Both 2023 and 2024 were very kind to equity investors, with very strong returns for both years. With high valuations, and even higher levels of political uncertainty as we entered 2025, there was some concern from investors that a third consecutive year of strong market returns may be difficult to sustain. Nevertheless, 2025 equity markets ultimately delivered another year of positive returns.

The 2.4% return the S&P 500 posted in the fourth quarter of 2025 did not show the same sizeable gains seen in both the second (7.8%) and third quarters (10.6%) but it did absorb quite a bit of volatility and end the quarter with a positive return. And like 2023 and 2024, the Magnificent 7 stocks (for the most part) led the way. This past year was a bit more of a broad rally than the previous two years, but the continued buildout of AI infrastructure played a major part of the move higher over the past 12 months.

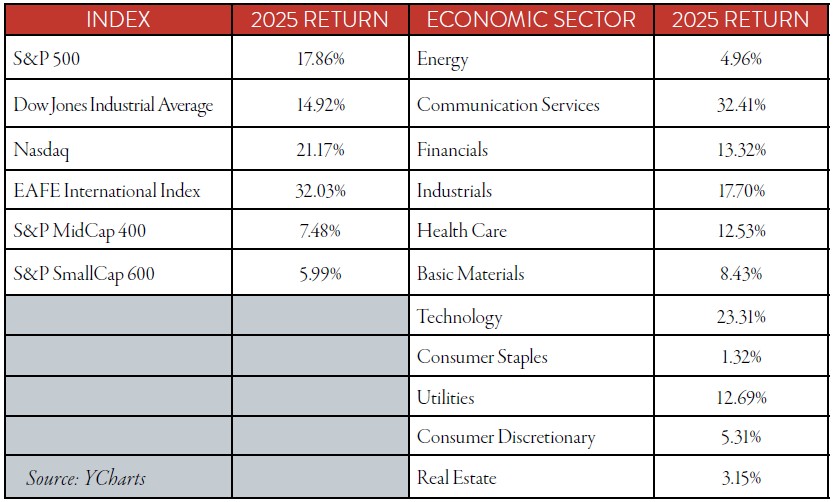

U.S. Equity Markets Rebounded in 2025

Looking at the performance of the economic sectors last year, it is not a surprise to see both technology (+23.3% in 2025) and communication services (+32.4%), the home of many of the largest growth stocks, show the best returns of the year. The third best performing sector may come as a surprise, and that is the industrial sector, posting a return of 17.7% last year. All of those new data centers supported demand for companies such as Caterpillar (CAT, +60.3%) and electric power provider GE Vernova (GEV, +99%).1, 2

It was also a turnaround year for aerospace giant Boeing (BA, +22.7%), which provided significant opportunity for General Electric (GE, +85.7%), which makes engines for Boeing.

The other eight economic sectors all underperformed the S&P 500, with the worst returns from the consumer discretionary (+1.3%), real estate (+3.2%) and energy sectors (5.0%). Also, the smaller stocks, represented by the mid-cap (+7.5%) and small-cap (+6.0%) indices, underperformed the large-cap stocks again in 2025.

After the market’s overreaction to the tariff announcement in early April 2025, stocks moved higher on the absence of added inflationary pressures from the new tariffs and the impact of the One Big Beautiful Bill Act passed last summer.

During the second half of 2025, stock prices were driven by the odd combination of a weakening labor market and increasing corporate profits. I say this is an odd combination because the “normal” sequence of events is that rising unemployment leads to falling consumer confidence, slower consumer spending and lower corporate profits.

The second half of 2025 delivered rising unemployment rates and falling consumer confidence — however, the last six months of the year gave us very consistent consumer spending and solid corporate earnings growth.

How did that happen? And more importantly, can it continue into 2026 and beyond?

One potential rationale is that the labor market from the beginning of the COVID pandemic has been heavily in favor of the workers. Many companies seemed to have over-hired, with fear that employee turnover would continue to be high.

Back in 2022 and 2023, with consumers full of excess cash and spending freely as the economy reopened, management was far less concerned with labor efficiency than with being fully staffed. Profit margins were somewhat compressed, but top-line sales growth was so strong that the efficiency losses were not impactful to earnings. This led to the lowest unemployment rate since the 1950s, alongside a surge in consumer confidence and spending.

By the start of 2025, the vast majority of that excess cash had been burned through, and companies were able to focus on the efficiency of their labor. With a slowing economy, worker turnover slowed and companies found themselves overstaffed. In the second half of 2025, they simply stopped hiring.

As employees left for a different opportunity, or retired, their positions were not replaced. The unemployment rate, which reached a low of 3.4% in April 2023 and started 2025 at 4.1%, drifted up to 4.6% as we finished the year.

That easing labor pressure allowed corporate profit margins to increase in 2025, allowing for strong earnings reports.

The key part of this story is that consumer spending remained solid, even with unemployment rising and consumer confidence numbers falling.

But how?

One potential answer is the stock market itself. Recent Federal Reserve data shows the top 10% of households own somewhere between 87% and 93% of all stocks.3 With very large stock market returns in six of the past seven years, that group has seen trillions of dollars added to their balance sheets since the start of the COVID pandemic. This is the same group of consumers that represents a significant share of current spending.

