Section I

Yesterday, President Trump flummoxed the markets by announcing a 25% tariff on imported steel and a 10% one on aluminum. This morning, bright and early, the President was already hard at work on his Twitter account with the following:

“When a country (USA) is losing many billions of dollars on trade with virtually every country it does business with, trade wars are good, and easy to win. Example, when we are down $100 billion with a certain country and they get cute, don’t trade anymore-we win big. It’s easy!”

“We must protect our country and our workers. Our steel industry is in bad shape. IF YOU DON’T HAVE STEEL, YOU DON’T HAVE A COUNTRY!”

I imagine the average American would view this as throwing a gauntlet at Beijing. After all, how many times have we heard about Chinese “steel dumping,” protectionism, unfair government subsidies, and the like? Further, China is the only country with which we run an annual trade deficit in excess of $100 billion. Mexico comes in second, at around $71 billion in 2017. So, Trump has to be calling out China, right?

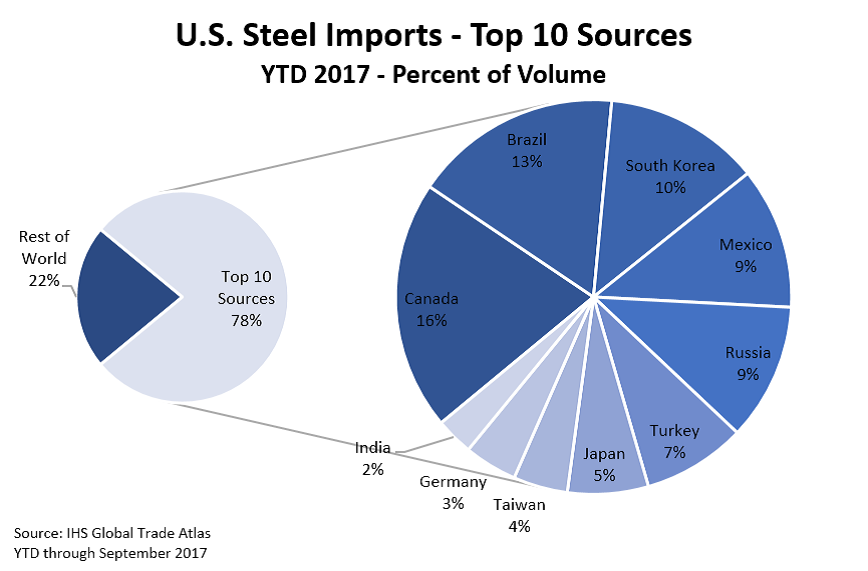

The only problem with this is we don’t import a substantial amount of steel from the Chinese, and it isn’t that large a line item in terms of overall trade. Huh? Yeah, according to the Department of Commerce’s International Trade Administration, the US imported less than 1 million metric tons of steel from China in 2016, which was good enough for 11th place. Take a look at the pie chart below. Amazingly (?), we import more steel from the Russians and the Turks than we do from the Chinese.

Then, let me just cut & paste this line from its ‘Global Steel Trade Monitor’ report released in December 2017: “In value terms, steel represented just 1 percent of the total goods imported into the United States in 2016.” Really? Just 1%?

Aluminum is a slightly different story, as the US imports roughly 90% of its primary (non-recycled) aluminum. From what I have read at minerals.usgs.gov (US Geological Survey – a bureau in the Department of the Interior), Canada is our top supplier, and it ain’t even close.

According to the ‘2015 Minerals Yearbook,’ the total quantity of aluminum imports from Canada was around 2.82 million metric tons. The Chinese were a very distant second at 395 thousand, and the Russians took home the bronze with 297K. All told, the Canadians accounted for almost 56% of aluminum imports by quantity. Yet we rarely hear of Canadian dumping, if at all. Ha.

Finally, our total trade deficit in aluminum in 2015 was an eye-popping $3.75 billion. While a lot of money to you and me, this represented 0.02% of 2015 US GDP, and less than 1% of total imports.

If I can pull this data pretty easily between meetings on a Friday morning in central Alabama, shouldn’t the Administration be able to do so before making trade policy? Or is there something else going on here? Something more than the dollar and cents reality of our steel and aluminum trade? Undoubtedly, but I am not sure I can tell you what that is. Maybe Donald Trump just really hates Canadians? Perhaps he has taken his apparent dislike for Justin Trudeau to a whole new level? Maybe it is none of that, and the Canadians just happen to be in the way? Probably.

