We’ve all seen it: a game that looks competitive on paper but is effectively decided in the opening minutes. I’m not talking about the typical David vs. Goliath matchup that college powerhouses schedule early in the season. Rather, I mean those supposedly competitive games where one team jumps out to a 10-point lead, and the two sides basically trade baskets for the remaining 35 minutes.

Of course, you’ve seen it. These games are dull and nearly devoid of energy—sports on autopilot, or cruise control.

In many ways, this is a fitting analogy for the U.S. economy during the first quarter of 2026. Despite the barrage of headlines and global uncertainty, where the rubber meets the road, the economic data was fairly uneventful. If you liked the fourth quarter of 2025, you probably liked the first three months of 2026.

If basketball isn’t your thing, consider a food analogy. The first quarter was the economic equivalent of a chicken-and-rice casserole, or maybe poppy seed chicken. Something along those lines.

One more? If the U.S. economy in the first quarter of 2026 were a rock ’n’ roll band, it would be either Styx or Journey.

There, I’ve said it.

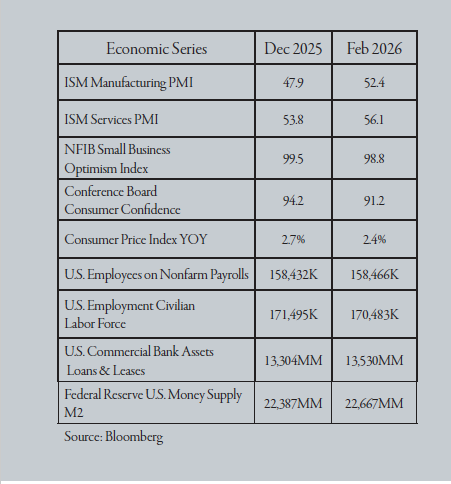

Following the underwhelming fourth-quarter 2025 gross domestic product (GDP) reading of 0.7%, it is unlikely the U.S. economy gained much momentum to start 2026—at least, that’s what the data suggest. The following table shows the final reading for 2025 and the most recent observation as of March 30, 2026. All data in the table is sourced from Bloomberg Financial.

While some of the data may be “Greek” to those who don’t closely follow the economic release calendar, the overall picture is fairly straightforward. In aggregate, the data appears satisfactory. It does not point to a sharp acceleration in economic activity, but it certainly does not signal an impending economic collapse, either.

In truth, January and February were about as uneventful as it gets when it comes to analyzing—perhaps overanalyzing—economic reports.

Then came March.

On Feb. 28, 2026, the United States and Israel launched a coordinated, large-scale attack on Iran, contributing to increased volatility in energy markets. Not surprisingly, the price of crude oil rose sharply as the conflict escalated.(1)

Perhaps even less surprising, this created uncertainly about future economic growth and inflation. As a result, the world’s investment markets fell.

Suffice it to say, many investors appear reluctant to hold “risky” assets when tensions in the Middle East escalate. Longer- term interest rates climbed as investors seemingly grew more comfortable avoiding long-duration risk, favoring cash over longbonds.2 Meanwhile, the domestic stock market, represented by the S&P 500, posted one of its worst months in recent memory. From the end of February 2026 through March 27, the index delivered a total return of approximately negative 7.32% for this index.3 Unsurprisingly, many investors are unlikely to be pleased with their first-quarter 2026 statements.

Even so, investment returns are one thing and economic activity is something else. While they might move together at times, there is no guarantee they always will.

Just because investors may be acting rationally does not mean they are always right. As of March 31, 2026, it remains unclear what impact this past month’s geopolitical turmoil has had on U.S. consumer activity and overall economic growth. My personal experience suggests not much has changed.

Put another way, if the rise in crude oil prices and heightened geopolitical tension have had an immediate, negative effect on domestic economic activity, there has been little observable evidence of a measurable shift in consumer behavior.

Traffic on Interstate 65 south of Birmingham remains as heavy as ever. In Atlanta, Interstates 85 and 75 are still the parking lots they’ve long been. Congestion around Greenville, South Carolina, continues to frustrate, as does Interstate 77 heading west toward Huntersville and Davidson, North Carolina.

In short, there are still too many people going too many places to buy too many things. And, of course, plenty of trucks are on the road.

The restaurants I visited in March were full, as were grocery stores and gas stations. Service at these establishments was dispassionate and often painfully slow. In other words, it was business as usual. Nothing changed in my daily work activities. In fact, I might argue things were a bit busier in March than in January or February. Most of my co-workers would likely say the same.