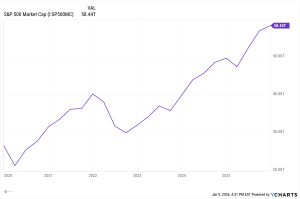

S&P Market Capitalization Reaches a New High

The S&P 500 has seen an increase of $36 trillion in market value since the start of 2019.4 That is roughly $32 trillion in net worth added to the top 10% of consumers over the past seven years.

In an odd way, both the stock market and the economy have the same dilemma, both being very “increased in concentration.” The largest 10 stocks in the S&P 500 account for more than 40% of the weight in the index, and (according to Moody’s Analytics) the top 10% of consumers account for 49.2% of all consumer spending.

Rising unemployment rates, coupled with inflation reports that failed to increase from tariffs, allowed the Federal Reserve to lower the Fed Funds rate at their last three meetings of the year.

They did the exact same thing in 2024.

Historically, a lower Fed Funds rate has been positive for stock prices, and that appeared to be the case in 2025. In the end, several key components were in place that supported higher stock prices:

- The Fed lowering interest rates

- Corporate profits moving higher

- Continued growth in consumer spending

This combination has historically been a winning hand for equity owners, and that was the case again last year.

This leads to the most important question: can the stock market keep moving higher given a weakening labor market and a consumer running low on confidence?

Looking Forward

The mix of strong corporate profit growth and an accommodative Federal Reserve would be a welcome sight in 2026, though outcomes are yet to be realized. According to Factset, S&P 500 earnings estimates for 2026 are currently expected to be roughly 15% higher than 2025.

That is an optimistic outlook given the state of the labor market. We would need to see a repeat of 2025 — with corporate profit margins continuing to increase amid softening labor markets, without a corresponding slowdown in consumer spending.

That was a cool trick the market was able to pull off in 2025, but can it do it again in 2026? For now, achieving those expectations would likely require continued margin expansion without a significant slowdown in consumer spending.

AI investments made over the past few years may begin to materialize, potentially contributing to a gradual rise in unemployment and improving corporate profit margins.

Sound familiar?

At some point, new jobs will start to emerge with the new AI economy, and that could potentially counter some of the jobs that AI will eliminate. Could the massive AI infrastructure buildout continue to grow at the torrid pace seen over the past few years?

Concerns over resource demands (e.g. electricity and water) could start to slow the growth rates moving forward. This issue has been raised in the past few years, with very little impact on the growth rate. Don’t be surprised if rising costs for residential electricity and water start to make this a political issue in 2026.

In the last few months of 2025, we began to see increased volatility as questions emerged about whether AI stocks were in a bubble. Early in my career, I remember a speech that Alan Greenspan, former chairman of the Federal Reserve, gave to the American Enterprise Institute. That day is remembered for a question he answered about stock prices becoming inflated beyond their fundamental value.

That is when he used the phrase “irrational exuberance” for the first time.

That phrase has been in the vocabulary of investors ever since. Many tie his answer to the end of the dot com bubble. Greenspan first used that term to describe stock valuations on December 5, 1996 — but the dot com bubble didn’t burst until March 2000, almost 40 months later. During those 40 months, the NASDAQ composite index move up 288% (from December 5, 1996, to March 10, 2000, according to YCharts).

Predicting the end of a market run or a turning point remains difficult. That does not mean investors should ignore fundamentals or valuation, and our Investment Committee continues to emphasize positioning portfolios to balance potential returns while managing risks.

The longer we move into this phase of the AI infrastructure buildout, the more challenging that balancing act becomes.

The Federal Reserve will see a new chairman in 2026, and the markets are anticipating a more “dovish” stance. One issue that may pose a problem for the next chairman of the Fed in 2026 is pesky inflation numbers. Consistent consumer spending has kept core inflation well above the 2% target of the Fed. The weakness in the labor market allowed the Fed to bring rates down in 2025, but how much lower can the Fed Funds rate move without some help from lower inflation numbers?

There are two main drivers of higher stock prices:

- Earnings growth

- Valuations move higher.

The market usually gives a higher valuation to the stock market with falling interest rates, so more moves from the Fed could help. Already trading near a historically high P/E ratio, future returns may rely more heavily on earnings growth to push us higher.

If we are able to get 7% to 9% earnings growth in 2026, and valuations remain stable, we could potentially have another positive year for equity markets, though outcomes depend on multiple factors and are not assured. Add on the just-over 1% yield of the S&P 500, and a total return of 8% to 10% for equity holders in 2026 would be a welcome sight.

SOURCES:

- Yahoo Finance – “Caterpillar (CAT) Finds a New Growth Engine in Data Center Power Demand.” (January 2, 2026)

- Morningstar – “20 Stocks in the S&P 500 that Gained the Most in 2025.” (January 1, 2026)

- Seeking Alpha – “Deeper Dive: The Wealthiest 10% of Americans Own 90% of the Stock Market.” (July 2, 2025)

- Y Charts – S&P 500 Market Cap

This commentary is for informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Investing involves risk, including loss of principal. Forward-looking statements are subject to uncertainty and actual outcomes may differ materially.