When all is said and done, Trump’s tariffs, as I will call them, will be very popular with a lot of people in this country…maybe even a majority. Economic consequences? Geopolitical ramifications? Shoot, all of that fancy gobbledygook is important only to people who are too smart for their own good. So smart they are stupid, if you catch my drift. If we put America first, the rest of it will come out in the wash, right?

The cause of this type of thinking is pretty simple: the average American household hadn’t seen any real improvement in its standard of living this century. While ‘we’ are still at a very high level, purchasing power has been stagnant for the median household. A few years here and there are okay, but decades of treading water will take its toll on the old zeitgeist. To that end, median US household income (adjusted for inflation) was $58,665 in 1999. ‘We’ didn’t see a level that high again until 2016, when it reached $59,039, which works out to be a 0.04% annualized growth rate. Put another way: it took us 16 years to get to the same level of relative prosperity we enjoyed in 1999.

I mean, IF we are standing still, someone else has to be gaining on us. Indeed, they have. Since 1999, according to what I can find from the World Bank, inflation adjusted per capita income has grown by a multiple of 4 in China. Surely, their success is proof of our failure! Right? They must be to blame for our relative stagnation! The numbers don’t lie! They are what they are.

Maybe, but, then again, maybe not.

In December 1999, the Labor Force Participation Rate (the number of eligible working aged Americans actively participating in the workforce) was 67.1%, and the Employment to Population Ratio (the number of people working relative to the size of the population of eligible working aged Americans) was 64.4%. In February 2018, these numbers were 62.7% and 60.1% respectively. In 2016, the year used for per capita income, the percentages were, again, 62.7% and 59.8%.

So, compared to 1999, there are fewer Americans looking for work and actually working on a relative basis. As such, it would have been extremely difficult for median household income to increase. What with fewer paychecks per household, on average? But….but…China has been stealing all these jobs, so it makes sense fewer Americans are looking for work! After all, the commute to China is pretty long!

Well, the real reason, or the primary one at least, is the US population is getting older. In 19990, some 12.4% of Americans were 65 years of age or older. According to 2016 Census estimates, that percent has increased to 15.2%. That is a pretty significant shift, and as you know, older workers tend to retire at some point. Basically, the Labor Force Participation Rate starts to fall dramatically after 65.

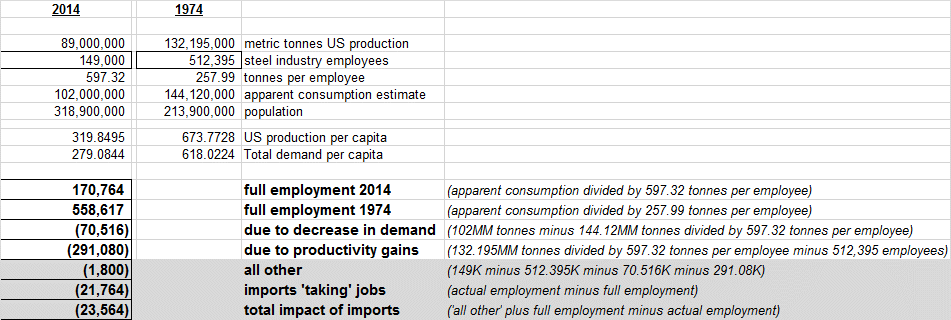

As for the steel industry, a couple of years ago, I compiled some data and concocted a spreadsheet to estimate what the impact imports had had on employment. I hope you can read this:

Basically, what the numbers suggest, at least mine, is the total impact of current imports (2014) on steel industry employment is/was roughly negative 21-24,000 jobs. The biggest cause for the ‘alarming’ drop in industry employment is the massive increase in worker productivity. Next up is the pretty substantial drop in domestic demand. Strangely enough, it would seem as though the impact on employment from imports would have actually been higher in 1974 due to lower US worker productivity at that time.

Obviously, this is just the math, my math. Plenty of other people have run similar spreadsheets, and come up with different numbers. However, I really don’t have a vested interest in this matter, so my calculations are about as unbiased as they can get. Yes, imports have taken and are taking jobs, or so it would seem. Even so, decreased demand and improved productivity has caused more job loses than the Canadians or the Chinese…mostly Canadians as the previous pie chart indicates.

