Financial Highlights

26% increase in core net income* 1Q22 vs. 1Q21

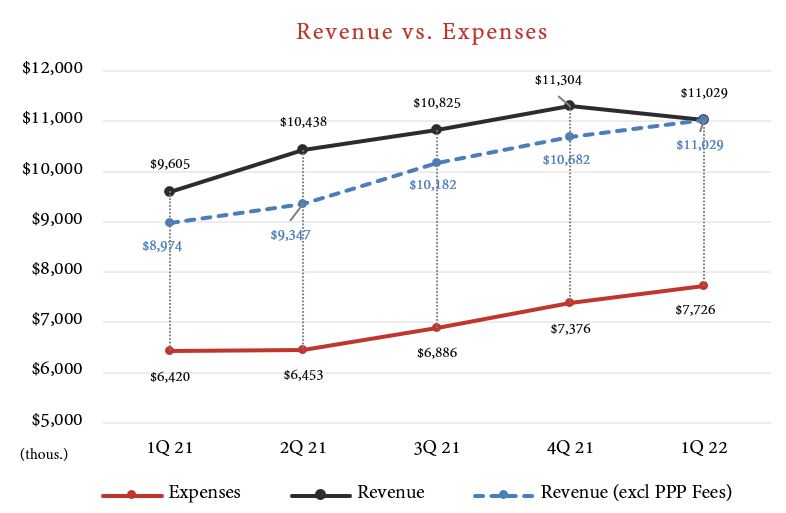

26% increase in core revenue

40% increase in pre-tax, pre-provision income

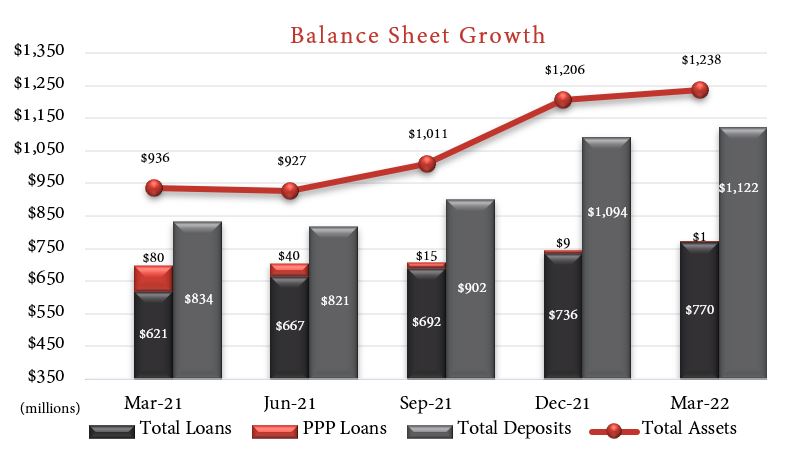

32% growth in total assets to $1.2 Billion**

24% year-over-year core loan growth (excluding PPP balances)

35% year-over-year deposit growth

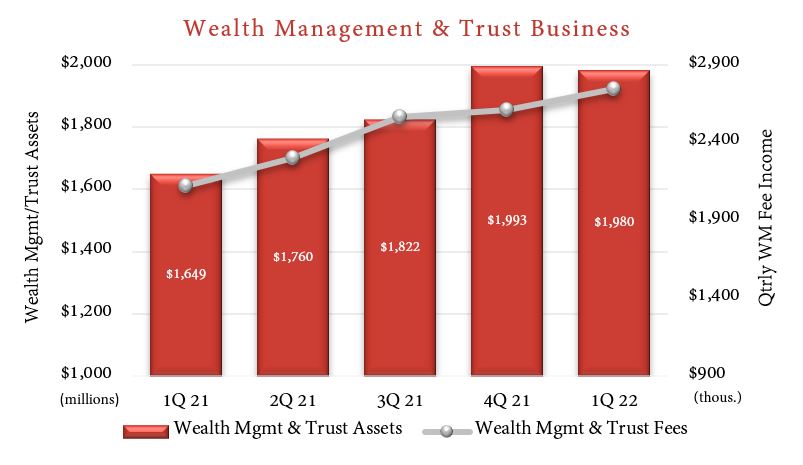

Wealth assets of $1.98 Billion, up 20% from 2021

Wealth fees up 29% year-over-year

$76 million in new wealth assets in the quarter, offset by declining market values

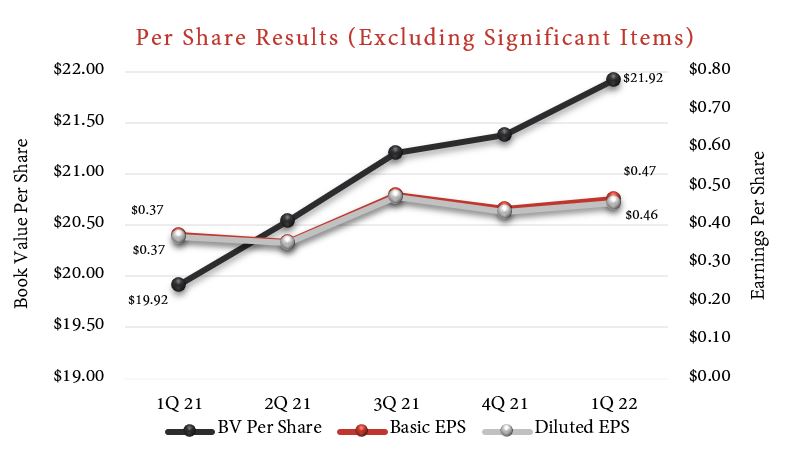

Core earnings per share, diluted of $0.46 vs. $0.37* year-over-year

4% increase in book value per share to $21.04 vs. $20.16**

Impacted by $5.7MM ”mark to market” downward adjustment to the securities portfolio, or $1.18/share

Paid $0.40/share dividend

33% increase from prior year

Record date of as of December 15, 2021, paid on January 14, 2022

*Excluding significant items. For detail on significant items, please see Financial Excerpts Excluding Significant Items below.