In our view, through the end of March 2026, and based on anecdotal evidence, any economic slowdown in the U.S. attributable to the conflict in Iran has likely not been significant enough to push first-quarter GDP into recession. However, because the war in the Middle East IS such a wildcard, it is difficult to make concrete predictions about the near term or to estimate March’s economic data with precision.

At its core, the situation comes down to some very basic questions that, as of late March, no one can answer with any certainty:

- How high will the price of crude oil ultimately rise? (4)

- How long will it remain at that level?

- And how will the Trump administration respond to countries that did not support the United States in its war against Iran?

This brings us back to what we do know—or think we know—with greater confidence: January and February. As noted earlier, the economy was, for the most part, fairly dull at the start of the year. To be sure, the now-familiar angst about artificial intelligence (AI) remained alive and well.5 The labor market continued to suggest a “low-hire, low-fire” environment—neither particularly strong nor week.

Official inflation data showed modest improvement, even if that did not always align with the experiences of those doing the grocery shopping. Banks were extending a reasonable level of credit, and the money supply was growing at a steady pace. January’s trade balance came in slightly better than expected, though that series has become increasingly difficult to predict.

All told, prior to March, I would have estimated first-quarter 2026 gross domestic product (GDP) growth in the range of 2.25% to 2.50%, even without knowing the final month’s data. After March, however, the outlook is far more uncertain, and I would hesitate to offer a prediction until just before the Bureau of Economic Analysis (BEA) releases its estimate. That is, if I still participated in those surveys, which I do not.

In conclusion, the U.S. economy in the first quarter was likely not as eventful as headlines may have suggested. In fact, it was fairly uneventful, at least in terms of the economic data. In many ways, it was like eating a chicken-and-rice casserole while watching a lopsided basketball game with Styx playing in the background.

Then, along came March, and we may simply have to believe whatever the government ultimately tells us about the economy for the month.

SOURCES:

- CME Group, Crude Oil Futures Quotes

- U.S. Department of Treasury, Daily Treasury Rates.

- Yahoo Finance, S&P 500, accessed March 31, 2026.

- CNBC, Brent Oil Heads for Record Monthly Surge, WTI Settles Above $100 for First Time Since 2022, March 29, 2026.

- Yahoo Finance, 30% of Americans Worry that AI Will Make Their Jobs Obsolete, March 30, 2026.

Advisory Services, including investment management and financial planning, are offered through Oakworth Asset Management LLC a registered investment advisor and is owned by Oakworth Capital Bank, Member FDIC. Investment products and services offered via Oakworth Asset Management LLC are independent of the products and services offered by Oakworth Capital Bank, and are not FDIC insured, may lose value, have no bank guarantee, and are not insured by any federal or state government agency. Because of the ownership relationship and involvement by Oakworth Asset Management LLC associates with Oakworth Capital Bank, there exists a conflict of interest to the extent that either party recommends the services of the other. Oakworth Asset Management LLC does not provide tax or legal advice. You should consult your tax advisor, accountant, and/or attorney before making any decisions with tax or legal implications. For additional information about Oakworth Asset Management LLC, including its services and fees, send for the firm’s disclosure brochure using the contact information contained herein or visit advisorinfo.sec.gov.

This communication contains general information that is not suitable for everyone and was prepared for informational purposes only. Nothing contained herein should be construed as a solicitation to buy or sell any security or as an offer to provide investment advice.

The information contained herein is based upon certain assumptions, theories and principles that do not completely or accurately reflect any one client situation. This communication contains certain forward-looking statements that indicate future possibilities. Due to known and unknown risks, other uncertainties and factors, actual results may differ. As such, there is no guarantee that any views and opinions expressed herein will come to pass. Investing involves risk of loss including loss of principal. Past investment performance is not a guarantee or predictor of future investment performance.

Any reference to a market index is included for illustrative purposes only as it is not possible to directly invest in an index. The figures for each index reflect the reinvestment of dividends, as applicable, but do not reflect the deduction of any fees or expenses, the incurrence of which would reduce returns. It should not be assumed that your account performance or the volatility of any securities held in your account will correspond directly to any comparative benchmark index. This communication contains information derived from third party sources. Although we believe these sources to be reliable, we make no representations as to their accuracy or completeness.

All opinions and/or views reflect the judgment of the authors as of the publication date and are subject to change without notice.