Geopolitical tensions in the Middle East have escalated, though whether the situation qualifies as a formal war remains a matter of interpretation. Regardless of the label, financial markets have begun to price in rising risk, with oil serving as the primary transmission mechanism.

Oil influences nearly every corner of the global economy, including energy, transportation, manufacturing, pharmaceuticals and plastics. When conflict spreads in the world’s most oil-rich region, prices can rise quickly.

This development comes at a challenging time. The global economy remains in a late-cycle phase, still battling stubborn inflation tied to post-COVID supply bottlenecks and stimulus measures. Like a runner stranded on third, the expansion has come within sight of a soft landing—but can’t quite cross home. Each spike in oil prices pushes the game further into extra innings.

Beyond the human toll of conflict, the market implications have dominated headlines, driven largely by oil at a time when inflation still refuses to fully subside. The path forward appears increasingly constrained, given current conditions. What impact has the situation in Iran had on markets, how severe could it become and what comes next?

Control the Straight, Control the Story

“In war, truth is the first casualty.” —Aeschylus, ancient Greek tragedian

As with most fluid situations, a healthy dose of “we don’t know what we don’t know” is a useful starting point. This moment is no different. We’ve heard a range of stated and implied objectives, including:

- Preventing Iran from obtaining a nuclear weapon

- Destroying their ballistic missile capabilities

- Diminishing their naval capacity to eliminate a military response and limit disruption in the Strait of Hormuz

- Factoring in, to a lesser extent, the potential for regime change

These objectives have been described as partially achieved, according to public statements from administration officials. Whether that holds over time remains an open question, but the market is focused on something more tangible: control of the Strait.

Threats from Iran targeting the roughly two-mile-wide shipping lanes that vessels must navigate in each direction remain. Roughly 20% of global petroleum liquids are estimated to pass through this narrow waterway, creating a clear emphasis on safe and secure passage.

To achieve this, the U.S. may pursue a longer-duration policy stance aimed at influencing stability in the region, neutralizing surface-to-surface missiles, countering clusters of fast-attack boats, preventing mines from being laid and limiting submarine threats beneath the surface. This is not a small task, even for a highly capable military. Iran has been preparing for this type of asymmetric warfare since the late 1980s during the “Tanker War” with Iraq, refining those capabilities over decades.(1) The result is a layered defense strategy designed to overwhelm and complicate any external force.

Compounding the challenge are low-cost, high-impact tools such as drone systems like the Shahed-136. These drones can inflict significant damage on critical oil infrastructure at a fraction of the cost of traditional military assets.(2) Even the threat of disruption is enough to deter normal tanker traffic, especially when vessels worth approximately $100 million rely on insurance coverage that may not extend to conflict zones.

A Two-Sided, Yet Handcuffed, Oil Market

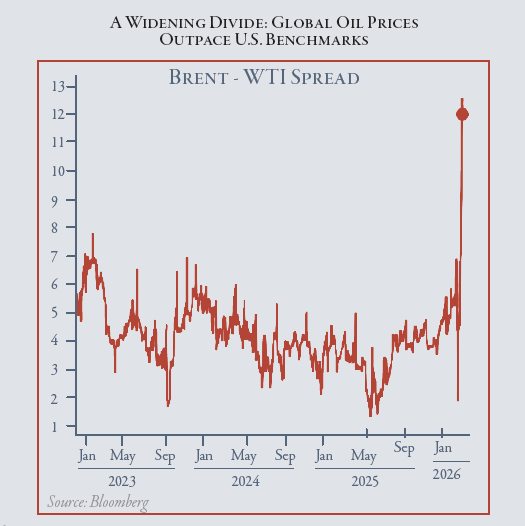

Within the global oil marketplace, there are two primary pricing benchmarks: Brent crude and West Texas Intermediate (WTI). Brent is seaborne and derived from North Sea production, making it a better barometer of OPEC+ output and Middle East tensions. WTI, priced in Cushing, Oklahoma, is influenced more heavily by U.S. domestic supply and inventory conditions. A widening Brent–WTI spread can signal tighter global seaborne supply relative to U.S. inland supply and often reflects disruption to international oil flows. As markets began pricing in potential disruption in the Strait of Hormuz, the spread between Brent and WTI widened sharply, reaching $17 per barrel intraday on March 19.(3)

So why does Brent matter to Americans if the U.S. is among the world’s largest oil producers? While both Brent and WTI are considered “sweet” crude, logistical constraints handcuff markets. WTI is landlocked, and transportation bottlenecks can restrict efficient distribution. U.S. refining capacity, approximately 18 to 19 million barrels per day, is insufficient to meet total domestic demand using only U.S.-produced crude.

