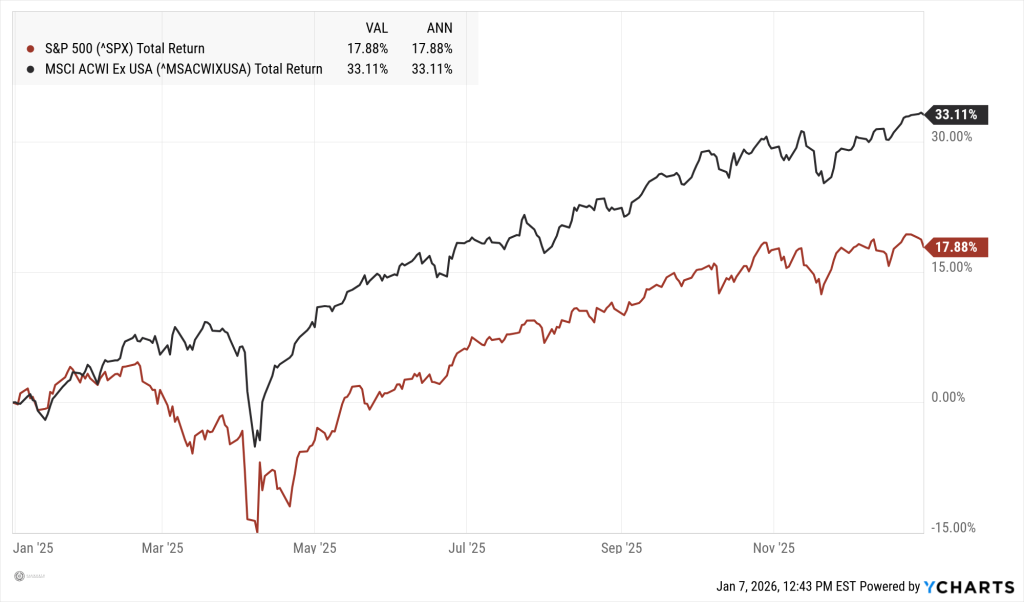

To lay the scene, we must first discuss international equity performance versus domestic equity performance in 2025. While there was no shortage of drama in domestic markets, it appeared to have little effect on the equity performance of U.S. companies over the course of the year. The S&P 500 index finished the year with a return of 17.88%1. This was driven in part by continued outperformance of the largest U.S. companies (the Magnificent 7), more specifically AI-related stocks that have continued to see strong growth (ex. NVDA) during the period. Additionally, Fed rate cuts began to materialize in the second half of 2025, and the labor market showed relative resilience with unemployment remaining historically low as we closed out the year.

At year-end, the Morgan Stanley Capital International All Country World Index ex. U.S. (or “MSCI ACWI ex U.S.” for short) gained approximately 33.11% in 2025, exceeding the S&P 500’s return over the same period. (1)

GLOBAL EQUITIES OUTPACE U.S. MARKETS IN 2025

INTERNATIONAL OUTPERFORMANCE

So, what happened? Did the Europeans suddenly create that much more value for shareholders in 2025 than the Americans?

Not necessarily. Instead, there was a fundamental shift in the ideology of fiscal policy, and broader geopolitical events may have driven some of the outperformance.

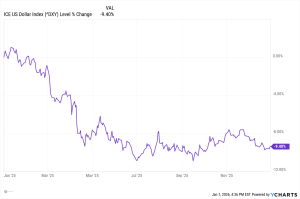

THE U.S DOLLAR

One major contributor that affected both Americans and Europeans was the weakness of the U.S. dollar. According to the ICE U.S. Dollar Index (DXY), in 2025 the dollar fell by over 9% relative to other international currencies.(2) [The U.S. Dollar Index (DXY) measures the value of the dollar against a trade-weighted basket of six major foreign currencies. You can find more about how it is calculated here: https://www.investopedia.com/terms/u/usdx.asp.]

