As featured in the Bay Business News.

One of the scariest phrases in investing is “it is different this time.”

Typically, it isn’t. A common thought is that history repeats itself — but if it doesn’t repeat, it may at least rhyme. In my view of current trends, today’s labor market appears to be changing, and that can be unsettling for both the economy and investors.

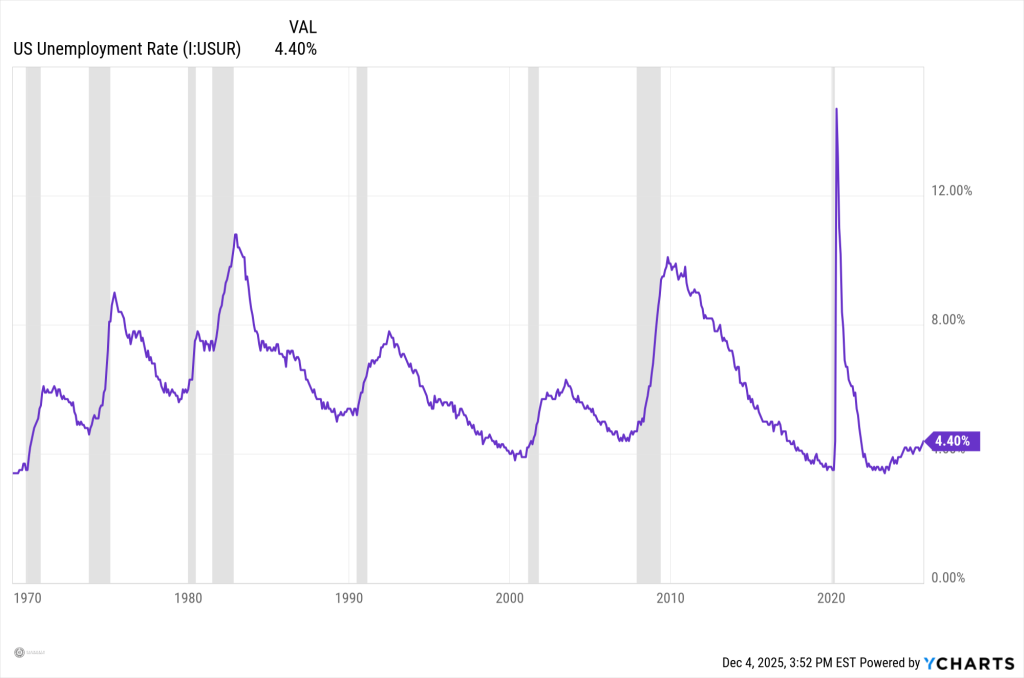

When the government shutdown finally ended on November 13, 2025, the September jobs report from the Bureau of Labor Statistics (BLS) was released a week later. It showed the unemployment rate moving up to 4.4%. Investors were very interested to see whether the labor market, which has been incredibly strong since the COVID recovery, was finally beginning to cool off. The answer seems to be yes.

In the past, a rising unemployment rate was almost always accompanied by a slowdown in economic activity and a recession. The past few years, however, we have seen a very strange combination: rising unemployment in the U.S., coupled with decent economic growth and strong corporate profits.

So, is it different this time? I would argue it may be, at least in the near term, based on current labor market dynamics.

We have seen the unemployment rate continue to drift up from the low of 3.4% we hit in April 2023. Historically, that kind of drift has often translated into bad news for the economy. Looking back, the unemployment rate does not usually drift up; it moves sharply higher, then drifts downward until the next recession.

Typically, a move higher in the unemployment rate is met with reduced corporate earnings. As consumers lose their jobs or have less confidence about their job security, they spend less. That slowdown in spending has a direct negative impact on the economy and on corporate profits.

That has not been the case for the past 29 months, based on currently available data. Even with the unemployment rate drifting higher for more than two years, the economy still seems to be in decent shape.

Why is it different this time?

First, that 3.4% unemployment rate was the lowest reading since September 1953. (For reference, the big new movie in theaters in 1953 was “Peter Pan.”) The average unemployment rate for the past 50 years is 6.13%, so a 4.4% unemployment rate is still very low. We have moved from a historically low level of unemployment to a more “normal” low level.

During COVID, the expanded unemployment benefits made staying home a viable alternate to work for many Americans. When the economy started to reopen, many companies had a difficult time finding workers to show up. Between 2021 and 2023, the economy was growing so quickly that normal business concerns around labor efficiencies took a back seat. The economy was on fire, fueled by all the cash that consumers had saved while being trapped at home for an extended period.

Restaurants and hotels seemed to be packed every day, and business owners could not afford to miss out by worrying about overpaying their staff. This is when some economists started using the term “labor hoarding” to describe the labor market.

