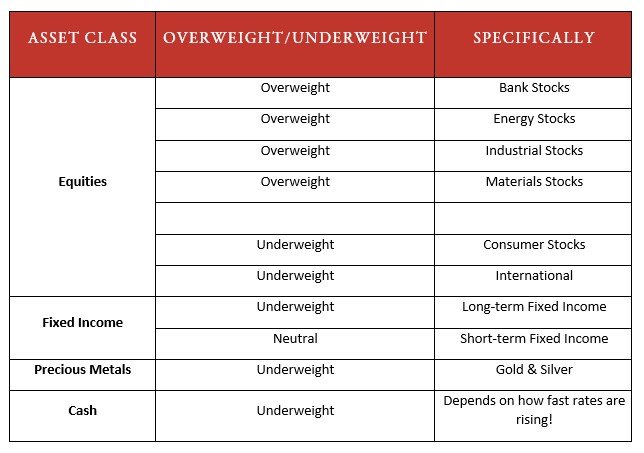

“We expect rates to move upwards over the next couple years” may be one of the most often repeated comments I hear every day in the financial media, and sitting right next to a tv with CNBC on for 8 hours a day, I hear it a lot. This thought is natural and almost the easy bet for two main reasons: inflation data has continued to run hot, and the economy continues to show signs of recovery. This ‘expectation’ is about as weak as the traditional cookie cutter expectation of 6-8% returns for any given year.

Nonetheless these expectations are cookie cutter for a reason: they are the probable outcome. If so, then our investment committee, along with every other asset manager, wants to have a plan for next year if it unravels like many think it will. So, what does it look like?

Quality is the first word that comes to mind when thinking about a higher interest rate environment, specifically in the equity space. A key component to any equity valuation is what is called the discount rate. The discount rate is the cost of capital for a company, and when interest rates rise, the discount rate rises as well.

Since the price of any stock is ideally the present value of the future cash flows discounted back to the present, this is where quality comes into play. If a dollar is worth more now than in the future, we are going to place a higher value on those companies in which produce quality cash flow in the present. A quality business model with quality cash flow and high-quality demand. Did I mention quality?

Of course, there are certain sectors which are going to perform better than others in a rising interest rate environment. Financials is the easy one. In a rising interest rate environment, the amount banks charge on loans will go up faster than the rates they pay for deposits. As such, rising rates means wider spreads, or interest rate margin. This which means more profit. This is good for everyone in the space from the traditional banks to the insurance companies to the capital market groups and the brokerages.

While intuitively financials may seem like the biggest benefactor of rising rates, energy, interestingly, actually one ups it. From 1966 through 2016, the energy sector outperforms the S&P by an average of over 4% in a rising rate environment. Rising rates are often associated with a growing economy, and this goes back to my original point of this being the easy bet. Our economy is growing. Rising rates can also be reactionary to inflation and a weaker dollar which is beneficial to energy, as most barrels of oil are priced in U.S. Dollars.

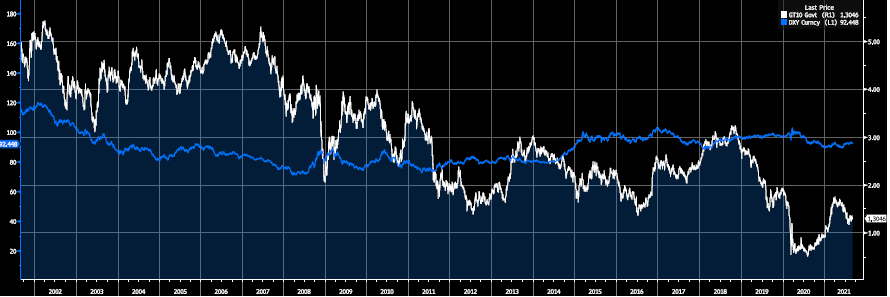

Wouldn’t that mean higher rates would strengthen the dollar and hurt the sector? Possibly in theory but that fact of the matter is we haven’t seen that strong of a correlation as seen in the chart below. In fact, as interest rates have continued to plummet over the last decade the dollar has strengthened.

When yields and the dollar are crashing, investors often flock towards international as a stronger foreign currency should buoy returns in foreign stocks. In the early 2000’s the dollar was weakening as seen in the chart above and this was the only period this century where international outperformed. If rates are going to continue to rise and help provide tailwinds for domestic stocks, we will continue to remain overweight, and underweight international.

Gold is often thought of as the inflation hedge so it should do well here, right? Not exactly. What gold really likes is lower real yields. Real yields are essentially the current rate of a treasury minus the breakeven inflation rate and right now the real yields are negative across the board. Essentially when calculated with inflation, you are losing money on a treasury held to maturity. As rates start to rise, real yields should increase creating major headwinds for the asset.

What about fixed income? Well, as John explained, higher rates means lower prices and who wants that? If rates are going to rise, most of the fixed income universe will suffer. Quality was the word of the day for equities, and the word of the day for fixed income is similar, but different. Duration. Let me explain. What I meant by quality is that I wanted companies that were making and delivering money to shareholders now, not sometime in the future. That is basically what duration is. The longer your duration, the longer you need to wait for the payment of coupons and principal. It is also defined as interest rate sensitivity. These are one and the same, and hopefully falls in line with my explanation of equities.

When rates are rising, we want all of our assets to be making us money now! Practically, with fixed income we want shorter duration assets if rates are going to rise. As I defined earlier, this means we get our money back quicker, and we have less sensitivity to the forecasted higher rates. The problem with shorter duration fixed income products is that with the less risk you take, like all things, the less reward you will receive.

For instance, the yield on short term fixed income products is disappointing, in both absolute and relative terms. Currently, the 5-year US Treasury Note is yielding roughly 75 basis points, 0.75%. Not very good. Further, even with short duration, you are still taking on interest rate risk and aren’t going to fare to well if rates are rising. So, short bonds are better than long ones when rates rise, but they still aren’t that great.

So, what does the overall portfolio look like? In fixed income, there is not much room to hide, as you naturally don’t want a depreciating asset. While bonds remain a part of any well diversified investment portfolio, we will want as little exposure as is possible when rates rise.

As far as equities are concerned, they are often the best place for capital in a rising rate environment. The S&P has averaged over 5.8% per year when rates are rising. While this isn’t much to write home about, it will be better than most other paper asset classes which will be going down in value. As we have been telling our clients this year, in a future rising interest rate environment, “stocks will be the most reasonably valued of all overvalued asset classes.

So, underweight fixed income and overweight equities? When rates are falling it’s a winner, and when rates are rising, well, it’s the best you got. Returns will undoubtably be harder to come by when rates rise; however, this does not necessarily mean negative returns. All it means is that asset managers will have to work a little harder for their returns, and that’s a challenge for which we will be prepared.