One historical effect of the Fed rate cuts is a change in the relative value of currency. Historically, when rates go up, currency values strengthen, and when rates come down, so does the value of the currency. Though the relationship is not guaranteed, this dynamic appeared to play out in 2025 as the Fed cut rates at three different meetings throughout 2025.(3) Additionally, periods of policy uncertainty can affect investor confidence, and 2025 was volatile. This is especially true with monetary and fiscal policy, as unclear guidance can reduce the confidence of investors and reduce the demand for dollar-denominated assets, such as a historically long government shutdown.

This environment seemed to go hand in hand with trade imbalances, especially with the introduction of global tariffs in 2025. Importing more than we export can slowly increase the supply of dollars globally over time, putting downward pressure on dollar values.(2)

THE U.S. DOLLAR WEAKENS IN 2025

DEFENSE SPENDING IN EUROPE

Another major contributor to the relative outperformance of internationals was the changing geopolitical situation in Europe (and other regions), which spurred shifts in fiscal policy. A clear example is the ongoing war in Eastern Europe, which has prompted German policymakers to reassess and expand the country’s defense budget. German officials announced an approval in mid-2025 of a plan aimed to spend $761 billion on their military and infrastructure over the next five years.

The plan will allow German officials to conform to the updated NATO guidelines by 2029, which states that member countries should allocate at least 3.5% of their total GDP to a defense budget. Germany will finance the spending with $469 billion in new debt. This was only possible due to fundamental changes in their constitution, which normally limits borrowing to 0.35%. This, again, displays the tone shift in Europe.(4)

Investors responded by reallocating capital towards some of the largest defense companies in anticipation of the potential government defense contracts. Companies such as Rheinmetall (RHM.DE), Germany’s largest arms manufacturer, delivered significant returns over the past year. The stock gained 232% over the period, substantially outperforming most U.S. companies (YCharts). Time will tell if these valuations are justified, but speculative investors have not been deterred.

Investors are also closely watching geopolitical events, theorizing about market moves likely stemming from the most recent news. Time will tell whether these valuations are justified, and speculative investor interest has played a role in recent performance.

GEOPOLITICS

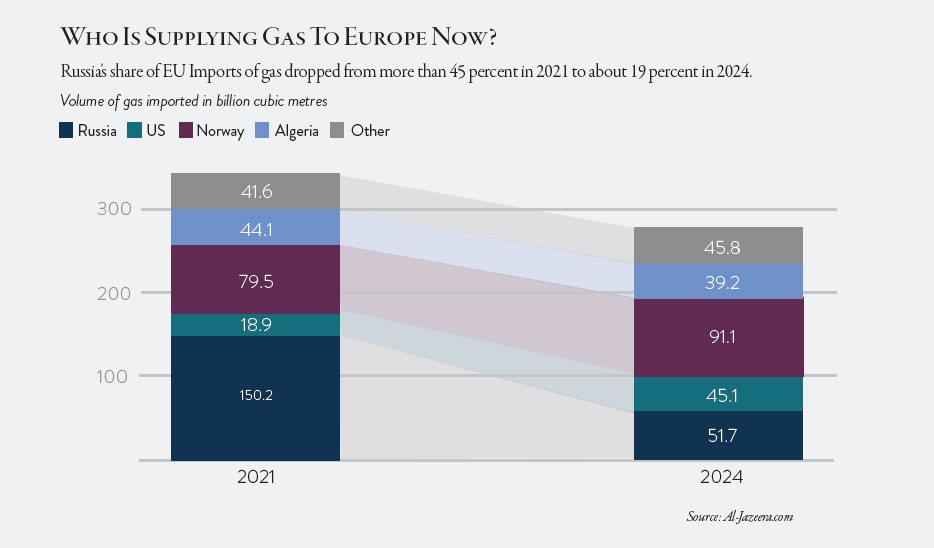

The ongoing conflict in Ukraine has also likely contributed to market volatility. Commodities produced by Russia have been severely restricted due to sanctions from most western countries, which has dwindled supply. Oil and natural gas are the most immediate commodities affected, mainly due to Europe’s reliance on imports pre-conflict.

