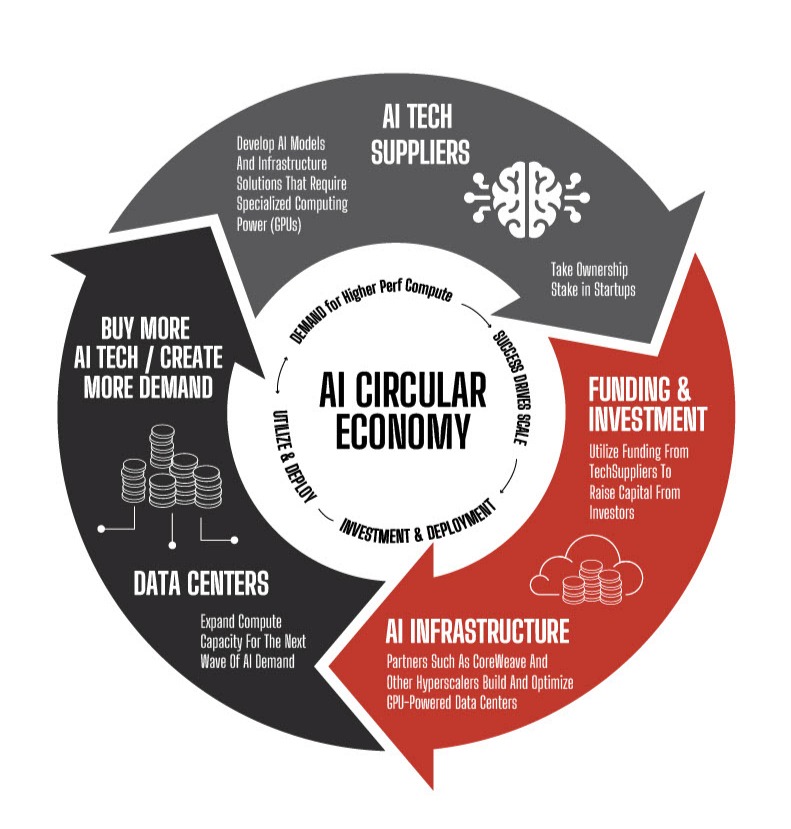

In a gold rush, the miners rarely strike it rich – it’s the companies selling the picks and shovels that do. This is termed “the picks and shovels play” and has been an interesting strategy employed across many different industries. In this dual role, NVIDIA has taken this to a new level —not only just acting as the supplier of picks and shovels, but stepping into the miners’ shoes, too. This illustrates how vertical integration can accelerate ecosystem growth. For years now, NVIDIA has been supplying the much-sought-after semiconductor chips that AI and Tech companies demand, growing the company into the largest in the world, with a market cap of $4.55 trillion. But that wasn’t enough – it is now investing directly into the companies that purchase its products and create infrastructure for the growing AI world. This has created a new “self-feeding” ecosystem that is isolated from the broader economy – but is becoming a larger and larger part of it.

It probably won’t come as a surprise when I say we are in the midst of a new gold rush – some have dubbed it the “AI Revolution”. While artificial intelligence has been in development for decades, it has only recently exploded into the zeitgeist since the COVID-19 pandemic. One of the largest contributors to this surge in popularity was OpenAI’s release of ChatGPT in late 2022, which revolutionized how people interacted with artificial intelligence. Its impact was immediate: companies and individuals alike saw its vast potential and raced to harness it.

This led directly to a boom in new AI startups. Some looked to compete directly with OpenAI and its large language models (such as Anthropic), while others tried to create useful applications using OpenAI as their engine. OpenAI’s business model includes selling access to their API, a backend solution to power new applications using its technology. This allowed the startups to leverage new technology without the massive cost and expertise required to develop large language models from scratch. Today, ChatGPT-style applications are everywhere, from Perplexity.ai, which specializes in deep-dive research, to my personal favorite, FinanceGPT, a finance-focused tool that provides AI-driven market analysis. But with this explosion of new applications, OpenAI must keep pace with demand — requiring ever more processing power, which translates into more data centers, and ultimately, greater reliance on NVIDIA’s all-important chips.

While startups were jockeying for the next round of funding, the largest tech players were gearing up for their own expansion into AI. Industry giants started to pour massive amounts of resources into their AI departments, hoping to increase the efficiency of their existing business model. According to the New York Times, Microsoft has allocated about $80 billion for AI infrastructure and data center spending in the 2025 fiscal year, while Meta has earmarked around $68 billion to build out their AI framework.1 Even search leader Google has entered the AI arms race, unveiling Gemini, its new flagship AI-driven chat tool. To realize these ambitions, companies are offering eye-popping compensation packages to the best AI talent—deals now rivaling the salaries of NBA and NFL stars.2

Despite the spending craze, it has not all been smooth sailing. Investors have started to question the return on investment for these huge capital expenditures, challenging businesses to rethink their approach. For NVIDIA, the current answer appears to be partnerships. Over the past six months, the company has announced several high-flying deals, aiming to invest in some of its largest customers. One of the most prominent deals is with OpenAI, which could see NVIDIA invest over $100 billion, an amount tied directly to how many chips OpenAI agrees to purchase and deploy, according to CNBC (September 22, 2025). Another is a $5 billion stake in fellow chipmaker Intel, aimed at co-developing custom data center and PC products.3 Investors have rewarded this strategy so far, as NVIDIA’s stock sharply increased following these announcements. In some cases, NVIDIA’s market cap increased more than the total amount pledged in the partnership.

