We started the 1st quarter of 2023 still worried about inflation and the Federal Reserve. By the end of it, investors were concerned about the health of the financial system. After all, higher interest rates lead to lower asset prices which reduce bank capital. So, would the Fed kill the economy in order to kill inflation?

The year had started so nicely, too. Stocks rebounded in January after slumping in December. Just about everyone thought the Fed might have only 0.50% worth of rate hikes remaining. It seemed the Fed was finally going to engineer the fabled “soft landing.”

Then, something happened.

While the inflation data had been better than it was in 2022, Chairman Jerome Powell spooked the markets with his comments after the February 15th Federal Open Market Committee (FOMC) meeting. Investors interpreted them to mean the Fed wasn’t done with only 0.50% in rate hikes. Nope. Perhaps it had 1.25% left, possibly 1.50%. If that wasn’t enough, the markets then had to deal with the collapse or near-collapse of several prominent banks.

While Silicon Valley Bank might not be a household name in much of the country, it was still a $200+ billion entity. Firms that size simply don’t go belly up very often. Overseas, the Swiss authorities arm-twisted UBS to take over the once vaunted Credit Suisse for pennies. Were we on the precipice of another 2008?

Fortunately, the answer to that is decidedly no.

The U.S. banking system is in much healthier shape than it was leading up to the most recent financial crisis.

Further, the economic data has been surprisingly resilient after over 4.50% in rate hikes. Finally, the official inflation gauges are poised to fall somewhat sharply during the 2nd quarter. While there are a number of reasons for this, the primary one is how the government calculates it.

In the end, the 1st quarter was yet another confounding quarter in what has been several years of confounding quarters. However, the good news is the light is at the end of the tunnel, at least as far as the financial markets are concerned.

- The economy is performing better than it should.

- Inflation will continue to come down.

- The banking system is in much healthier shape than the headlines suggest.

- Finally, the Fed will probably be finished with this tightening cycle by the end of the 2nd quarter.

That should lead to better investment returns in the not-so-distant future.

Thank you for your continued support,

John Norris, Chief Economist & The Investment Committee

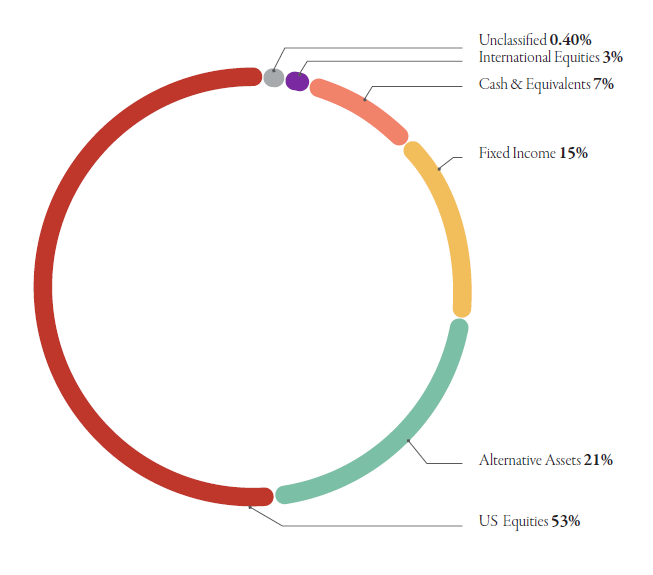

The Oakworth Capital Investment Committee distributes information on a regular basis to better inform our clients about pending investment decisions, the current state of the economy and our forecasts for the economy and financial markets. Oakworth Capital currently advises on approximately $1.8 billion in client assets. The allocation breakdown is in the chart below.

This content is part of our quarterly outlook and overview. For more of our view on this quarter’s economic overview, inflation, bonds, equities and allocation read our entire 1st Quarter 2023 Macro & Market Perspectives.