Refineries are optimized for specific blends, and building new refining capacity would take years and require significant capital investment. As a result, the U.S. continues to rely on a mix of domestic production and imported crude.

At its core, oil is a global market. Over time, arbitrage mechanisms help keep pricing relationships in check, as traders can shift supply routes and absorb transportation costs when spreads become too wide. Oil is fungible, and over time, the market works to rebalance itself.

The Cost of Higher Oil and Gulf State Partners

Even if the shipping through the Strait of Hormuz stabilizes, oil prices may remain elevated. Longer-term pressures may persist, particularly due to the condition of oil and refining infrastructure across the region. The Islamic Revolutionary Guard Corps (IRGC), along with its proxy forces, has targeted oil infrastructure in neighboring Gulf states as part of a broader strategy to pressure oil-dependent economies into urging de-escalation.

If securing the Strait proves to be the shorter-term challenge, infrastructure damage presents a longer-term risk. This raises the possibility that oil may struggle to return to sub-$60 levels in the near term, even in the absence of direct disruptions to shipping lanes.

Similar to how global supply chains were reassessed following COVID-19 due to over-reliance on China, a parallel realization is emerging in energy markets: diversification is no longer optional—it is necessary.

While oil shocks can still push inflation higher in the short term, their long-term impact is increasingly shaped by broader forces such as monetary policy and supply chain dynamics. Oil above $90 per barrel may contribute

to inflationary pressures, which in some scenarios could influence U.S. 10-year Treasury yields, which have been elevated above 4.3%. In turn, higher yields can act as a headwind to equity markets in certain environments, which can limit valuation expansion and weigh on corporate growth expectations.

Conclusion

Historically, oil and inflation have been closely correlated, but that relationship has become far less linear.

Markets may respond positively to temporary pauses in conflict or optimistic rhetoric, but the underlying structure of this situation remains fragile. Control of the Strait of Hormuz is not a switch that can simply be turned on and off. It would most likely rely on a long-duration Geopolitical balancing act involving a wide-scale military operation followed by additional oversight. Even if worst-case scenarios are avoided, the margin for error appears limited under current conditions.

For investors, this reinforces a familiar theme: geopolitical risks are rarely linear and seldom fully priced in at the outset. Oil prices may continue to influence inflation prints and interest rates, while global supply chains shape longer-term market outcomes.

In the meantime, markets are left doing what they do best – reacting in real time to incomplete information, attempting to price a situation where, as always, the truth is still unfolding.

SOURCES:

- Brittannica, Strait of Hormuz, accessed March 25, 2026.

- Drone Warfare, Shahed-136: The Weapon That Rewrote the Economics of Air War, March 2026.

- Seeking Alpha, Oil divergence: Brent-WTI spread widens, Middle East benchmarks top $150, March 20, 2026.

Advisory Services, including investment management and financial planning, are offered through Oakworth Asset Management LLC a registered investment advisor and is owned by Oakworth Capital Bank, Member FDIC. Investment products and services offered via Oakworth Asset Management LLC are independent of the products and services offered by Oakworth Capital Bank, and are not FDIC insured, may lose value, have no bank guarantee, and are not insured by any federal or state government agency. Because of the ownership relationship and involvement by Oakworth Asset Management LLC associates with Oakworth Capital Bank, there exists a conflict of interest to the extent that either party recommends the services of the other. Oakworth Asset Management LLC does not provide tax or legal advice. You should consult your tax advisor, accountant, and/or attorney before making any decisions with tax or legal implications. For additional information about Oakworth Asset Management LLC, including its services and fees, send for the firm’s disclosure brochure using the contact information contained herein or visit advisorinfo.sec.gov.

This communication contains general information that is not suitable for everyone and was prepared for informational purposes only. Nothing contained herein should be construed as a solicitation to buy or sell any security or as an offer to provide investment advice.

The information contained herein is based upon certain assumptions, theories and principles that do not completely or accurately reflect any one client situation. This communication contains certain forward-looking statements that indicate future possibilities. Due to known and unknown risks, other uncertainties and factors, actual results may differ. As such, there is no guarantee that any views and opinions expressed herein will come to pass. Investing involves risk of loss including loss of principal. Past investment performance is not a guarantee or predictor of future investment performance.

Any reference to a market index is included for illustrative purposes only as it is not possible to directly invest in an index. The figures for each index reflect the reinvestment of dividends, as applicable, but do not reflect the deduction of any fees or expenses, the incurrence of which would reduce returns. It should not be assumed that your account performance or the volatility of any securities held in your account will correspond directly to any comparative benchmark index. This communication contains information derived from third party sources. Although we believe these sources to be reliable, we make no representations as to their accuracy or completeness.

All opinions and/or views reflect the judgment of the authors as of the publication date and are subject to change without notice.