So, why the tariffs on steel and aluminum? I would have to venture the decline in the steel industry over the last couple/several decades is the most obvious example of the shift from an industrial to a post-industrial economy. I can drive past the rusted out old steel mills here in town and “remember when,” back when the US was the world’s factory and all that jazz. It is hard to NOT wax nostalgic to some degree about those days.

So, someone has to be the villain here, right? And it is hard to hate Canadians, isn’t it? And it is certainly hard to hate ourselves for being too darn productive and efficient! So, who should it be? Well, the answer is pretty obvious, even though the numbers might suggest China isn’t really to blame…at least not directly in this instance.

As for the impact on the economy, at this point it is too early to tell. If the rest of the world shrugs its shoulders, it will be so much so what, and this is a very real possibility. After all, setting up and refitting steel mills are incredibly complicated and expensive endeavors. Is this added tax on 30% of the industry enough for US steel producers to significantly alter employment plans and dramatically increase capital expenditures?

I would be willing to bet a plug nickel against it. However, US Steel and Nucor probably will enjoy the little gift from Washington. In Twitter terms, I suppose you could say #moneyfornothing.

Section II

I have long maintained there are three primary ingredients for economic success: 1) the rule of law; 2) the development of human capital, and; 3) strong, definable property rights. Perhaps interestingly enough, these things aren’t absolutes, as they can and will vary with location and cultural norms. They just have to be transparent, evenly applied, and sacrosanct.

This past week, the powers that be in South Africa passed a motion to confiscate land from white farmers without monetary compensation. While whites make up a little less than 10% of the population, they own over 70% of the land. Intuitively, this is a holdover from colonial times and the racist apartheid regime which followed. So, this is a very politically popular move with the general population. Perhaps you could argue it is overdue or even just desserts.

But will it work? Will it help reduce wealth and income inequality in one of the most unequal economies in the world? Ah, that is the $64,000 Question.

First things first, the government says it won’t automatically evict anyone; that no one will lose their homes. Landowners will receive short-term leases on their former property, or some portion thereof. According to Julius Malema, the sponsor of the, let’s call it a, bill, the state will assume ownership of the land, and ultimately decide how to parcel it out. Pay close attention to that last sentence: the state will assume ownership of the land, not the private sector.

So, what will happen here, in purely economic terms?

The equity, or wealth, of an economy is essentially aggregate assets minus aggregate liabilities. That is Accounting 101. So, what happens when the government, any government, reduces the private sector’s assets without a corresponding reduction in its liabilities? By definition, wealth evaporates. It is just the math.

Now, what happens to the financial system when societal wealth, or capital, falls precipitously in a relatively compressed period of time? Is that good for banks? If the value of their collateral becomes zero and they can’t collect it in any event? What, then, happens to their loans? You know, the ones they made, and make every year, to the large white farmers?

Even if the white farmer pay back their loan this year, what is the likelihood the bank will extend the same amount of credit on the same terms next year? Now that the government owns what had been the borrower’s collateral? I will spare you the trouble: it won’t, and that is the best case scenario here. Period and end of discussion.

As such, if South Africa moves forward with this land confiscation program, the economy will, at best, suffer from a credit crunch, as banks reign in lending as wealth evaporates in the private sector with the proverbial swipe of a pen. This is a problem. At worst, it will lead to a collapse in the banking system and a drying up of foreign direct investment; in other words, an economic meltdown.

After all, who would want to invest where the government has the authority, and inclination, to expropriate private assets without compensation, for whatever reason? Even if the government’s actions are well-intentioned and popular, don’t you want some assurance it won’t take your investment without paying for it? Of course.

That is why property rights are so important: without them, your list of potential investors shrinks precipitously. If the South Africans are okay with this, so be it. However, they shouldn’t complain and point fingers when the inevitable happens.

Take care, and have a great weekend.

John Norris

This report does not constitute an offer to sell or a solicitation of an offer to buy or sell and securities. The public information contained in this report was obtained from sources and vendors deemed to be reliable, but it is not represented to be complete and its accuracy is not guaranteed.

This report is designed to provide an insightful and entertaining commentary on the investment markets and economy. The opinions expressed reflect the judgment of the author as of the date of publication and are subject to change without notice; they do not represent the official opinions of the author’s employer unless clearly expressed within the document.

The opinions expressed within this report are those of John Norris as of the date listed on the first page of the document. They are subject to change without notice, and do not necessarily reflect the views of Oakworth Capital Bank, its directors, shareholders, and employees.