It is hard to believe that we only have a few short weeks left in 2025. Back in March of 2020, when the COVID-19 pandemic was in full swing, not many investors would have believed the returns that awaited stockholders. From the start of COVID-19, it seems like every presentation or client meeting that I was having began with the same conversation — how odd the current environment had been for the economy and stock market. After almost six years, I guess odd is the new normal.

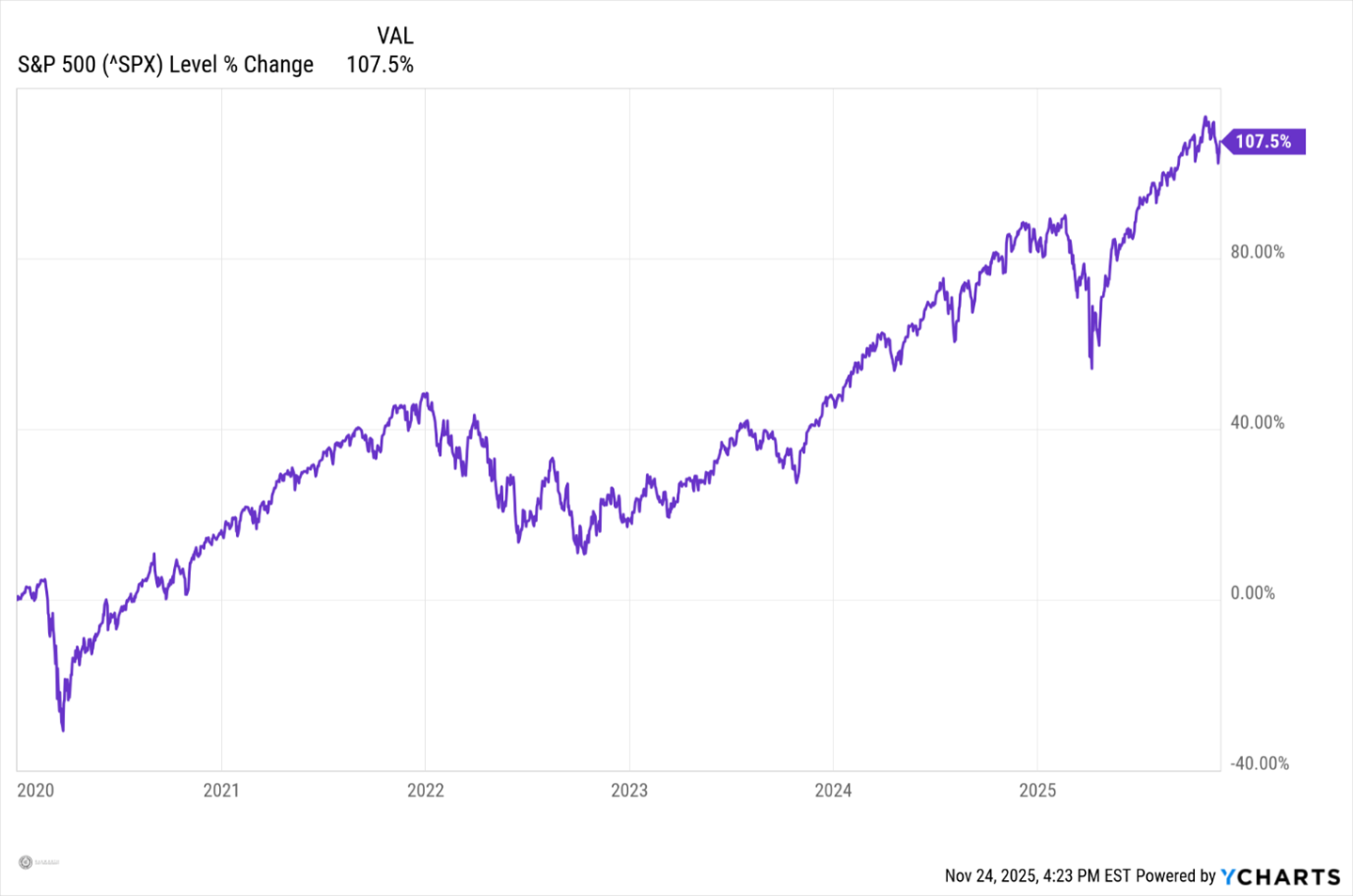

Given how strange the past six years have been, it is truly amazing to see how resilient the stock market has been. As I line up things to be thankful for, I need to include this on the list! Even with a very challenging 2022, the S&P 500 has more than doubled since the start of 2020. However, investors should be mindful that significant risks persist, including high inflation that erodes purchasing power, the potential for economic contraction and the inherent volatility of equity markets.

