In a lot of ways, the 3rd quarter of 2025 was one of the more boring of my career. With everything happening in the world right now, that might seem like a crazy statement. However, when it comes to investing and dissecting economic data, it was about as plain vanilla as it gets.

Simply put, many investors continued buying stocks while the official economic reports remained somewhat lackluster, mediocre even. The only question anyone had was whether the Federal Reserve would eventually cut the target overnight lending rate.

As we all know by now, it did so at the Federal Open Market Committee (FOMC) meeting on September 17, 2025. Further, it (mostly) left the door open for more rate cuts in the future. Frankly, this wasn’t terribly surprising.

The reasons are simple: official inflation gauges are much lower than they were a couple of years ago, and the U.S. labor market doesn’t appear to be as strong as it was. Yes, inflation is still higher than the Fed’s stated target of 2.0%, and the official Unemployment Rate was a low 4.3% in August 2025.

However, given where the upper bound of the overnight rate stood at the start of the 3rd quarter, 4.50%, and where the trailing 12-month Consumer Price Index landed in August 2025, 2.9%, the Fed had a little wiggle room to do something if it so desired and thought it prudent.

Apparently, it did. Frankly, after waiting for so long for this cut, it was sort of anticlimactic.

Of arguably greater interest were the continued stories behind gold and artificial intelligence (AI).

The shiny stuff has s has appreciated significantly throughout 2025. According to Bloomberg Financial, the “Generic 1st Gold Future” closed the 3rd quarter at $3,840.80 an ounce. At the end of 2024, one ounce would have set you back, if that is the right phrase, $2,641.00. Obviously, that is quite a move in a short period of time.

- Is it due to foreign central bank demand? That is certainly some of it.

- Growing mistrust of the global financial system? That could be part of it.

- Increased acceptance of commodities as an asset class for retail investors? There is probably some of that.

- A fear of missing out on a rally, a FOMO trade?? I suspect that is in the mix as well.

The truth is gold’s recent strength is probably a combination of all of it.

As for AI, it seems the mere mention of it in a business model is enough to get investors frothing at the mouth. While that statement is obviously hyperbolic, after a difficult start to the year, the AI sector has been on a period of strong performance in U.S. stock markets . This, even as folks are beginning to question its ability to upend jobs and entire industries. However, while the ultimate economic upheaval in the future remains to be seen, investors appear to be focusing on growth in the here and now.

All told, while there was a lot happening around the world during the 3rd quarter of 2025, it was still sort of boring in a lot of ways. While, again, that might sound a little crazy, investors will take positive and boring over negative and exciting any day.

Thank you for your continued support,

John Norris

Chief Economist & Chief Investment Officer

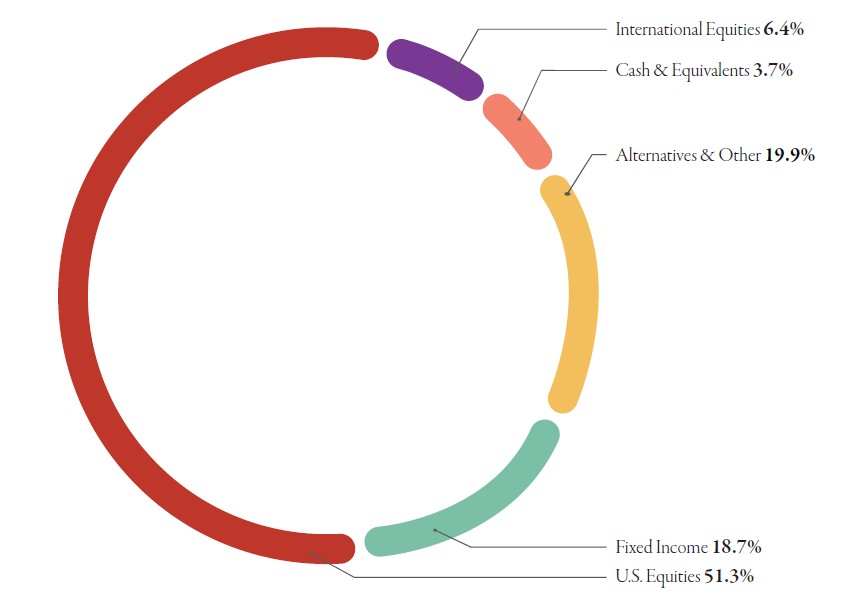

As of September 30, 2025, Oakworth Capital currently advises on approximately $2.52 billion in client assets. The allocation breakdown is in the chart below.

The views expressed herein reflect the opinions of the author as of the date of publication and are subject to change without notice. This material is for informational purposes only and should not be construed as investment advice or a recommendation regarding any security, strategy, or market sector. Past performance is not indicative of future results. All market and economic data are obtained from sources believed to be reliable, but accuracy cannot be guaranteed.