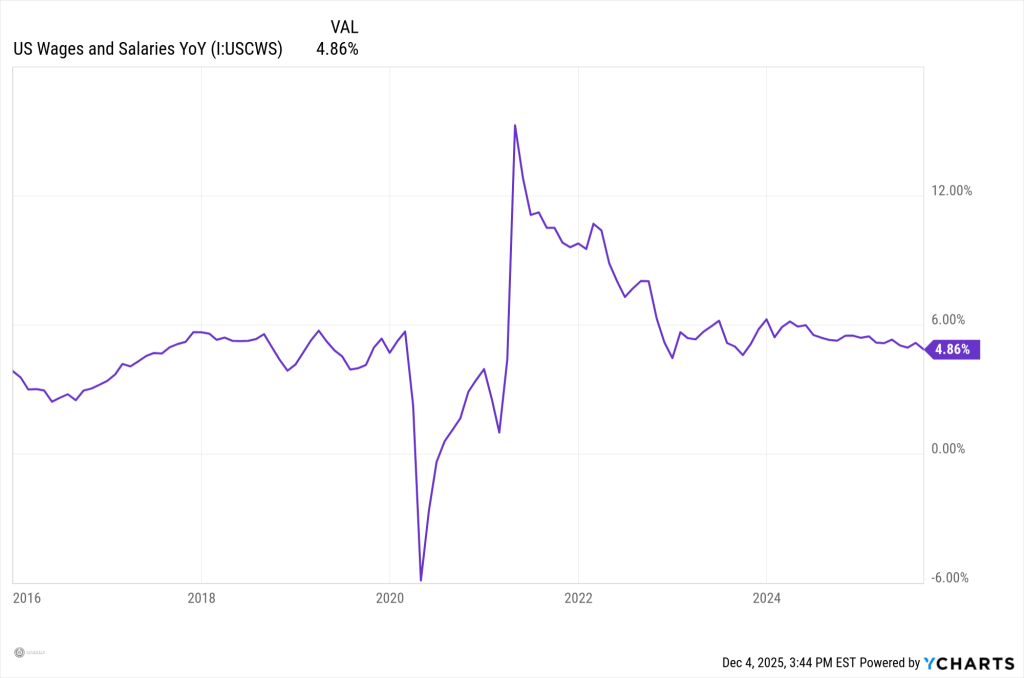

You can see that companies had to pay up to retain current (and attract new) employees. Wage growth has drifted down from a staggering high of 15.38% to a more normal 4.86%.

As we move farther away from those COVID years, the fear of not being able to hire enough employees is fading, and a refocus on efficient staffing levels has returned. I feel that the unwind of the “labor hoarding” trend from 2022 and 2023 accounts for much of the move up from the extremely low unemployment rate of 3.4% that we saw over the past 29 months.

Both corporate earnings and stock prices have moved up significantly since the unemployment rate bottomed in April 2023. In my view, the shift away from labor hoarding toward more efficient workforce levels may be contributing to improved corporate profit margins, though this can vary by industry and company.

Another factor that could be helping business efficiency is the slowdown of the work-from-home trend. There are varying studies on the productivity of work from home employees with mixed findings, and some studies and anecdotal evidence suggest productivity may be modestly lower in certain roles.

Many companies are now requiring employees to return to the office. Remote work is still higher than it was pre-COVID, but the trend seems to be reversing, and those productivity gains are helping improve corporate earnings as well.

There is also the emerging AI effect on the labor market. I do believe that we are still in a very early stage of AI implementation. Moving forward, however, the effects could become more significant. As AI becomes more widely used across industries, it is logical to believe that fewer new jobs will be created, at least initially.

Many entry-level, white-collar jobs should be an area where AI could have a significant impact. This may make it more of a struggle for recent college graduates to land that first “real job.” Like any new technology, however, the implementation of AI will also produce many new types of jobs that currently do not exist. Don’t be surprised if there is a lag time between some current jobs becoming obsolete and these new jobs being created. The quicker this group of young employees can adapt to this changing environment, the shorter that gap will be.

The efficiency gains that could be realized as businesses expand their use of AI should also help earnings move higher. As companies continue to unwind their labor-hoarding practices and start to gradually adopt AI, it is possible we could be looking at a very unusual combination: slowly rising unemployment coupled with continued economic growth and potentially solid corporate earnings growth for a much longer period than we have ever had. Whether such conditions persist, and for how long, remains uncertain and will depend on a variety of economic and policy factors.

The current 4.4% unemployment rate, with wages growing at 4.8%, is not, by itself a recipe for a weak economic environment in historical terms. As this economy transitions from the COVID era to the AI era, changes in the labor market will follow. An unemployment rate that drifts higher for an extended period may simply be a part of that transition. Over the past 60 years, that has not been great news for the economy.

I am not arguing that we cannot have a recession. There is always the chance that some out-of-left-field geopolitical event could cause economic growth to turn negative. Historically, in my lifetime, a rising unemployment rate has often been associated with economic slowdowns or recessions. Now, more than two years into a rising rate of unemployment, it seems that the rising unemployment rate alone may not be the recession warning that it has been in the past.

Oakworth Capital Bank is a financial institution focused on helping professionals, closely held businesses and families with generational wealth achieve their goals. With a commitment to personalized service, we offer a range of banking, wealth management and advisory services, creating tailored solutions that align with clients’ unique financial objectives and aspirations.

Advisory Services, including investment management and financial planning, are offered through Oakworth Asset Management LLC, a registered investment advisor. Oakworth Asset Management LLC is owned by Oakworth Capital Bank, Member FDIC. Investment products and services offered via Oakworth Asset Management LLC are independent of the products and services offered by Oakworth Capital Bank, and are not FDIC insured, may lose value, have no bank guarantee, and are not insured by any federal or state government agency. Because of the ownership relationship and involvement by Oakworth Asset Management LLC associates with Oakworth Capital Bank, there exists a conflict of interest to the extent that either party recommends the services of the other. Oakworth Asset Management LLC does not provide tax or legal advice. You should consult your tax advisor, accountant, and/or attorney before making any decisions with tax or legal implications. For additional information about Oakworth Asset Management LLC, including its services and fees, visit advisorinfo.sec.gov.

All opinions and/or views reflect the judgment of the authors as of the publication date and are subject to change without notice. This commentary is provided for informational purposes only and should not be construed as investment advice.