**For the period ended 3.31.2022 compared to 3.31.2021.

Letter to Shareholders

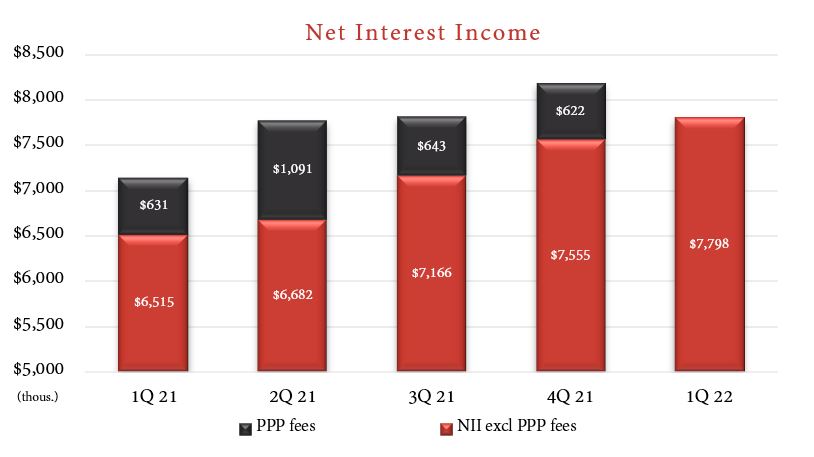

The first quarter of 2022 represents an exciting start for Oakworth. A strong close to 2021 set our company up to realize success in the first quarter of 2022. However, Oakworth’s performance should be considered in the context of numerous “moving parts” that impacted both the balance sheet and income statement. The major factors influencing our numbers include the significant reduction in overall Paycheck Protection Program (PPP) loan balances as the federal government systemically forgave balances to our clients; interest rate increases that impacted the value of the bond portfolio; the cessation of PPP revenue; and the adjustment to the overall allowance for loan and lease loss. (For detail on these factors, please see Financial Excerpts Excluding Significant Items below.)

Balance Sheet

Total loans grew 10% year-over-year without considering the impact of PPP loan balances. However, core total loans (excluding PPP loan balances) increased 24%. Oakworth certainly benefited from the significant amount of cash infused into the economy from government stimulus programs as evidenced by 35% growth in total deposits. We do expect a moderation in deposit balances for the rest of this year as clients pay tax obligations, government stimulus winds down, and interest rates increase. We were not immune to the industry phenomenon of book value per share pressure created by rates rising for the first time in two years. Rate increases and a higher mix of securities on our balance sheet are the primary drivers of a meaningful downward “mark to market” of the company bond portfolio. This “mark to market” adjustment resulted in muted growth in book value per share of 4% year-over-year. While our securities are classified as available for sale and therefore marked to market through bank equity, we have historically held them to maturity and do not anticipate realizing the current unrealized losses.

Wealth Assets

We crossed the $2 billion mark for wealth assets in the first week of 2022 and experienced continued success in our wealth offering with $76 million of new wealth assets in the quarter. However, the net change in wealth assets is flat given the offsetting impact of a general decline in market values of invested assets.

Income Statement

We closed and funded $35 million of loans in the last weeks of 2021 that established a record level of interest income entering 2022. This loan growth plus the loan growth in the first quarter drove a 23% increase in quarterly core net interest income compared to the first quarter 2021. In addition, we benefited immediately from the 25 basis point Fed Funds target increase in mid-March and anticipate further benefit from expected increases in the second quarter. Wealth revenue is up 29% compared to the first quarter of 2021, driven primarily by the growth in wealth assets. Finally, as we enter second quarter 2022, our wealth and loan pipelines are at record levels.

The trajectory of revenue and net income growth (excluding non-recurring items) followed the balance sheet with pre-tax, pre-provision income increasing 40% year-over-year first quarter. Our net income increased 26% year-over-year with the difference being the provision for loan losses that comes along with loan growth.

Quarterly Graphs

Financial Highlights

View Statements Below

In closing, first quarter 2022 was exceptionally positive financially and strategically. We are particularly pleased with the success of each individual market – South Alabama growing deposits by over 200% year-over-year and in line with overall pre-tax, pre-provision income growth at 40%; Middle Tennessee, our newest market, continuing strong loan growth and approaching $100 million in loans; and Central Alabama bringing in approximately $125 million of deposits over the course of the last year, along with 19% wealth asset growth in spite of the market downturn. Our balanced model of providing clients with the best solutions for their needs continues to prove successful.

We hope you will join us for our Annual Shareholders Meeting on May 18 at 4:00 p.m. Central Daylight Time at our headquarters in Birmingham and look forward to receiving your vote. Thank you for your continued support of Oakworth.

Sincerely,

Chairman and CEO

Macro & Market Perspectives

- A First Look at Q2

- Key Takeaways from Q1

- Stocks, Bonds & Asset Allocations