And don’t think NVIDIA is only gunning for the top dogs. The largest company in the world has also made significant investments in the AI startup space, taking a 91% stake in cloud AI company CoreWeave, along with other smaller stakes in ARM Holdings, Applied Digital and others.4

*Source: MyTechMusings via X, Oct. 2025

These investments from NVIDIA represent a significant boost to the cash reserves for receiving companies. Flush with cash, most companies have opted to, you guessed it, purchase even more chips from NVIDIA. This phenomenon, often referred to as “circular financing,” is a self-reinforcing strategy in which a company invests in its own customers to accelerate their growth. That growth then drives increased demand for the company’s core products, boosting revenues and ultimately delivering a positive return on the original investment.5

An example from history can be found in the late 1990s with Intel. A subsidiary called Intel Capital was founded in 1991; its main purpose to invest in hardware, networking, and other PC startups to accelerate the adoption of personal computers worldwide. The investing arm began subsidizing PC makers that featured Intel chips inside, leading to the famous “Intel Inside” campaign, which can still be seen on computers today. Investors questioned the capital expenditures back then as well, stating that Intel was overspending and inflating the PC boom. This eventually led to an antitrust investigation in the late 90s and early 2000s, which culminated in a settlement that ordered Intel to change its licensing and marketing practices, eliminating what prosecutors called “hidden rebates” for companies using Intel’s chips.6 While this wasn’t the end of the story for Intel, many argue it fueled the flames of the irrational exuberance that technology companies saw at the turn of the century.

So — is this good or bad for the overall economy? The jury still is out, but we can examine the pros and cons of the strategy and its possible long-term effects.

One potential benefit that may arise is the co-development of new technologies through these partnerships. Chipmaking and AI programming require extreme expertise, and the hardware and software must work together in perfect harmony. If they are designed to work together from the start, the components may have a better chance of success.

Then there is the financing situation. It requires massive amounts of resources to create and train these large language models such as ChatGPT, and OpenAI itself is not yet profitable. The solution the market has seemingly proposed is to secure funding for this cutting-edge research from one of the largest and most profitable companies in the world, who also happens to understand the environment in which it operates.

On the other hand, there are some inherent risks with this strategy. Although NVIDIA’s stock growth has been nothing short of meteoric, it seems the stock has been priced to perfection. In the investing world, this means investors are assuming near-flawless performance with near-perfect conditions to justify the current price.

If the company experiences any significant hiccups, the house of cards could come crumbling down.

Some analysts have begun labeling the AI boom a potential bubble, pointing to the recycling of NVIDIA’s cash through its customer acquisitions and partnerships as evidence.7 Another potential downside comes from Intel’s history lesson. Their strategy was foiled by litigation, specifically anti-trust concerns. Being on the losing end of such cases has often prosecutors to break up these corporations, which would almost certainly reduce NVIDIA’s business moat in the AI space, which could spell the end of its dominance.

As the effects of this new-age gold rush continue to be seen, one thing is clear: AI and its ecosystem have come to dominate domestic markets in a way that few other industries have before. The technology sector now represents more than a quarter of the total S&P 500 weighting, with NVIDIA alone accounting for a staggering 8% of the total weight.

This raises an interesting question, is this explosive growth really driven by a technological breakthrough that has revolutionized efficiency? Or is it simply a self-feeding investment loop that has created artificial value? If these companies’ projected efficiencies are realized, current valuations could prove reasonable. However, if profitability expectations fall short, broad market valuations may adjust. Much like in the dot-com bubble, there is often a fine line between revolutionary technology and speculative market euphoria.

SOURCES:

- Investing.com – NVIDIA Stock Up as Meta Boosts AI Capex, Microsoft Datacenter Demand Not Slowing (April 2025).

- New York Times – AI Researchers Are Negotiating $250 Million Pay Packages (May 2025).

- Investing.com – Intel Gains AI Lifeline as Nvidia Invests $5B and Takes 4% Stake (September 19, 2025).

- HedgeFollow – Top 50 NVIDIA Corp Holdings

- The National Bureau of Economic Research – The Determinants of Corporate Venture Capital Success

- The Federal Trade Commission – Intel Corporation, In the Matter of 1999.

- Yahoo Finance – NVIDIA’s $100 billion OpenAI Investment Raises Eyebrows and a Key Question: How much of the AI Boom is Just NVIDIA’s Cash Being Recycled?

This material is provided for informational and educational purposes only and should not be construed as investment advice or a recommendation to buy or sell any security. The opinions and information contained herein are based on sources believed to be reliable, but their accuracy and completeness cannot be guaranteed. References to specific securities or companies are for illustrative purposes only and do not constitute an offer, solicitation, or recommendation for any particular investment strategy.

Past performance is not indicative of future results. Investing involves risk, including the possible loss of principal.