- In 2021, Russia supplied Europe with 45% of its natural gas consumed and 27% of oil consumed.

- These numbers have changed drastically, with Europe only receiving 19% and 3% of natural gas and oil from Russia by the end of 2024.(5)

The current U.S. administration appears to prioritize bringing an end to the conflict, as de-escalation could reduce geopolitical risk, stabilize global markets and alleviate persistent supply chain and commodity disruptions that have weighed on economic growth.

This isn’t the only region where the current administration is seeking to influence foreign politics. In the Middle East, Washington continues to play a leading role in negotiation efforts amid ongoing disputes, while in the Western Hemisphere the U.S. has significantly escalated its involvement in Venezuela — seemingly daily — as part of a broader strategic push to further key economic interests.

Altogether, these geopolitical events have reshaped the current global market dynamics, especially in Europe. The recent changes to European fiscal policy and investment into their defense sector have seen short-term positive effects on economic activity, however these actions largely reflect responses to geopolitical pressures rather than a true growth initiative.(6) While there is momentum building in these once-sleepy markets, it’s important to look beyond the current situation and analyze the overall economic drivers of the region such as innovation, physical and human capital investment, government regulation and natural resource exploitation.

Taking these economic drivers into consideration, the Oakworth Investment Committee currently views U.S. domestic markets as offering structural characteristics supportive of long-term growth going forward, subject to change as conditions evolve. The United States continues to exhibit structural advantages over international markets. From the committee’s perspective, the U.S. retains key advantages, including deep and complex capital markets, a strong focus on innovation and technological leadership, and a more pronounced entrepreneurial spirit.

Europe’s recent outperformance appears primarily cyclical, supported by responses to geopolitical stress rather than sincere growth drivers. In contrast, the U.S. economy may be positioned to generate sustained earnings growth, if past performance gives us any insight into future results. As a result, the committee believes domestic equities are well positioned and could regain leadership over international markets as the global economy moves forward. But only time will tell – and future market leadership remains uncertain.

SOURCES

- YCharts – S&P 500 Annual Total Return for 2025

- NPR. – “Why the Dollar Fell Over 9% in 2025, and What to Expect in 2026.” (4 Jan. 2026), https://www.npr.org/2026/01/04/nx-s1-5662540/why-the-dollar-fell-over-9-in-2025-and-what-to-expect-in-2026

- Federal Reserve Bank of New York – Secured Overnight Financing Rate (SOFR). FRED, Federal Reserve Bank of St. Louis, https://fred.stlouisfed.org/series/SOFR

- Defense News – “Germany Plans to Double Its Defense Spending Within Five Years.” (26 June 2025).https://www.defensenews.com/global/europe/2025/06/26/germany-plans-to-double-its-defense-spending-within-five-years/

- Al Jazeera – “How Much of Europe’s Oil and Gas Still Comes from Russia?” (3 Oct. 2025). https://www.aljazeera.com/news/2025/10/3/how-much-of-europes-oil-and-gas-still-comes-from-russia

- “US Stocks Had a Stellar 2025, but Global Markets Stole the Show.” CNN, 4 Jan. 2026, https://www.cnn.com/2026/01/04/investing/global-stock-market-year-international

Past performance is not indicative of future results. This material is for informational purposes only and does not constitute investment advice or a recommendation. References to specific securities are for illustrative purposes only and should not be construed as investment recommendations. Indexes are unmanaged and not investable. Forward-looking statements are subject to uncertainty and change. Index performance is unmanaged and does not reflect the deduction of fees or expenses.

This content is part of our quarterly outlook and overview. For more of our view on this quarter’s economic overview, inflation, bonds, equities and allocations, read the latest issue of Macro & Market Perspectives.