S&P 500 SINCE 2020

In my opinion, part of the stock market’s strength reflects just how tight the labor market has been. The past 6 years have provided us with the strongest labor markets in my career. We are still at a historically low unemployment rate of 4.4%. A solid labor market usually equals a strong, spending-oriented consumer. Without question, that has been the case.

The ultra-low mortgage rates during the COVID-19 years have also placed significant upside to home prices since 2020. The very top end of the consumer has benefitted from appreciating stock and home prices. The ballooning net worth of the top end of the consumer has allowed this group to keep spending. Americans that do not own a home or an investment portfolio have struggled to keep up with rising prices.

This is why many are calling the “recovery” from the COVID-19 recession in 2020 a “K” recovery. The letters that historically have been most often used to describe a recovery from a recession were “V” (sharp recovery), “U” (a delayed recovery) or “L” (no recovery at all).

The K description shows that the high-end consumer has exhibited a strong recovery, while the lower consumer is not able to keep up. A February PYMNTS study, “Consumers Change Spending Habits to Ease Monthly Money Squeeze,” showed that 65% of Americans are living paycheck-to-paycheck. That is a very scary statistic, and gives us an idea who is on the downward sloping part of the K.

As we are finishing the 3rd quarter of earnings season, most of the consumer discretion (retail) companies have reported earnings over the past few weeks. There is a very clear trend that has developed: the consumer is changing.

- Consumer confidence seems to be falling, and are more cautious with their money on discretionary items

- Consumers seem to be more value focused than they have in years

- Consumers are “trading down”, looking to discount retailers like Marshall’s and TJ Maxx

This is not a new trend, but a trend that seems to be getting even stronger. We have seen Wal-Mart for the past several quarters show strong grocery sales, as higher end consumers are “shopping down” to try and save money on their grocery bill. It should not come as a surprise that folks will try and do the same with their holiday shopping.

We are about to kick off the most important time for consumer spending, with black Friday and cyber-Monday kicking off the holiday spending season. I have seen black Friday ads running for the past several weeks. I think most retailers were jumping the gun just a bit, but it is hard to blame them. Many consumers say they will not be spending quite as much this year, so stores need to grab sales whenever they can. I can see “Cyber October” in our future.

That makes this Black Friday/Cyber Monday more unpredictable than usual. Will the low unemployment rate and very strong top end of the consumer make up for a very inflation-weary bottom two-thirds of Americans?

We will have a good idea in a few days, when we hear overall spending numbers for this promotional weekend. In a normal year, we could expect overall sales growth of 4% to 5% compared to last year. We will not know the winners and losers until we get actual corporate earnings reports in February of 2026. It seems that stores with the best value proposition for shoppers will have the most success in the next few weeks.

David McGrath, CFA®

Managing Director, Portfolio Manager, Oakworth Asset Management

Please note, this newsletter is for informational and educational purposes, and the commentary should not be considered or otherwise construed as an offer to buy or sell securities of any type. Any individual action you might take from reading this newsletter is at your own risk. My opinion, as well as those of our Investment Committee, is subject to change without notice. The opinions expressed herein are not necessarily those of the rest of the associates of Oakworth Asset Management, Oakworth Capital Bank or the official position of the company itself.

Opinions and forward-looking statements are subject to change without notice and may not come to pass. Past performance is not indicative of future results.

Advisory Services, including investment management and financial planning, are offered through Oakworth Asset Management LLC a registered investment advisor and is owned by Oakworth Capital Bank, Member FDIC. Investment products and services offered via Oakworth Asset Management LLC are independent of the products and services offered by Oakworth Capital Bank, and are not FDIC insured, may lose value, have no bank guarantee, and are not insured by any federal or state government agency. Because of the ownership relationship and involvement by Oakworth Asset Management LLC associates with Oakworth Capital Bank, there exists a conflict of interest to the extent that either party recommends the services of the other. Oakworth Asset Management LLC does not provide tax or legal advice. You should consult your tax advisor, accountant, and/or attorney before making any decisions with tax or legal implications. For additional information about Oakworth Asset Management LLC, including its services and fees, visit advisorinfo.sec.gov.